By Klaus Eberhardt, Technology Manager for Photovoltaics, M+W Group; Peter Csatáry, Head of the Global Technology Services Group, M+W Group

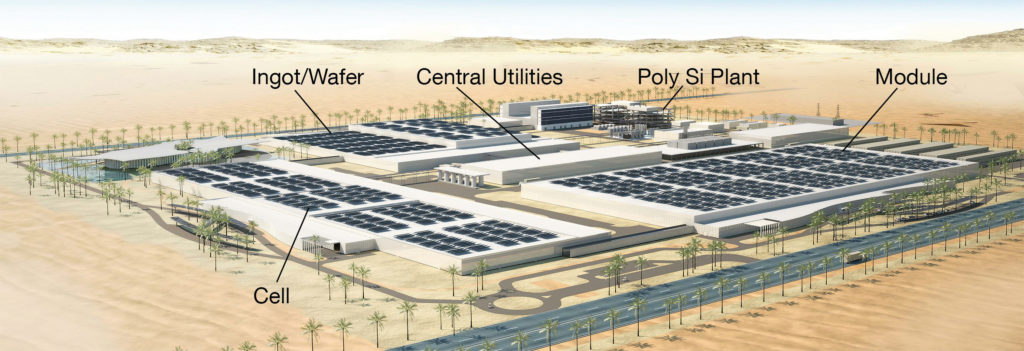

The PV manufacturing and technology hubs established over the past decade will change at an accelerated pace through the globalization of solar power installations. This development will be most pronounced in regions with high solar radiation, where grid parity can be achieved without subsidies. It can therefore be expected that parts of manufacturing within the PV added-value chain will also be established in new markets, such as South America, Africa, the Middle East and Asia. This trend will also stimulate these economies by the generation of new employment opportunities in the advanced technology sector. During the development of a new business plan, the key factors to resolve include the optimum manufacturing size and the extent to which upstream integration, from module manufacturing to poly Si, will be competitive. This paper addresses technology trends and strategic considerations for optimally selecting a PV manufacturer's strategy for each region, the determinants for centralized versus decentralized manufacturing, and the impact of these on fab and facilities concepts. Furthermore, the dependence of manufacturing capacity on fab and facility cost, as well as on the energy demand for individual manufacturing steps along the value chain, is discussed and compared.