Clean energy investor confidence in Australia has deteriorated sharply over the past year, according to the Clean Energy Investor Group (CEIG).

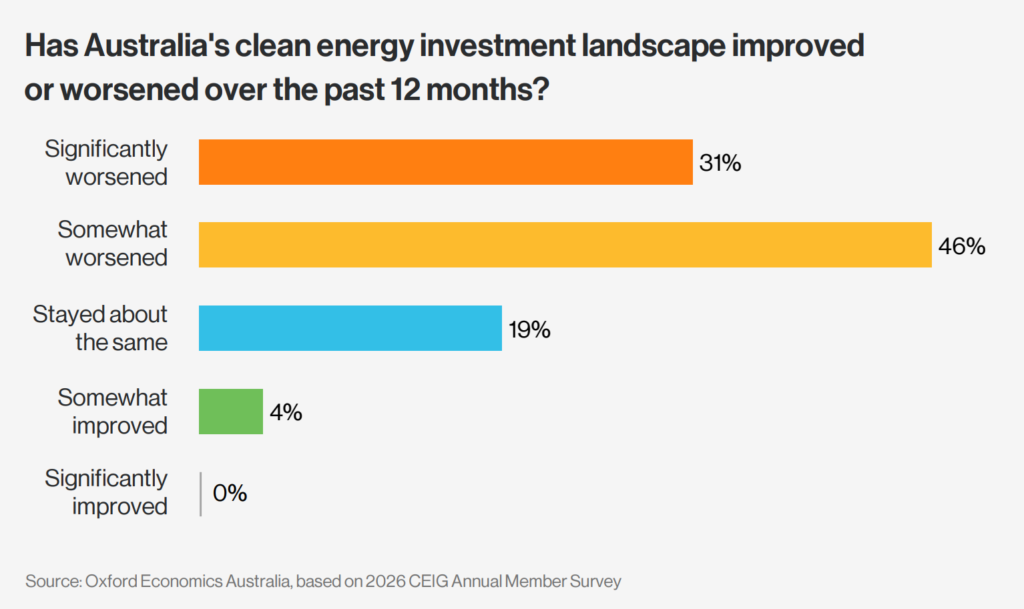

According to the advocacy and engagement platform’s ‘2026 Clean Energy Outlook,’ 77% of members surveyed said the investment landscape has worsened, including 31% who said it has worsened “significantly”.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The survey, conducted by Oxford Economics on behalf of CEIG, whose members collectively control 18GW of renewable energy capacity across 139 power stations valued at more than AU$41 billion (US$28.41 billion), marks the third consecutive year of the annual member survey and produces some of its most downbeat readings to date.

The share of respondents rating Australia as “very attractive” for clean energy investment compared to other countries has fallen from 23% to 12% in a single year, while those rating it “somewhat unattractive” have more than doubled from 8% to 19%.

Despite those shifts, 58% of respondents still view Australia as somewhat or very attractive overall, down from 69% in 2025, with regulatory and institutional stability, confidence in the rule of law, and the country’s renewable energy resource base cited as the foundations of that residual appeal.

The findings arrive as AEMO is calling for nearly 120GW of utility-scale wind and solar by 2050, roughly five times current capacity, with the 2026 Integrated System Plan explicitly stating that delivery is now the primary constraint.

The CEIG survey suggests investor confidence in that delivery is weakening precisely as the scale of the task grows.

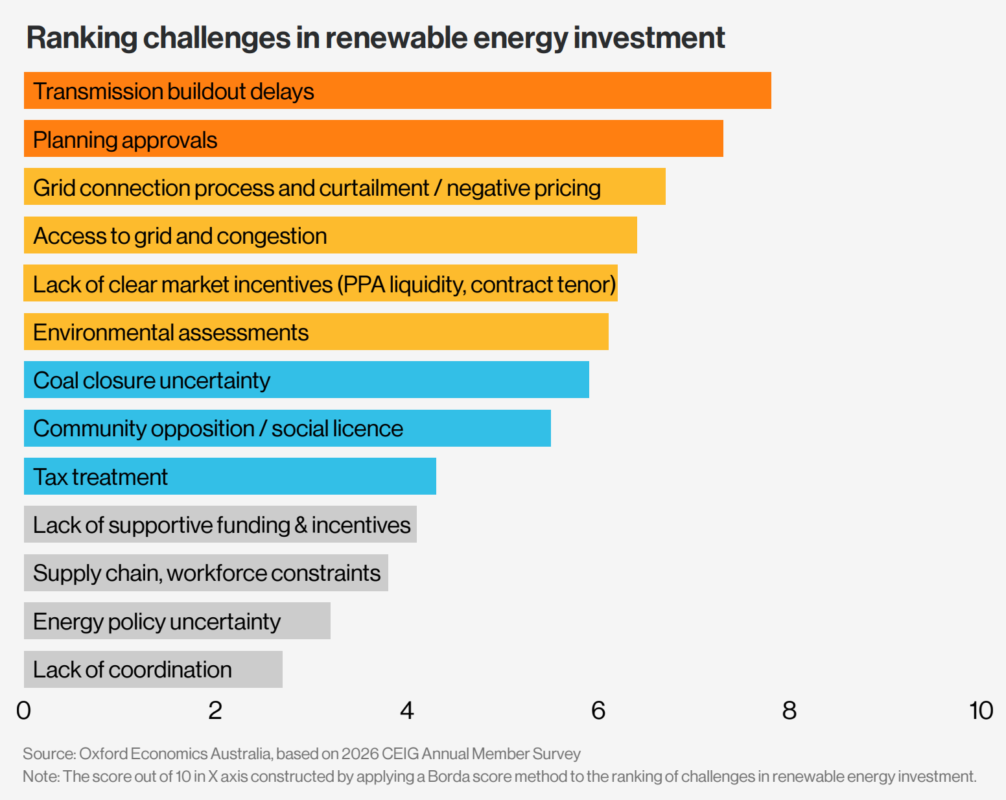

Transmission buildout delays have risen to become the single largest challenge facing renewable energy investment, overtaking planning approvals, which topped the list in 2025.

The report notes that progress on transmission infrastructure was expected following the positive reception of the 2025 federal election outcome, which 90% of respondents in last year’s survey described as a positive development for clean energy. That confidence has not been borne out.

Planning approvals ranked second in the 2026 challenges list, with the report noting that despite several recent reforms, including changes to the EPBC Act and the New South Wales Planning Systems Reforms Act, investors have yet to see meaningful improvements.

Grid connection processes, curtailment and negative pricing and access to grid and congestion rounded out the top five challenges.

Greater transparency and certainty around the Capacity Investment Scheme also emerged as a priority theme, with respondents raising concerns about market distortion, limited support for wind and long-duration energy storage (LDES), and insufficient clarity around future auction design and delivery.

State rankings shift as Queensland holds and Western Australia rises

At the state level, New South Wales retains its position as Australia’s leading destination for renewable energy investment with a renewable energy investment potential score of 9.3 out of 10, well ahead of Queensland at 7.6.

Despite New South Wales’ position at the top, investors identified planning approvals, grid access, and congestion as key constraints within the state, with 57% of the state-focused respondents citing planning approvals as a challenge and 38% citing grid access and congestion.

The biggest mover in the state rankings is Western Australia, which has risen two places to third since 2025 with a score of 7.0. The state government’s release of the South West Interconnected System Transmission Plan is credited with providing investors greater certainty, though the lack of a renewable energy target and a shallow offtake pool were identified as factors limiting further improvement.

Victoria has slipped to fourth at 6.7, identified as the worst state in the country for transmission build-out, with 43% of investors citing transmission delays as the primary challenge. Alongside South Australia at fifth place with a score of 6.2, Victoria continues to suffer from curtailment and negative pricing.

Queensland had already been under pressure from policy uncertainty in the 2025 survey, and the Queensland government’s decision to run coal power stations until the end of their useful life, rather than targeting closure by 2035 as the previous government had planned, has introduced further uncertainty about the market signals needed to support new investment, with 59% of Queensland-focused respondents citing energy policy uncertainty as a challenge.

The 2030 target and what could unlock investment

The survey’s findings on the 82% renewable energy target by 2030 represent its starkest result.

Just 8% of respondents believe Australia is on track to meet the target under current settings. A further 27% are not sure. 65% believe Australia will not meet it.

The report notes that closing this confidence gap will require stronger revenue certainty for new projects, faster delivery of transmission infrastructure, and CIS reform better aligned with final investment decisions.

Data centres represent the survey’s most positive finding. The NEM’s market design was already under scrutiny as investors grew frustrated with barriers to project delivery, but 92% of respondents view growing data centre demand as a positive for clean energy investment, with 50% describing the impact as “strongly positive”.

Investors broadly agreed that for this demand to translate into new renewable energy generation and storage, data centres should be required to source electricity from new and additional renewable energy capacity, consistent with the federal government’s National Data Centre Expectations framework.

Long-term power purchase agreements from data centre operators were identified as a mechanism that could deepen the shallow offtake market, constraining investment in multiple states, particularly Western Australia and South Australia.

CEIG’s recommendations from the 2026 report are framed around four priorities. Accelerating transmission buildout.

Improving grid connection and access processes. Strengthening revenue certainty through CIS reform and clearer signals on coal closures, and ensuring that data centre demand growth is matched by additional renewable energy generation and firming capacity rather than drawing on existing grid supply.