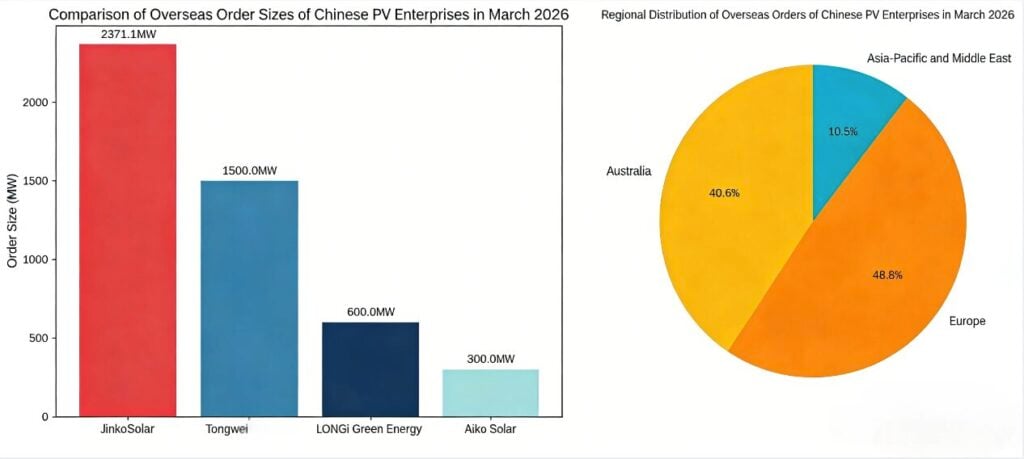

Since the start of March, several leading Chinese PV manufacturers have announced overseas module supply agreements. Among them, Jinko Solar, Tongwei, Aiko and LONGi Green have won gigawatt-scale orders across Europe, Australia, the Middle East and Southeast Asia, with a total contracted volume exceeding 4.67GW.

By regional breakdown, Europe remains the core market, accounting for 51.1% of total contracted volume, Australia makes up 42.5%, and the Asia-Pacific and Middle East regions account for the remaining 6.4%. These trends are shown in the graph on the right below.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Jinko Solar’s performance has been particularly strong, as shown in the graph on the left above. In March alone, the company secured orders in multiple countries including Spain, Australia, New Zealand, France and Japan, with a total volume of 2,371.1MW.

Earlier this month, the company signed a 2GW supply deal with Australia’s Blue Sun Group for its tunnel oxide passivated contact (TOPCon) Flying Tiger 3 module series, making up the majority of its orders in March.

Meanwhile in early March, Tongwei secured a combined 500MW module contract with two Italian partners, followed on 17 March by a 1GW module supply agreement with KENO, Poland’s largest PV distributor.

LONGi Green has further strengthened its position in Europe’s high-value PV market. After renewing a 2GW framework supply deal with Energy 3000 in February, the company won a 100MW order in the Netherlands and a 500MW order in the UK in March, as its back contact (BC) technology gains wider adoption across Europe.

Aiko also notched a breakthrough in emerging markets, securing a 300MW module order in the Middle East and Africa region on 16 March. The performance of China’s leading manufacturers is detailed in the table below.

Towards energy solutions providers

In contrast to earlier fragmented orders, this wave of concentrated agreements represents long‑term, large‑scale and integrated gigawatt‑level partnerships spanning the full value chain—from module supply and power plant construction to energy storage integration and post-construction operation and maintenance (O&M) services.

This is the latest step in the evolution of Chinese PV enterprises from equipment suppliers into full‑service global new energy solutions providers.

Taking Jinko Solar’s partnership with its Australian partner as an example, the two sides have cumulatively shipped more than 1GW over the past three years, and this latest contract underscores their long‑standing, stable partnership.

Notably, fellow PV leader Trina Solar announced on 11 March that its TrinaTracker subsidiary secured a 360MW smart solar tracking system order in Spain. At the same time, its energy storage business has grown rapidly; previous announcements show Trina Solar’s 2026 European energy storage bookings have surpassed 6GWh, with deals signed in markets including the UK, Germany and Italy.

Canadian Solar is also making strong progress in energy storage. On March 17, the company announced that it had signed a 500MW/2.49GWh energy storage system supply agreement with a major US utility for data center grid support, with shipments scheduled to complete by 2027.

Commenting on the order surge, industry insiders note that the PV sector will follow a structurally high‑growth trajectory of “steady acceleration with increasing concentration among top players”, rather than a broader boom affecting all industry players. On one hand, global carbon neutrality goals and the energy transition are long‑term, irreversible trends. The steady fall in PV’s levelized cost of electricity (LCOE) and the growing range of green power applications have laid a firm long‑term foundation for industry expansion.

On the other hand, gigawatt‑scale large orders set extremely high bars for manufacturers’ production capacity, technology, capital strength and overseas operational capabilities. Order flow will keep concentrating toward industry leaders, sparking greater market differentiation and faster phasing out of inefficient capacity, which could lead to healthier industry development.

Notably, China’s PV industry now accounts for more than 80% of global manufacturing capacity. All key technologies across the full value chain—from polysilicon, wafers and cells to modules—are independently developed and controlled. Top players are accelerating overseas capacity expansion by building localised production bases in Southeast Asia and Europe. In addition, companies are upgrading their global expansion models by setting up overseas R&D and service centers to deliver full‑lifecycle operation and O&M services, further boosting customer loyalty and brand value.