With many of the top-20 module suppliers to the solar industry now having multi-GW shipment volumes, attention has turned firmly to assessing metrics that companies can use to benchmark the quality and reliability of shipped products against their competitors.

Almost every week, a different module supplier sends out marketing collateral claiming to be top of a table or the highest in a ranking, performed by a third-party body. It is extremely confusing to those immersed in the daily production analysis of the module suppliers/producers in question: far less, the downstream companies that have to make module purchasing decisions from a less informed perspective.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Indeed, almost every trade show these days seems to have a ‘quality’ workshop or forum bolted on with a different subset of stakeholders, where inevitably the conversation drifts to the difficulty in balancing site capex with project viability, purely from a build perspective.

The backdrop to this confusion has been a major factor in PV-Tech deciding to launch the PV ModuleTech 2017 event, in order to get clarity and informed discussion on these issues, and subsequently propagated through the PV-Tech.org portal to explain to the global solar audience what is really going on, and the issues that are important for correct module selection for major solar investment projects.

Are we moving towards any industry standards?

The range of third-party bodies weighing in on the quality issue has certainly grown in the past few years, and perhaps not unsurprisingly given the growth of the industry and the investor profile that fuels the utility segment (in comparison to rooftop driven segments that were the main driver in the feed-in-tariff days of early solar growth).

As soon as solar became an asset class, all issues related to component selection – including the modules, the materials used for the module assembly stages, and plant design and maintenance – then moves to a different level, and this can be seen clearly today for utility-based solar sites.

Many different labels are being used by module suppliers, including third-party certification, test-and-inspection, bankability studies, factory audits, and purely academic studies such as the misleading Tier-1 tables often disseminated in the public domain. Some companies combine different aspects of these, but as yet, it is fair to say that an industry-wide standard has not emerged as to the definitive or ‘gold’ standard that all companies should strive towards.

Sub-contracting & OEM outsourcing is still the bigger issue

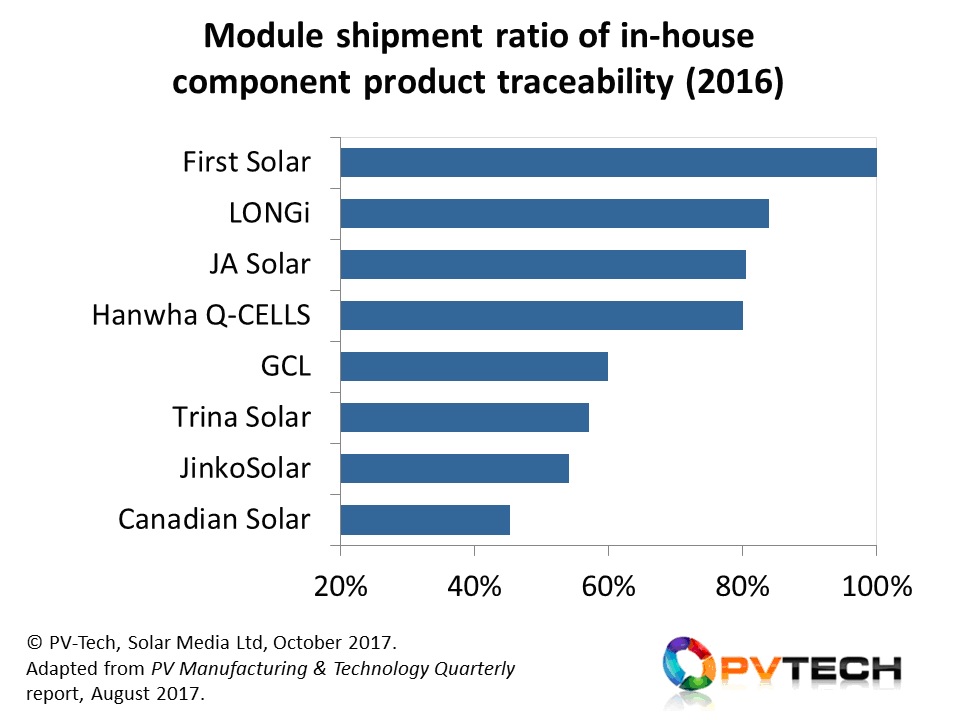

With factory audits and module inspection being a key feature of any quality/bankability study, and featuring in most of the third-party assessments of module suppliers, we are compelled to return to one issue that is still muddying the waters for many of the leading c-Si module suppliers: in-house component production.

How can rankings of suppliers be done with accuracy when so much of the key components (wafers, cells and modules) are outsourced at levels that change considerably across any given calendar year? Even if one was to label wafers as raw materials consumables (which they are certainly not), then we still have the fundamental issue of contracted module assembly, where a factory audit of the module supplier selling the product becomes almost superfluous.

Therefore, one could argue that as a starting point, ‘quality’ is by default heavily weighted to those companies that have production and materials supply ownership over the greatest fraction of their shipped modules. This is a key topic that has become somewhat lost in the past few years, with so many fixated on GW-levels of annual shipments, and so many project developers and EPCs are essentially blind to this, not to mention the asset owners and managers of acquired as-built sites.

In this context, we decided to do some new analysis based on the leading module suppliers that will be speaking at PV ModuleTech 2017, in Kuala Lumpur on 7-8 November 2017.

First, let’s return to the module supplier rankings by shipment for last year, where we ranked companies purely from a shipment standpoint for global, China-only, and Non-China markets.

Excluding Yingli Green and Wuxi Suntech (that have less presence outside China now compared to other Chinese global module brands), the only companies from our listing above that are not yet confirmed to be speaking at PV ModuleTech are SunPower, SolarWorld and REC Solar.

However, having the leading eight modules suppliers globally explain how their product supply is ticking all the boxes that are being used by the certification bodies, test houses and independent engineers is almost certainly a first for any global conference in the solar industry, and will be a massive takeaway for all the EPCs and project developers that are set to be in the audience in Kuala Lumpur on 7-8 November.

Therefore, as a starting point, we confine our ‘in-house’ production statistics here to the leading eight module suppliers that are shown above and will be delivering key talks at PV ModuleTech.

Explaining the methodology

Firstly, we need to standardize c-Si and thin-film, with First Solar the only company in our ‘quality’ module grouping here that is based on thin-film.

The obvious way to do this is to treat polysilicon like glass, and then basically the thin-film production line is doing the c-Si equivalent value-chain roles of ingot/wafer/cell/module.

Another way of looking at this is from the other perspective. A thin-film fab in the c-Si world would have ingot/wafer/cell/module production all in one building and 100% in-house supplied/produced, so that only chunks of polysilicon were going into the factory, and only finished modules would be going out. The closest we ever got to this actually happening was the REC Solar concept in Tuas, and currently can be seen in Adani’s mid-term strategy at Mundra.

The only subjective point comes down to the significance or weighting placed on using in-house/third-party ingots, wafers, cells and modules, and one can make arguments one way or another on this. We chose a simple pathway here that is by no means conclusive, but serves to explain the key message visually.

Wafer supply was selected as the least sensitive, with cell the most important, and modules somewhere in between (although it can be hard to really know whose cells are being used when the modules are being completely outsourced and simply rebranded by the final seller to the EPCs or installers).

So we based the rankings of in-house production ‘quality’ based on wafers, cells and modules only, and then used this weighted number as a fraction of the final module shipment levels from the companies.

The results of this are shown below now:

A key factor in some of the leading names having lower percentage rankings in the above graphic can be traced back directly to the individual companies’ strategies to gain market-share and show investors year-on-year shipment growth figures, backed up by having global branding status that remains the exclusive domain of no more than 20 module suppliers globally today.

The conclusions from the above analysis should certainly be factors that feed into any third-party exercise that then looks at directly measurable factors across component production, material selection, module testing and other supplier bankability factors.

Gathering the key stakeholders at PV ModuleTech 2017

In setting out the main objectives for PV ModuleTech 2017 in Kuala Lumpur on 7-8 November, we knew that the event would work best only if the key stakeholders across all the module-related categories above were the ones giving the talks at the event, and this focused us on company and speaker selection from an invited-basis only.

In this respect, the event is set to fill the clear ‘gap’ in the solar events calendar for understanding exactly what is meant by module ‘quality’ and ‘bankability’, and has to be a golden opportunity for major solar developers, EPCs, O&Ms and asset owners to get completely up to speed with exactly what types of modules will be used on the large utility-based solar farms that will be constructed during the 2018-2020 period.

The image below shows the main companies speaking at PV ModuleTech 2017, with a further 4-5 to be added in the next couple of weeks, completing the full complement for the event in November.

The 2-day agenda for PV ModuleTech 2017 can be seen by using this link. There are just a few companies and speakers to be added before the final agenda is fixed down.

To get involved with PV ModuleTech 2017, to learn more about the event, or to register to attend the event in Kuala Lumpur, Malaysia, on 7-8 November 2017, please see the event website here.