Every utility-scale PV project starts with a number: expected annual energy yield. It shows up as PVOUT and it quickly becomes the anchor for everything that follows—design, budgets, contracts and the financial model.

Behind that number, however, there is always some uncertainty, driven by solar resource, model assumptions, input data quality and site-specific effects, including soiling, snow, shading, clipping, thermal behavior, degradation and curtailment assumptions.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Uncertainty represents different things and different challenges, depending on who’s looking at it. For engineers, uncertainty is a design constraint. For investors, it is a probability distribution that frames expected returns. For lenders, it’s credit risk.

Once we start acknowledging uncertainty, the important question arises: what do we do with it?

Simply reporting uncertainty is rarely enough. Let’s look at why actively reducing uncertainty is more effective.

The same uncertainty, three different interpretations

Engineers ask: ‘Can I optimise the design with confidence?’

Engineers use yield estimates to make dozens of decisions that affect performance and cost: DC/AC ratio, inverter loading, tracker geometry, row spacing, string design, terrain adaptation, cable sizing, clipping strategy and loss assumptions. For engineers, uncertainty isn’t just a reporting issue. It determines whether the project is optimally designed.

When uncertainty is well understood and credibly low, engineers can push toward an optimised design. When uncertainty is vague, they fall back on conservative ‘safety’ decisions, often without realizing what it costs.

If PV engineers overdesign, they are adding capacity or equipment to protect against unknowns, such as extra DC, larger margins and conservative layouts. If they underdesign, they are leaving energy on the table because the model doesn’t capture key effects, for example clipping peaks, complex shading, seasonal soiling, snow and bifacial albedo dynamics.

LCOE (levelised cost of energy) is the engineer’s reality check. Engineers compare variants by looking at how LCOE shifts when they change layout, equipment or assumptions. Uncertainty matters because it affects how confidently they can say: “This design produces more net energy,” or: “That extra cost really pays back.”

If uncertainty is high or poorly characterised, the optimisation loop breaks: it becomes harder to justify tighter spacing, higher DC/AC ratios, or more aggressive design choices, even when they’re actually optimal.

Investors ask: ‘How wide is the range of outcomes and how resilient the returns?’

They invest in a probability distribution. The P50 yield represents the most expected case, but investment committees care about how returns behave in downside conditions, especially under tighter financing, higher capex or weaker merchant pricing.

That’s why projects often speak in either P50—’expected’ yield, including median or mean, depending on convention—or P90—conservative yield with 90% confidence (probability of falling short).

Return on Equity (RoE) is often presented as a single figure, but a more realistic view is a band:

- P50 RoE: what the project should deliver under base-case energy

- P90 RoE: what the investor can expect in a downside production case when all else is equal

Even modest changes in yield uncertainty can widen the gap between those two—and that gap is often where investment risk ‘lives’.

The bottom line for investors: yield uncertainty reshapes return confidence. It’s not only: “how much money do we make?” but: “How much can returns degrade before the story breaks?”

Lenders ask: ‘Can the project repay debt under conservative assumptions?’

Banks translate uncertainty into one core question: Will the project reliably service debt? One of the key metrics is usually debt service coverage ratio (DSCR). In simple terms, DSCR measures a project’s ability to generate sufficient income to cover its debt service.

Lenders typically evaluate DSCR using conservative production assumptions—often P90—and then protect themselves with structure. This is where the lender perspective is often misunderstood. A critical nuance: lenders don’t usually ‘apply an annual uncertainty discount’.

A common instinct, especially outside project finance, is to treat uncertainty as a recurring cut on production, for instance “reduce output by 8% every year”. In real project finance, that approach is often too blunt. If you reduce production every year across a 20–25 year horizon, you can materially damage DSCR, LLCR (loan life coverage ratio), and equity returns. That can make projects look non-bankable on paper, even if the risk can be managed more intelligently.

Overall, lenders and investors often focus on scenario analysis rather than arguing over a few percentage points of PV yield.

Bottom line for lenders: uncertainty is real, but it’s usually managed through financing structure and covenants, not by mechanically reducing energy every year in the base case.

Reducing uncertainty versus merely reporting it

This is where the difference between reporting and reducing uncertainty becomes practical. Reporting uncertainty improves transparency, but it doesn’t stop stakeholders from acting defensively.

Engineers keep conservative buffers, investors discount the downside and lenders structure for protection. Reducing uncertainty changes the conversation because it narrows the gap between ‘expected’ and ‘bankable.’ That can improve design confidence, strengthen downside returns and create more headroom in financing without changing the site, technology or market.

A simple example shows the mechanism. Imagine a utility-scale solar project with a defined expected P50 yield per year. In a ‘do nothing’ approach, total yield uncertainty might be relatively high, placing P90 below other similar projects. The project may still be financeable, but only just; the lender sizes debt to keep DSCR above the minimum threshold, and the investor’s downside return looks modest.

Now consider the same project where the team invests in better data and more realistic modelling, reducing the level of uncertainty. The P50 stays the same, but P90 rises. Nothing physical has changed, only confidence.

Yet that shift can be enough to improve DSCR headroom and strengthen the downside return case, which can translate into slightly better leverage or reduced equity requirement. Even small improvements can matter because the whole capital structure is built on conservative cases.

What does ‘reducing uncertainty’ usually mean in practice?

It means improving the parts you can control. Interannual variability cannot be eliminated, but uncertainty in irradiance inputs and simulation assumptions can often be reduced with relatively low friction.

That typically comes from using validated, high-quality solar datasets over long time periods, moving beyond typical-year averages where possible, and using modelling approaches that better reflect real plant behaviour and losses. In more complex regions, adding site measurements and local validation can further tighten confidence.

The takeaway is that PV yield uncertainty is not a technical footnote. It influences engineers through design conservatism, investors through downside confidence, and banks through bankable energy assumptions.

Reducing uncertainty can change how precisely engineers can optimise, how defensible the investment case becomes and how efficiently lenders can finance the project.

Practical ways to reduce PV yield uncertainty

- Use proven, validated solar radiation datasets, such as long-term satellite-based time series and ground validation where available).

- Use long-history time series to understand interannual variability; it’s not enough to rely on TMY).

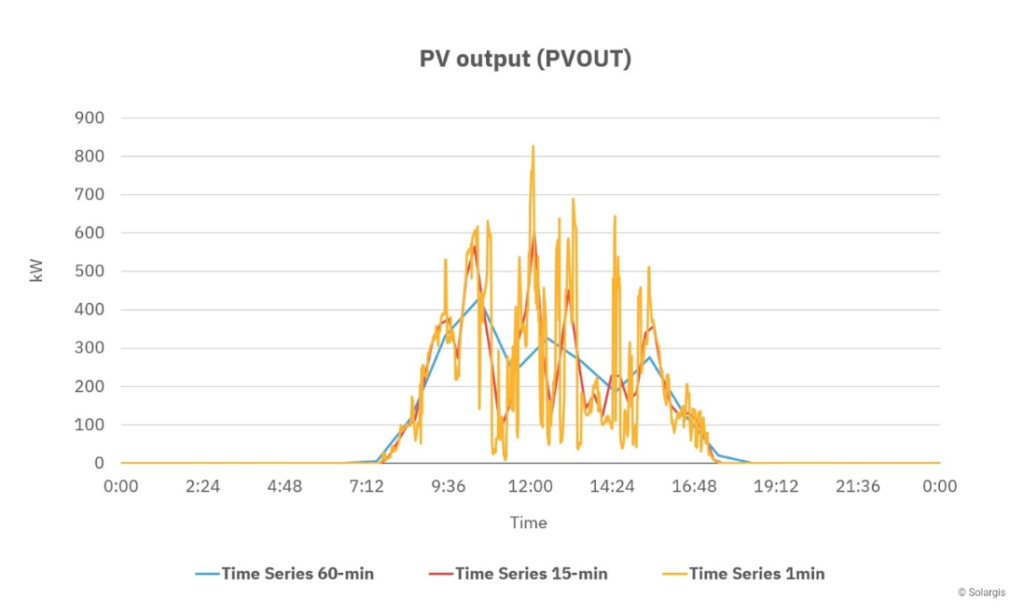

- Use higher temporal resolution when relevant, at the sub-hourly level, to capture clipping, peaks and thermal dynamics.

- Model optical losses with advanced methods where complexity warrants it, such as raytracing in challenging layouts.

- Replace fixed ‘rules of thumb’ losses with physics-based models where possible, including soiling, albedo and temperature.

- Validate component datasheets and ensure model parameters match what will be installed.