Over the past year, many developers have asked a variation of the same question: will the solar investment tax credit still support the projects we plan to build?

The short answer is yes.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The longer answer — and the part that matters for procurement — is that eligibility no longer depends solely on what a project builds, but on how each component gets sourced, documented and verified.

H.R. 1 (the One Big Beautiful Bill Act) shortened the incentive runway created by the Inflation Reduction Act. For wind and solar, the clean electricity investment tax credit now applies only to facilities that begin construction by 4 July 2026 and complete construction within four years or achieve commercial operation by 31 December 2027. Projects that meet those conditions can still claim a tax credit, but the window for new qualifying projects is narrower than many developers hoped.

Importantly, H.R. 1 also tightened rules around “material assistance” from prohibited foreign entities and increased scrutiny around ownership, traceability and supply chain verification. Those changes influence how tax equity buyers evaluate risk and how equipment buyers compare module options.

This shift raises a new issue for procurement teams: counterparty risk in module supply and the question of what buyers need to know — not just about the product, but also about the companies, processes and upstream manufacturing behind it.

From performance risk to counterparty risk

For most of the past decade, PV module diligence focused on performance and degradation. Developers determined whether modules would deliver modelled output, whether warranties aligned with expectations and whether field reliability matched testing.

Performance still matters, but diligence has expanded. Buyers now face an additional question: what if ownership structures, traceability requirements, or legal exposure create problems downstream — especially for tax treatment?

Counterparty risk does not imply wrongdoing. In many cases, the issue is opacity. Treasury, investors and insurers want predictable projects, and predictable projects depend on verifiable suppliers. Buyers benefit from a clearer view into how modules are made, how upstream materials move through the supply chain, the ownership structure of each facility in the supply chain and how compliance claims can withstand audit.

Why diligence now extends beyond the module

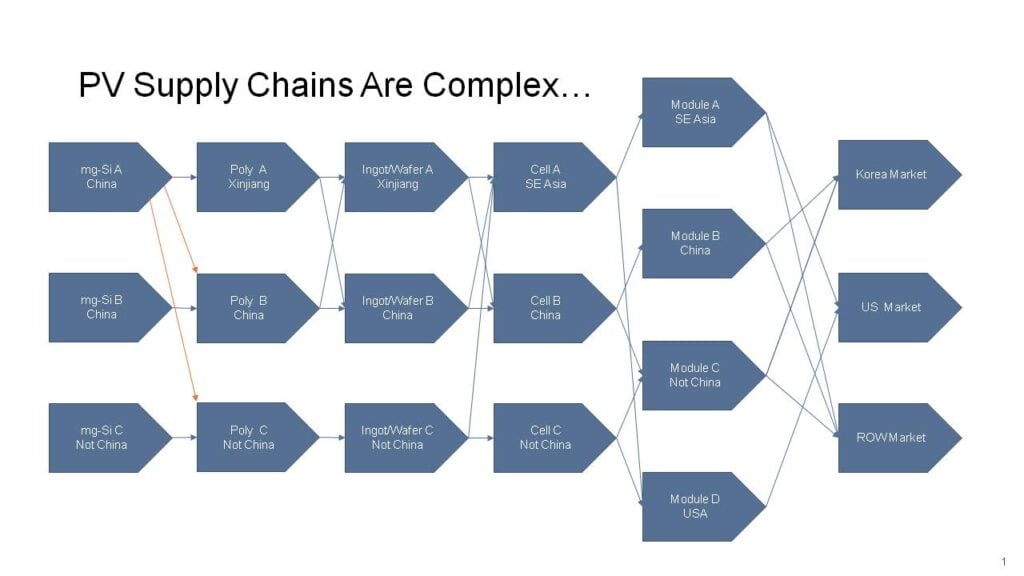

Conversations with developers and tax equity investors show a consistent pattern. Technical diligence on a finished module no longer closes the loop, because modules sit downstream of multiple inputs — cells, wafers, glass, backsheets, encapsulants, junction boxes, frames, adhesives and manufacturing processes that vary by supplier and facility. Even within a project, there may be multiple combinations and suppliers for these inputs.

Each input raises questions:

- Can the supplier document where each input originated?

- Can it demonstrate chain of custody?

- Can it verify that representations made to the buyer will hold up in an audit? Has an audit been done?

For many buyers, the goal is not to satisfy a specific statute, but to prepare for scrutiny. If a tax equity partner, insurer, or auditor requests evidence, can the project produce it? And will that evidence meet the counterparty’s risk model?

None of this is hypothetical. Recent and ongoing forced-labour enforcement, import detentions and diversion of supply during trade actions exposed gaps in traceability and documentation for modules originally procured on price and availability alone.

Why documentation now matters for tax-equity confidence

The investment tax credit remains a cornerstone of PV finance for projects that qualify. Tax-equity partners continue to support projects, but diligence now includes deeper inquiry into how eligibility might be challenged.

Developers report more tax-equity questions about:

- traceability

- ownership structure

- country of origin

- chain-of-custody audits

- representations and warranties

- data sufficient for verification

Not all projects encounter the same level of questioning. Larger portfolios, merchant-exposed assets, or deals involving new tax equity relationships often face deeper diligence. For all of them, verified documentation reduces uncertainty and lowers the risk of discounted credit value or delayed monetisation.

Tax certainty vs. tax optionality

Developers increasingly choose between certainty and optionality.

Tax certainty favours suppliers with robust documentation, audited traceability and consistent disclosures. These suppliers may command a premium, but they reduce the risk of future negative findings during the determination of tax credits.

Tax optionality prioritises price and availability, while maintaining a plausible path to documentation. This approach may lower upfront costs, but it can create delays or negative findings that undermine financing and eventually tax credits if a supplier’s disclosures do not satisfy tax equity investors and tax authorities.

Both strategies coexist. The choice depends on financing structure, investor relationships and the developer’s tolerance for risk.

The role of independent verification

Suppliers can provide documentation directly, and for many buyers, that remains the first step. Verification layers strengthen representations and reduce ambiguity for tax equity, insurers and auditors. Independent verification may include:

- facility audits

- mass balance assessments

- environmental and social due diligence audits

- supply chain mapping

- traceability documentation

- ownership disclosure reviews

These tools do not exist to “catch” suppliers. They exist to make procurement more predictable, increase confidence in tax credit eligibility and support representations that may be tested years after COD.

What PV buyers should watch in 2026 and 2027

Several factors may shape procurement strategy this year and next:

Treasury guidance and market interpretation. Clarification on documentation, material assistance rules and prohibited foreign entity guidance may influence how tax equity prices risk.

Supply chain transparency expectations. Developers, offtakers, investors and insurers continue to raise standards as part of risk management, often borrowing from enforcement frameworks developed for forced labour.

Evolution of ownership and corporate structures. Consolidation, foreign investment and restructuring may affect counterparty assessments even when the technology and manufacturing facilities do not change.

Forced labour enforcement and trade actions. These remain active and influence routing, availability and documentation.

Project timing relative to H.R. 1 deadlines. Developers now evaluate whether to accelerate procurement to meet the new deadlines or assume post-ITC economics.

Solar still benefits from the ITC, but procurement has new dimensions

The US solar market does not lack projects. It lacks clarity around the documentation and verification needed to convert eligible projects into financeable ones under compressed timelines. Buyers that integrate verification into procurement — not as a final step, but as a parallel track — deliver projects with fewer surprises and more straightforward tax treatment. Independent diligence shortens the learning curve for developers by catching gaps in supplier documentation and resolving traceability questions before they delay financing.

Solar has benefited from decades of cost reduction, technology learning and performance improvement. The next phase rewards developers who reduce uncertainty in how projects qualify, not just how they perform.

Paul Wormser is senior vice president, technology at Intertek CEA