At the start of each year, when market observers do their annual look at the year ahead, there is normally always a vague statement about some type of widespread consolidation of companies set to unfold.

And almost always, this fails to materialize.

Unlock unlimited access for 12 whole months of distinctive global analysis

Photovoltaics International is now included.

- Regular insight and analysis of the industry’s biggest developments

- In-depth interviews with the industry’s leading figures

- Unlimited digital access to the PV Tech Power journal catalogue

- Unlimited digital access to the Photovoltaics International journal catalogue

- Access to more than 1,000 technical papers

- Discounts on Solar Media’s portfolio of events, in-person and virtual

Or continue reading this article for free

This article shows just how fragmented the solar industry remains, and reveals the number of companies still accounting for the bulk of production and shipments across the polysilicon-to-module manufacturing value-chain, and companies that account for the production equipment, materials and gases used in the factories.

We then look at the companies attending the forthcoming PV CellTech 2017 event in Penang, Malaysia, 14-15 March 2017, as representative of the key manufacturing stakeholders in the solar industry today.

Finally, we present the latest updating upstream-strength rankings listing, which we initiated in 2016 within our in-house market research team, as a visual prompt arising from the data contained in the January 2017 release of our PV Manufacturing & Technology Quarterly report.

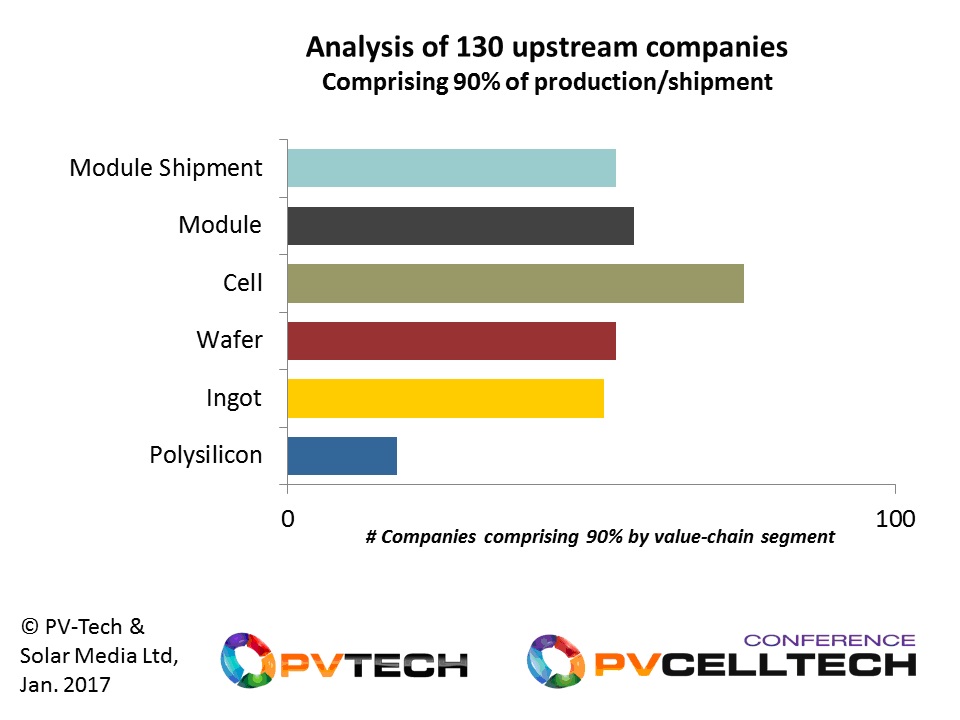

How many companies contribute to 90% of solar manufacturing?

If you posed the above question to ten ‘experts’ as part of a pub-quiz, you would likely get a wide range of answers. In fact, I tried this on a few occasions over the past six months, and answers ranged between 20 and 40 normally. So, let’s try to show the real answer now.

The graphic below goes all across the upstream value-chain, including polysilicon, ingot, wafer, cell, c-Si module, thin-film panel and final end-market shipment of modules/panels. The size of the bars for each shows the number of companies within each part of the chain needed to reach 90% of production (or end-market shipment of modules) during 2016.

Excluding polysilicon, each part of the value-chain (including end-market shipments) has anywhere from 50 to 75 companies making up 90% of industry activity. This is fragmentation in any shape or form.

However, many companies span the value-chain in production and shipment. Therefore the answer to the above question is not adding up the sum of the parts, but a smaller number.

If you perform that analysis, then you get to the answer: 130 (plus-or-minus).

Factoring in equipment and materials

If we now factor in the equipment, materials and gas suppliers that make up the 90% criterion, then (based on revenues), our count grows to approximately 200.

If we were to expand to 95% or (dare I say it) 100%, then we are looking at 3-4X this number, reflecting the vast number of mini-players still feeding into the solar PV industry.

Hopefully this helps to explain the title of this blog: so much for consolidation!

The reality is that for every merger, acquisition or terminal bankruptcy, there are other players still entering the solar industry.

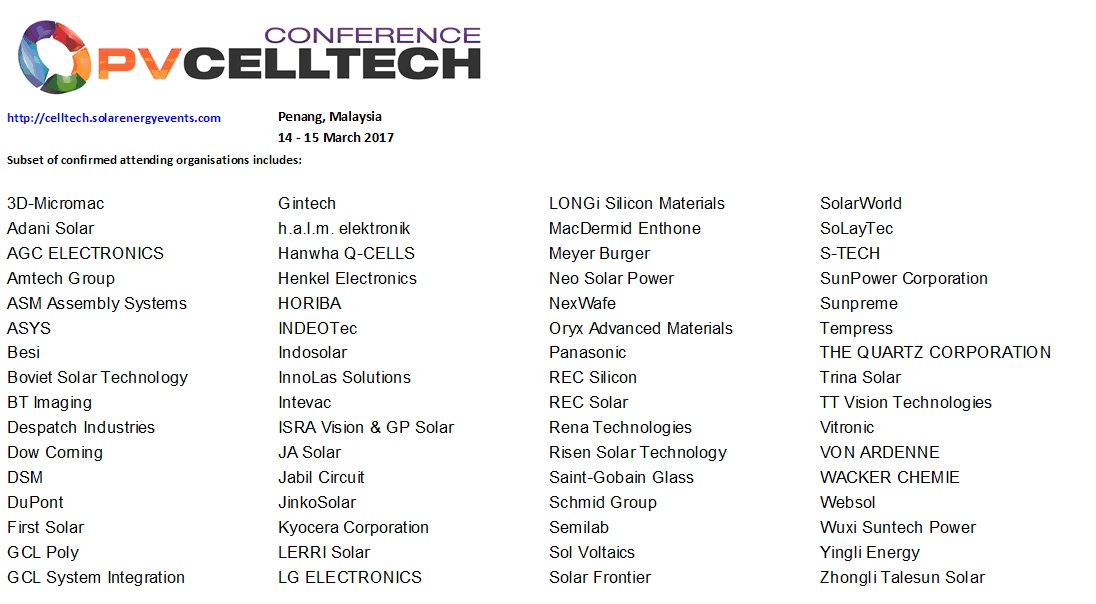

Who are the 200 companies that make up 90%?

What many would give to have this list! However, to flag up a partial list in this blog, we turn to the current company attendee list for our forthcoming PV CellTech 2017 event in Penang, Malaysia on 14-15 March 2017.

PV CellTech was designed to get the CTOs and Heads-of-R&D at a dedicated real-world PV manufacturing conference, something that the solar industry had been sorely missing in the past, with technology events confined to academic gatherings or an afterthought on the periphery of dedicated trade-shows.

Therefore, all going to plan, we should indeed have the must-meet and must-hear companies in attendance at PV CellTech.

Here is a subset of current list of companies that are confirmed to be at PV CellTech 2017 next month in Penang.

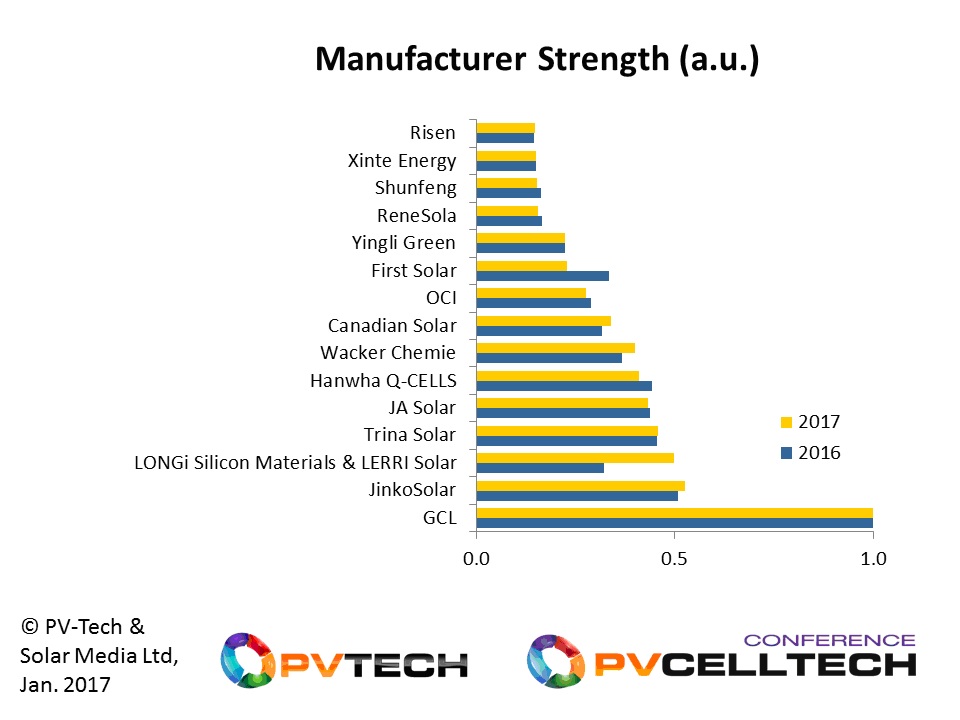

Who are the Top-15 upstream companies in the industry today?

We now move to the output from our reworking of manufacturing rankings that we introduced last year, in an attempt to provide more accurate ranking of the upstream segment, effectively ring-fencing the companies that are really driving output, technology and change.

In contrast to some of the value-chain specific Top-10 rankings we have covered on PV-Tech in the past couple of weeks (the Top-10 cell producers and the Top-10 module suppliers), the rankings graphic below applies a weighted stack-rank methodology based on in-house production levels and final module shipment numbers (company-produced and third-party branded).

Of course, it should be clear that these Top-15 companies below are in the 130 list, discussed above. Many of the CTOs from these companies will in fact be delivering the keynote and invited talks over the two days of PV CellTech 2017.

To view the latest PV CellTech agenda, please follow this link. To register for the event, click here.