Clean energy investment in the US remained resilient in 2025 despite political volatility and accelerated tax credit deadlines under the One Big Beautiful Bill Act (OBBB), according to Crux’s State of Clean Energy Finance: 2025 Market Intelligence Report.

The clean energy financing technology platform estimated that total lending to clean power, fuels and manufacturing projects reached approximately US$120 billion in 2025, up 5.8% year on year. Tax credit monetisation across tax equity, hybrid structures and transfers rose 27% to US$63 billion.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

“Clean energy finance did not stall in 2025; it matured,” said Alfred Johnson, co-founder and CEO of Crux. “Investor appetite in clean energy projects remains strong: aggregate available capital is not the bottleneck; access to well-priced capital is. As the market becomes more selective, clarity becomes the advantage. In 2026, the winners will be those who combine strong assets with superior execution.”

Previously, the report forecast that the US would reach between US$55-60 billion in clean energy tax credit monetisation in 2025, up from US$52 billion in 2024. While tax equity investments were forecast to rise by 10-20% year-on-year in 2025, with between US$32-35 billion.

The “One Big, Beautiful Bill” Act (OBBBA) accelerated the expiration of wind and solar tax credits, requiring projects to begin construction by 4 July 2026 to qualify for safe harbour. According to the report, developers have safe-harboured an estimated 147GW of solar and 23GW of wind generation, for a combined total of approximately 170GW.

Around 70GW of the total – most of which from solar PV – qualified under legacy Section 48 and Section 45 credits and are exempt from Foreign Entity of Concern (FEOC) rules. The report highlighted that this pipeline is sufficient to support several years of deployment, providing near-term stability despite policy tightening.

Capital deployment in 2025

The report stated that despite policy headwinds, investment activity was front-loaded in 2025. Capital deployment peaked in the first quarter of the year as developers rushed to safe harbour projects ahead of policy changes.

While total lending increased, growth slowed compared to 2024, when project finance lending rose 22%. Investment became increasingly selective during the year, favouring experienced developers, advanced projects and traditional solar, wind and storage technologies.

Moreover, utility-scale energy storage emerged as a major growth segment. According to Crux, deployment reached approximately 19GW in 2025, up 72% year on year, driven by falling costs, rising grid volatility and demand from large-load customers.

Tax credit monetisation and hybrid tax equity structures

The report highlighted that total tax credit monetisation reached US$63 billion in 2025, up 27% year on year.

The transfer market alone accounted for nearly US$42 billion, an increase of roughly 48% from 2024. Long-dated production tax credit strips, a collection of tax credits sold collectively, contributed US$8.8 billion in transaction volume.

However, activity slowed in the second half of the year due to uncertainty around tax liabilities and future guidance, leading to modest price softening and greater dispersion.

Meanwhile, hybrid tax equity structures became the dominant monetisation mechanism in 2025, with total tax equity investment exceeding US$36.6 billion, up 22% year-on-year. Hybrid structures represented 68% of the market, compared with 58% the previous year.

Crux observed that more than US$15 billion of tax credits were transferred out of hybrid partnerships into the transfer market. After accounting for transfers, tax equity investors retained over US$21 billion in credits for their own use.

The report said hybrid structures enable more efficient capital recycling and tighter integration between tax equity and transfer markets.

Tech-neutral tax credits and corporate tax buyers

Investment in tech-neutral Section 48E and Section 45Y tax credits remained limited, the report noted, with only 10% of surveyed tax equity investors actively pursuing tech-neutral credits, while 90% indicated interest only under certain conditions. Qualification risks linked to FEOC rules and a lack of clear Internal Revenue Service (IRS) guidance were cited as key barriers.

Crux expects a gradual shift towards tech-neutral credits after 2026 as safe-harboured legacy projects reach commercial operation.

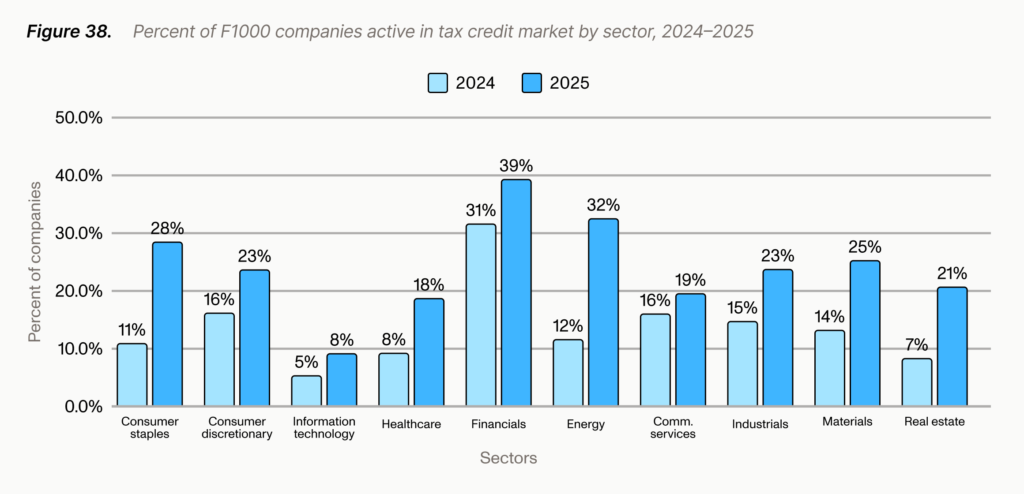

Furthermore, corporate participation in the tax credit market increased significantly in 2025, with nearly 25% of Fortune 1000 companies participating. Mid-cap and small-cap companies also increased involvement, with participation rates of 24% and 15% respectively.

On average, companies purchasing transferable tax credits reduced their effective tax rates by approximately three percentage points compared with non-buyers. Crux said transferable credits are increasingly viewed as a standard component of corporate tax planning rather than a niche strategy.

2026 outlook: a competitive tax credit market

Crux forecasts a more competitive market in 2026, particularly for prior-year tax credits.

As of year-end 2025, between US$8 billion and US$10 billion of 2025-vintage tax credits remained unsold. Many sellers delayed transactions in the second half of 2025 while buyers reassessed tax liabilities amid OBBB uncertainty, the report said.

With larger corporate buyers returning to the market in early 2026, Crux expects a potential rebound in pricing, particularly for solar investment tax credits and Section 45X advanced manufacturing credits. Competition among buyers for a finite pool of credits is expected to drive pricing higher.