While 2012 was arguably the year the solar mega project entered the public consciousness, with what are (for now) some of the world’s largest PV plants reaching completion, 2013 has seen its fair share of solar behemoths too. We profile the biggest projects of 2013 from the world's biggest markets.

Concentrated solar power has had a difficult year in the US, with several high-profile projects being turned down or shelved. But as Felicity Carus reports, it's a technology that still has some distance to run.

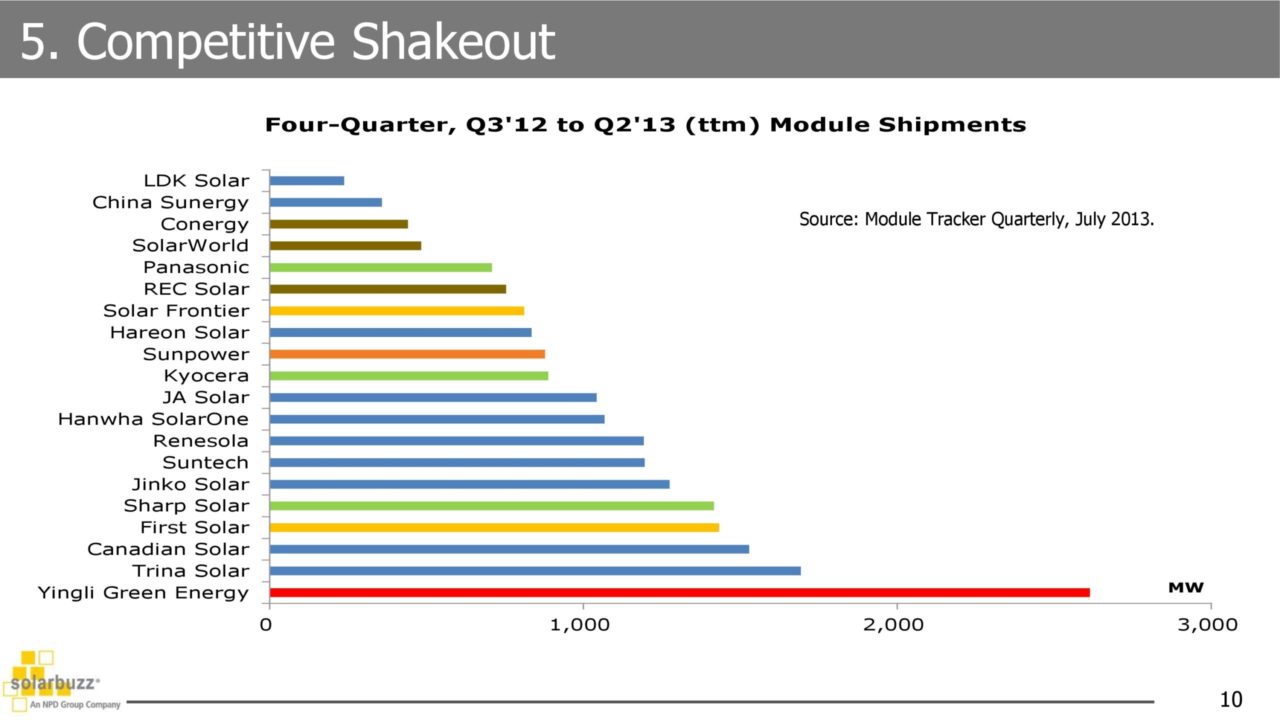

Trade disputes with the Chinese are still rumbling on in the US and Europe. As Felicity Carus reports, although efforts are still ongoing to find a settlement, the only winners so far have been Taiwanese cell manufacturers.

The search is on for the next source of solar finance once the Investment Tax Credit winds, and some elaborate ideas are on the table. Just don't mention sub-prime mortgages, says Felicity Carus.

Although much of the focus of debate in the US has been around residential and commercial solar, utility-scale projects represent the largest segment in America's PV market. But as Felicity Carus, the days of the PV 'mega' project could be numbered.

Neither commercial-scale nor energy storage have yet take off in the US. But as Felicity Carus reports, this could be about change as companies eye opportunities in both segments.

Solar deployment in Canada has so far largely been restricted to its biggest economy, Ontario. But as Felicity Carus reports, other provinces are now beginning to consider the technology, even Alberta, home to the controversial tar sands.

SunEdison is racing to build significant scale to its PV power plant project business, while SolarCity has just successfully added a new financial business model to its bow.

With the spotlight frequently shining on residential and utility-scale solar in the US, the commercial and industrial segments are often left in the dark. Felicity Carus reports on how they could shortly have their moment in the limelight.

Investor-owned utility companies are often seen as the enemies of the US's booming residential solar industry. But as Felicity Carus reports they are also emerging as solar providers themselves, with plenty more scope for their role to grow.