In early 2015, snow and ice in parts of North America created unexpected problems for solar plant operators. As winter approaches once again, Gwen Bender reflects on the challenges of keeping a project running profitably in harsh weather conditions.

Encapsulation is a key aspect of module durability, yet less effort is made to assess the quality of this process during manfuacture. Christian Honeker describes a new test procedure designed to improve the quality control of lamination and thus promote overall module performance.

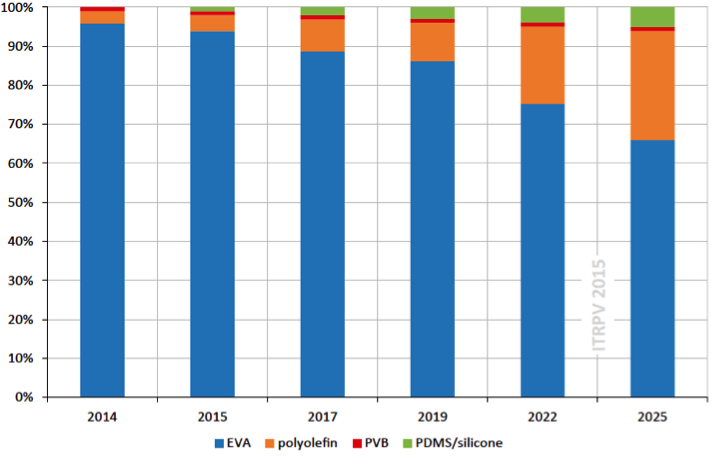

By Dr. Joris Libal & Dr. Radovan Kopecek, ISC Konstanz

Researchers are developing a new module specifically for use in desert areas, where much of the future growth in PV deployment is expected. Radovan Kopecek and Joris Libal of ISC Konstanz, one of the research partners involved, explain the thinking behind the 'AtaMo' module and its attributes in harsh conditions.

The growing size and geographic dispersal of PV power plants worldwide presents numerous supply chain challenges. Ulrike Therhaag runs through some of the essential steps in effectively managing the procurement process.

How silicon feedstock is packed into casting crucibles can have a big impact on the size and cost-efficiency of the resultant solar ingots. Til Bartel looks at some of the latest thinking around this essential stage in the PV manufacturing supply chain.

Last week the UN hosted the first of three crucially important global development conferences this year, culminating in the COP21 climate change talks in December. Reporting on the event, Alexander Lagaaij saw evidence of an appetite for cooperation, but still no high-level understanding of the potential of solar energy to put the world on a more sustainable path.

By Dr. Joris Libal & Dr. Radovan Kopecek, ISC Konstanz

PV technologists often face the question of what the next-generation solar cell work-horse will look like. Radovan Kopecek and Joris Libal of ISC Konstanz offer some answers.

PV's continued growth worldwide is creating fresh opportunities for investment in new and enlarged production facilities. But as Matthias Grossman writes, the costs and risks associated with entering new markets mean caution is required by investors.

As Europe seeks ways to impove the energy efficiency of its building stock, a key contributor to carbon emissions, building-integrated photovoltaics technology could offer some answers, writes Silke Krawietz.