With module suppliers currently seeking to hit annual shipment volume guidance for 2020, and many announcing ambitious expansion plans for 2021 and beyond, the sector is seeing a shift now in terms of module supply to global utility-scale sites.

The PV industry is still somewhat fixated by module shipment numbers, and not company financial health. This year in particular, there has been a much greater reliance on arms-length business arrangements with peer-based companies through the value-chain, rather than the traditional goal of owning as much of the production in-house within company-run factories.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

This article explains how this has contributed to a smaller group of module suppliers now commanding premium A and B-Grade ratings in the Q4 2020 release of PV ModuleTech Bankability Ratings report.

Additionally, with the focus now shifting to 2021 and sector expectations, some of the key issues impacting module suppliers over the next 12 months are presented and discussed.

Who-makes-what in a maze of Chinese MoUs, JDAs, JVs & quid-pro-quo’s?

The PV industry is rife with outsourcing and OEM arrangements, especially when it comes to Chinese producers and Japanese/Korean entities. The other main category that has played in the OEM supply game are distributors (typically in Europe and the US) that serve some of the smaller domestic rooftop markets; and in the past SunPower.

The Japanese/Korean use of OEMs is very different to the Chinese tactics of course. Typically, Japanese companies have resorted to full OEM rebadging once in-house manufacturing has been terminated, leaving only a ‘brand’ name to work from. With the exception of Hanwha, Korea-PV can often be seen as Japan-with-a-time-lag. Once module supply becomes a combination of module-only assembly and third-party produced modules, it is hard to see how this is anything other than a short-term model.

The Chinese approach to manufacturing is far more fluid of course, with in-house production and third-party supply often changing quickly, with almost none of the major companies seeing 100% in-house ownership from ingot-to-module as a top priority now.

In some ways, this is understandable. If you have 20-30-GW ‘pure-play’ wafer and cell producers in China, why would you not use these companies as and when needed? The problem however is that in-house audit trails get corrupted the more this happens. Furthermore, the so-called ‘pure-play’ wafer and cell makers are far from stand-alone within China, but more embedded in the fabric of the domestic PV culture that largely works in unison to dominate global production market-share.

During 2020, there has been a deluge of announcements from Chinese companies regarding capacity expansions and JV’s with like-minded value-chain companies. It has led many to a rather naïve knee-jerk conclusion that the sector will collapse under the weight of over-capacity.

This conclusion is erroneous, and misleading. Any industry can be top-heavy with capacity. It is only when production (not capacity) goes into an oversupply situation that issues happen such as pricing volatility and excessive loss-making. Somewhat against all odds today, the PV industry is not in an over-production situation, mainly because Chinese supply of polysilicon and glass was out of synch during the second half of 2020.

Chinese module suppliers are saying this will not change in 2021, and module pricing will remain stable. Well, they would say that, wouldn’t they? Nine-times-out-of-ten in the past few years, the opposite has happened, and module ASPs have come down. Expect this to happen in 2021, and any materials supply tightness in China to end. China is very good at hitting the build accelerator when raw materials are needed to support domestic manufacturing. Why should 2021 be a year of moderation?

All these announcements and inter-company dealings however do make it hard to know who-made-what, and not simply at the key wafer and cell stages. Differentiating between module line production by contract/OEM/in-house use and module shipment by OEM/own-brand is a major challenge today. When one factors in cell/module manufacturing country-of-origin, the issue of China-made or Southeast-Asia made then adds an extra layer of complexity to US module buyers, as the only major import tariff in play globally today is the 2012 CVD/AD ruling.

At the start of 2021, I will return to the above issues more, mainly to form a picture of what in-house own-brand module supply will look like next year, and which module suppliers will dominate the global utility space. By default, this will include 2020 rankings.

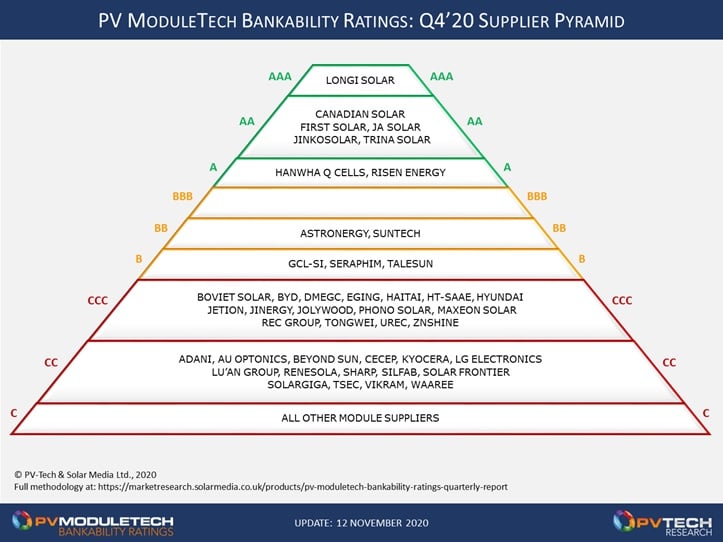

Let’s look now at module supplier bankability standings at the end of 2020, with the first showing of the PV ModuleTech Bankability Ratings hierarchy pyramid for Q4 2020.

Fewer module suppliers in top ratings bands should not be a surprise

As the PV industry has moved well into the 100-200 GW annual demand phase – and the majority of this is coming from utility-scale solar deployment – the barrier-to-entry to be considered a viable supplier to 100-500 MW sites is something that only a small handful of companies can satisfy.

Indeed, when the supply universe for a module supplier becomes the global end-market (in particular excluding China and India) and participation in the US market is a must, then the list of prospective module suppliers is reduced further.

It is these criteria that have caused a change in module supply dynamics in the past few years, and this can be seen most clearly in the Q4 2020 pyramid below.

Of course, the Bankability Ratings is not based simply on module supply or shipments. It is based on a combination of Manufacturing Strength and Financial Strength. Each of these parameters is a host of quarterly-updated and trailing-quarter-blended metrics, all benchmarked across the sector every three months. But there are some key must-have’s that differentiate the top players, in particular today those companies in the AA and AAA bands (just six module suppliers).

Without global shipments in high-volume for utility deployment, it is impossible to be in the top bands. And rightly so, these module suppliers are never in the mix for 100-MW-plus projects. If all shipments are domestic (e.g. Chinese module suppliers with capacity only in China and shipments only in China, or ditto for India), then these companies will never be selected for supply to overseas projects (at least where investor due-diligence is involved). And finally, if the company is technically-bankrupt, one would imagine that most investors would walk away (although gutter-pricing and the lure of third-party warranty insurance may work short-term).

This explains why so few module suppliers are in the top bands, and the most-populated is actually the one at the very bottom above (the bottom ‘C’ rating). This is often where people consider a shake-out to be occurring within the sector, but this is wrong and generally just driven by media coverage. (Remember the ‘famous’ thin-film shake-out and the fact that the 100 companies that went bankrupt had barely made any product?)

The key area to track is where the changes are in companies being selected for 100-500 MW supply deals globally, and what these module suppliers are doing in terms of technology, in-house productivity, cell/module capacity outside China, and if the company’s books are in order.

In this regard, we are seeing a bifurcation of sorts occurring in the bankability pyramid, and potentially a maximum of 5-6 module suppliers being in the mix for the major PV projects outside China and India in the coming years. And leaving the rest of the industry to play in their domestic markets with smaller sites (and rooftops) befitting the supply levels on offer to them.

Why bother competing in a 5MW rooftop annual segment, when the real prize is 10-20GW of 50-MW-plus global utility deals? Higher margins from rooftops sound great, but if the supply volumes are 1-2% of utility project volumes, the served market is basically irrelevant.

In looking at the pyramid above, LONGi Solar remains the only AAA-Rated module supplier. What differentiates e.g. LONGi from other AA players is not shipment/manufacturing strength, but the company’s cost structure and valuation (market cap relative to total assets), and minimal exposure to debt. Going into 2021, there are still no red flags for LONGi in this regard.

Possibly, the only thing to watch is how the rest of the industry – in particular fellow global module suppliers at the multi-GW plus level – addresses its own long-term mono wafer supply.

I have discussed frequently in the last couple of years that being a supplier and competitor at the same time is not something that can be sustained in the long run. At some point, it may even benefit LONGi to carve out its wafer and module business units into separate listed entities in China.

At some point, a decision likely needs to be made whether the end goal is to be a leading material commodity supplier wholly in China (wafers) or a global international end-market brand supplier (modules); one suspects it is the latter one. In fact, to be successful long-term for each of these activities has a different business model, and likely just too hard to do under the one roof.

Module suppliers falling into the CCC and CC Rating bands of the Q4 2020 pyramid make up a mixed bag, with many different types of companies here. Some are newly-created variants of older household names that had been struggling financially for some time (Maxeon/SunPower, UREC/NSP, for example).

There are still legacy entrants (mainly Japanese) that cling onto listings by virtue of past-performance and OEM deals. And then there are those that exist for domestic business only and have limited play overseas (some of the Chinese and Indian entrants). The Q4 2020 may indeed be the final time we see them in the AAA-to-CC named entities within the quarterly pyramid.

The main thing however is that there is now daylight between the top grouping and the rest of the sector, and this is perhaps what one would expect when comparing a circa-150-GW demand sector with the industry as it was just a few years ago.

What to watch for in 2021, in terms of module supply

Moving into 2021, module supply will look much like 2020 in fact. The shift to a mono-PERC dominated landscape is still in its final phases. Any new capacity additions of importance from the leading players will be mono-PERC; the only question being the cell sizes used and the module format sizes built. But the technology is not a moving target now – mono-PERC is utterly dominating the industry now and will do through the whole of 2021.

Getting to grip with cell and module capacity needed outside China will be a key thing to watch in the coming months, especially for those Chinese companies wishing to compete in the US market but unable to do so until now owing to being China-only producers.

The other thing to consider is whether having relied in the past on Vietnam OEM module supply is possible going forward. The Vietnam OEM route was only ever going to be a short-term play, and subject to risk at any point. It is still a house of cards that could collapse any time.

The first half will be about keeping gross margins in the low double-digit range (at least for Asian c-Si supply), before seeking to move this closer to the desired 15-20% range in the second half. With the industry heavily second-half weighted next year in terms of shipments/demand, all the net profits will likely come in Q3’20 and Q4’20 on the back also of further cost-savings done in the first half but not as yet showing meaningful dividend.

In terms of the pyramid rankings, it is not impossible that a group of 5-6 suppliers will occupy the AAA and AA Ratings bands at year-end, with every other supplier CCC or below. If this does look like happening, then it will certainly require some other way to differentiate the also-ran’s. Although, if you look closely at the module suppliers currently in the CCC and CC bands above: realistically, when do they ever compete with one another?

If module suppliers do not complete with one another, there is no point in benchmarking them.

More than likely, it may be necessary to introduce further benchmarking across the top players. We have started to do this within the full PV ModuleTech Bankability Ratings Quarterly report, which explains all the module suppliers individually, and then benchmarks the top players across a wide range of manufacturing and financial metrics/ratios.

The more the industry sees a small group of 5-6 companies supplying all the major investor-financed projects globally, the more there is a need to increase the analysis and benchmarking of these players, at the expense of what I referred to above as the also-ran’s.

Anyone interested in accessing the full PV ModuleTech Bankability Ratings Quarterly report can complete the request form at the report weblink here.