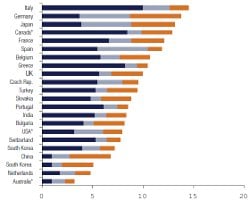

Predicting what will happen to the global PV market is very nearly an impossible task. Its underlying principles are very similar to the dozens of other electronics markets that IMS Research studies, but the key difference in the PV industry is the very close link to, and ultimate dependence on, government policy. In a few years’ time, the introduction, halting or change (or rumoured change) of a single government’s PV policy will have little effect on the global industry, and the huge swings in demand will be less common and less severe. The reasons for this are clear. First, because of geographic diversification in the industry, a single country will account for a smaller portion of the global total (unlike in 2011, when Germany and Italy accounted for more than half of global demand) and thus individual governments’ policy changes will have a smaller impact. Second, if system prices continue to drop rapidly (and IMS Research believes they will), a growing number of regions will achieve the ‘holy grail’ of grid parity and will thus no longer depend solely on government policy to drive their markets.