Artificial intelligence is already embedded in the PV value chain but brings with it complex challenges. David Moser of Becquerel Institute Italia explores how to navigate workforce disruption, data risks, regulatory gaps and digital sovereignty in the age of solar automation.

Artificial intelligence is no longer a distant prospect for the solar photovoltaic industry. It is arriving now. From automated project design and predictive maintenance to robotic panel installation and algorithmic energy trading, AI and robotics are here to reshape every link in the photovoltaic (PV) value chain. The potential gains are substantial: lower costs, faster deployment, improved asset performance, and the ability to scale solar at the pace the energy transition demands.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Yet for all its promise, the integration of AI into solar brings with it complex challenges and risks that the industry must confront head-on. These are not abstract, futuristic concerns. They are emerging right now, in real projects and real day-to-day operations, as companies have to deal with workforce displacement, unreliable data, undefined legal liability, cybersecurity vulnerabilities and the uncomfortable reality that Europe’s solar sector is increasingly dependent on a handful of non-European technology providers for its digital backbone.

This article maps the big-picture challenges shaping the AI-solar nexus, drawing on the ‘Transforming the PV sector: the AI & robotics revolution’ report, published by the Becquerel Institute in 2025 and constantly updated. It explores what can go wrong, what is already going wrong and what the sector must do to steer AI adoption toward outcomes that are efficient, equitable, secure and resilient.

The workforce question: displacement, disruption and the skills gap

Of all the challenges AI presents to the solar industry, the impact on jobs is perhaps the most discussed. The sector has built its social licence in part on the promise of green employment, translated into millions of jobs in installation, operations and manufacturing worldwide. AI and robotics threaten to contradict that narrative.

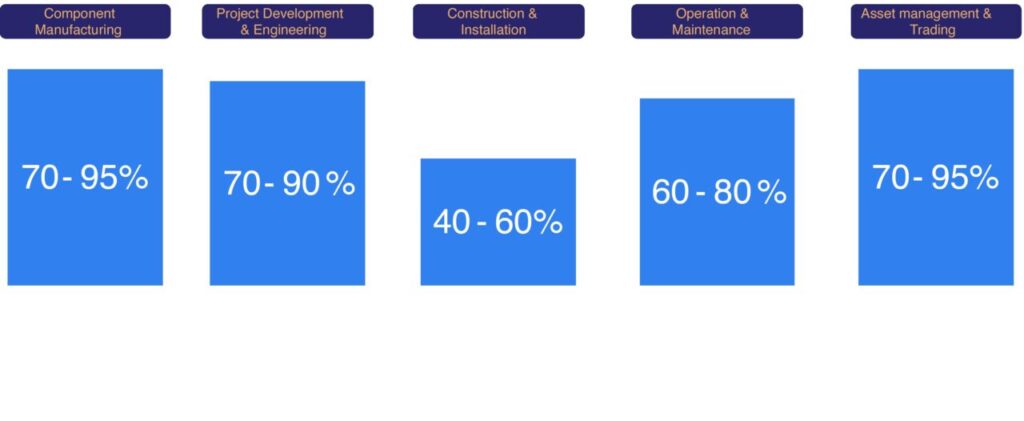

Analysis from the ‘Transforming the PV sector’ report projects that combined AI and robotics implementation could reduce workforce requirements by up to 60% on a per-megawatt basis compared to traditional approaches. In the most accelerated scenario, the industry could move from roughly 20 jobs per megawatt today to fewer than five. Manufacturing, construction and O&M roles are all exposed to varying degrees, while asset management and development engineering, being heavily knowledge-based, face the deepest proportional cuts.

The numbers are scary, but they must be properly explained, as this does not necessarily translate into mass unemployment across the sector as a whole. Automation will simultaneously accelerate overall PV deployment by decoupling growth from workforce constraints, meaning total employment in solar may hold steady or even grow in absolute terms. New roles in AI development, robotics maintenance, data science and system oversight will emerge. But these are fundamentally different jobs, requiring fundamentally different skills. That is where the real challenge lies.

The skills gap is difficult to quantify, but an estimated 25-30% of existing workers are projected to successfully transition to oversight or AI-adjacent roles without significant retraining. The mathematical, programming and systems-thinking capabilities required for the new positions differ substantially from the practical, hands-on skills that define much of today’s solar workforce. Education systems, meanwhile, are forecast to meet only 60-70% of new skill needs by 2028, an optimistic projection given historical difficulty in aligning curricula with fast-moving technology domains.

There is also a geographic mismatch. The jobs being eliminated, often in construction and field operations, tend to be in different regions from the new jobs being created, which cluster in technology centres and urban areas. Only a small share of displaced workers are estimated to be willing to relocate, risking structural unemployment in some communities even as skills shortages persist elsewhere. Social acceptance should not be underestimated either: the industry’s licence to automate will depend on how well it manages the human side of the transition.

Data accuracy and reliability

Predictive AI is only as good as the data it is trained on and fed in real time. In the solar industry, the quality of that data varies enormously, and the consequences of getting it wrong can cascade through entire portfolios. The “garbage-in, garbage-out” problem is well understood in principle, but its practical implications in PV are only now becoming apparent as AI systems take on higher-stakes roles. Errors in weather datasets, production records, or sensors can propagate through AI models and lead to misguided operational decisions, like scheduling unnecessary maintenance, misjudging energy yields, or failing to detect genuine faults. As models become more complex and opaque, tracing the origins of mistakes or biases becomes increasingly difficult.

The data landscape in solar is fragmented. Equipment specifications, performance data, maintenance records and financial information often resides in disconnected systems with incompatible formats and are rarely connected through interoperable systems. Legacy assets, which make up the majority of installed capacity, frequently lack the sensor density or digital infrastructure needed for effective AI deployment.

This creates a digital divide between newer, data-rich installations and the existing fleet, where data quality is poor or unavailable. Without industry-wide data standards, the benefits of AI may remain confined to within-segment optimisations rather than delivering transformative cross value-chain integration. Generative AI can significantly reduce data quality risks, but not entirely eliminate them. Human oversight, better digital infrastructure and robust governance remain critical.

Data security and privacy are growing concerns as well. Sensitive information on asset performance, grid conditions and site locations is increasingly moving into the cloud and across borders. The attack surface expands with every new connected device and data stream, making robust data governance not just a technical requirement but a strategic imperative.

Legal liability and the regulatory framework

As AI systems assume greater responsibility for decisions in the solar value chain, from automated engineering designs to autonomous trading strategies and robotic construction, the question of legal liability becomes unavoidable. Who is accountable when an AI-driven decision leads to equipment damage, a safety breach or a financial loss?

Current regulatory frameworks and insurance policies were designed for a world in which humans oversee critical decisions and operations throughout the PV lifecycle. Building codes, electrical standards, grid connection requirements and financial regulations typically specify human certification or supervision for key processes. The transition to autonomous systems will require these frameworks to evolve, but regulatory adaptation typically lags behind technological capability, creating a compliance grey zone for early adopters.

Engineering decisions carry particularly important liability implications. Licensed professionals are legally responsible for design adequacy and public safety. Existing regulatory frameworks governing professional engineering may not easily accommodate AI-generated designs without human verification, creating a legal requirement for oversight that limits full automation potential.

Until these frameworks evolve to specifically address AI-generated outputs, the human verification requirement will persist as a constraint, particularly for structural and electrical engineering aspects with safety implications.

In energy trading, organisations may be reluctant to delegate high-value decisions to autonomous systems due to governance and liability concerns. Regulatory frameworks may impose limits on algorithmic trading in critical infrastructure markets to prevent systemic risks, similar to circuit breakers in financial markets, restricting AI systems to advisory roles for high-consequence decisions.

Insurance and financing structures compound the problem as established risk models are based on human-operated systems. AI approaches may face higher premiums or financing costs until sufficient operational data demonstrates their reliability. This institutional friction could delay adoption even when technologies are technically and economically ready, and the timeline for adaptation will vary across jurisdictions, creating uneven deployment patterns worldwide.

The fragmented regulatory environment, especially within Europe, adds further compliance risk where multiple subcontractors interface proprietary AI algorithms across a single plant.

Cybersecurity

The more the solar industry digitalises, the more it exposes itself to cybersecurity threats – and the stakes are high. PV assets are critical energy infrastructure, and a successful cyberattack on widely used AI systems could have cascading impacts across hundreds of plants or grid nodes. AI systems controlling operations, maintenance and trading require comprehensive data access and often internet connectivity, creating potential attack vectors. Robotic systems with physical capabilities introduce safety risks beyond traditional IT security: compromised systems could damage equipment or endanger personnel.

The integration of operational technology with information technology across the value chain is particularly challenging, as these domains have historically operated with different security models. Robust security measures may increase system complexity and cost beyond current projections, and concerns about vulnerabilities could limit adoption in critical infrastructure applications.

Systemic risk is the larger worry. As the industry converges on a relatively small number of AI platforms and cloud providers, a vulnerability in one widely deployed system could affect a significant share of global solar capacity. This concentration of digital risk mirrors the concentration of physical supply chains that the industry has already experienced with module manufacturing, but with potentially faster and more widespread consequences.

Dependence on non-European AI and cloud infrastructure

For European solar companies and policymakers, one of the most strategically uncomfortable dimensions of the AI transition is the sector’s growing dependence on non-European technology infrastructure.

The AI and cloud platforms underpinning the industry’s digital transformation are overwhelmingly provided by a few US-based technology giants. This concentration raises several interconnected concerns: data residency and privacy risks tied to non-EU jurisdictions; vendor lock-in that threatens the competitiveness of European companies; and geopolitical risk, including potential trade restrictions or shifting data-movement laws that could disrupt access to the very infrastructure on which solar operations depend.

The strategic vulnerability is real. Europe’s solar industry is one of the world’s largest by cumulative installed capacity, and its ambitions require massive further scale-up. If the digital layer controlling this infrastructure is owned and governed from outside Europe, the continent’s energy sovereignty is compromised in a new and largely unexamined way. Investment in AI for solar is also geographically skewed, with recent major funding rounds concentrating in US-based startups and digital leadership sitting primarily with China and the United States.

Prospects for European-made AI platforms

The growing awareness of digital sovereignty risks is prompting action. EU policymakers and parts of the private sector are investing in developing native AI technologies and sovereign cloud solutions tailored to the energy transition. Initiatives seek to foster interoperability and data protection standards, while EU research programmes aim to stimulate local innovation in AI. The EU AI Act, with its emphasis on transparency, accountability and environmental sustainability, is establishing a regulatory identity that could shape how AI is developed and deployed across the continent’s energy sector.

But the path to European-made AI platforms for solar is far from straightforward. The European AI ecosystem remains less mature, with fragmented initiatives and fewer large-scale platform providers. Talent retention is a persistent challenge, as researchers and engineers are drawn to better-funded opportunities abroad.

But there is a window of opportunity. The PV sector’s specific requirements, domain expertise, regulatory familiarity and data localisation needs could favour specialised European entrants over general-purpose global scalers, provided the investment and policy support materialise. The question is whether Europe can move fast enough: the technologies being deployed today will shape the competitive landscape for decades, and first-mover advantage in AI platforms tends to be durable.

Technical and operational challenges

Beyond the strategic and regulatory dimensions, a range of technical challenges confront the solar industry as it integrates AI into daily operations.

Integration and interoperability remain significant hurdles. AI must operate not only within individual solar assets but across grid operators, market platforms and distributed energy resources. The PV industry currently lacks comprehensive data standards and interoperability frameworks. Equipment from different vendors, data in incompatible formats and disconnected software systems create friction at every boundary, risking siloed benefits rather than end-to-end optimisation.

The “black box” problem presents a particular challenge for safety-critical applications. Many advanced AI models lack the transparency needed for troubleshooting, compliance auditing, and operator trust. The industry urgently needs progress on explainable AI and new transparency benchmarks, particularly for plant operations where errors carry safety or financial consequences.

Legacy assets represent a structural barrier. The existing installed base was not designed for robotic maintenance or AI-driven operations, and this fleet represents the majority of maintenance needs through 2030. This bifurcation between AI-ready and legacy systems limit the addressable market and could widen the performance gap between early adopters and the rest. Implementation costs remain substantial, especially where digitalisation steps must come first.

For smaller operators, these costs may prove prohibitive, potentially creating a two-tier industry.

The big picture: systemic risks and the erosion of human expertise

Stepping back from individual challenges, two overarching risks deserve attention. The first is systemic fragility. As digitalisation deepens and the industry converges on shared platforms, the potential for correlated failures grow. A software bug, a flawed algorithm update, or a coordinated cyberattack could propagate through interconnected systems far faster than any physical fault.

The industry is not yet accustomed to thinking about risk in these terms; its engineering traditions are rooted in physical redundancy and local control, not in the distributed, software-defined architectures that AI demands.

The second is the gradual erosion of human expertise. Over-reliance on AI may lead to a loss of traditional engineering skills and local operational knowledge. If technicians and engineers no longer understand the systems they oversee at a fundamental level because the AI handles the analysis, the diagnostics and, increasingly, the decision-making, the industry becomes vulnerable to situations the AI was never trained for.

Edge cases, novel failures and black-swan events require human judgement grounded in deep domain knowledge. If that knowledge is eroded, the sector’s long-term resilience suffers. This is not an argument against AI adoption. It is an argument for thoughtful adoption, for preserving and valuing human expertise even as technology augments and, in some areas, replaces it.

Conclusion: managing the transition

AI in solar holds immense promise. It can drive efficiency gains that make the energy transition faster and cheaper. It can unlock new business models, from autonomous asset management to algorithmic grid services. It can help address the industry’s persistent labour shortages and quality inconsistencies. But realising these benefits while managing the accompanying risks requires deliberate, coordinated action.

For industry, that means investing in workforce transition alongside technology; prioritising data governance and AI model validation; developing transparent, auditable systems; and collaborating to define standards and best practices.

For policymakers, it means modernising regulatory frameworks to clarify AI liabilities; incentivising European innovation in cloud and AI platforms; fostering cross-border standards harmonisation; and investing in targeted retraining for workers at risk of displacement.

For all stakeholders, it means approaching AI with both ambition and humility. The coming years will determine whether the PV sector embraces AI as a strategic priority with eyes open to the risks or sleepwalks into a transformation it does not fully control. The choices made now, on governance, investment, workforce policy and digital sovereignty, will shape the solar industry for decades to come.