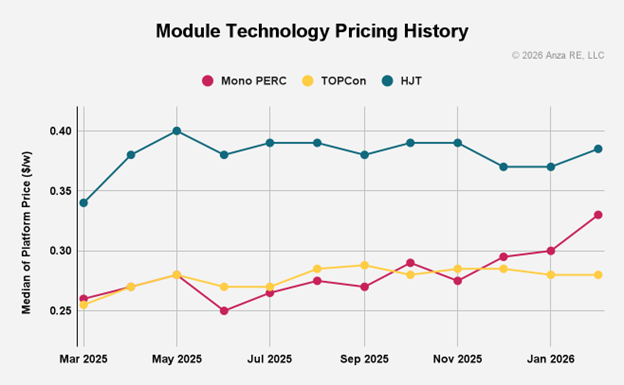

Monocrystalline passivated emitter rear contact (PERC) modules saw a 20% increase in average price in the US between November 2025 and February 2026, as the pricing balance of the US solar sector changes rapidly.

This is a key conclusion to be drawn from Anza’s latest report into the US solar and battery energy storage system (BESS) sector, published this week. While the general solar module price remained relatively stable in February, only increasing marginally form the US$0.28/W reported last November to US$0.285, Anza notes that this obfuscates significant changes in both the price of different solar technologies, and the role of US-made versus overseas components.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Most notably, mono PERC modules hit US$0.33/W in February, up from US$0.275/W in November, and up from US$0.3/W as recently as January. This means that mono PERC is now significantly more expensive than tunnel oxide passivated contact (TOPCon)—which saw module prices fall marginally to US$0.28/W—while heterojunction technology (HJT) remains the most expensive technology type. These pricing trends are shown in the graph below.

Anza said that this is the first time that mono PERC has been more expensive than TOPCon—“outside of a brief anomaly during last summer’s Safe Harbour rush”—and can be attributable to an increased demand for domestically produced modules, many of which are PERC, ahead of the 3 July investment tax credit (ITC) safe harbour deadline. There was a similar rush to advance projects before an earlier deadline, on 31 December 2025, and both periods highlight how the deadlines imposed by the Trump administration to meet the deadlines required to receive ITC support for solar projects has had an impact on project development and module purchasing trends.

The analyst also suggested that some of the long-running patent disputes in the TOPCon field, which saw many of the industry’s leaders plunged into legal battles that are still ongoing, could have encouraged developers to look to other technologies for their modules. As demand for PERC modules, a more established technology than HJT, has increased, so too has the price of these panels.

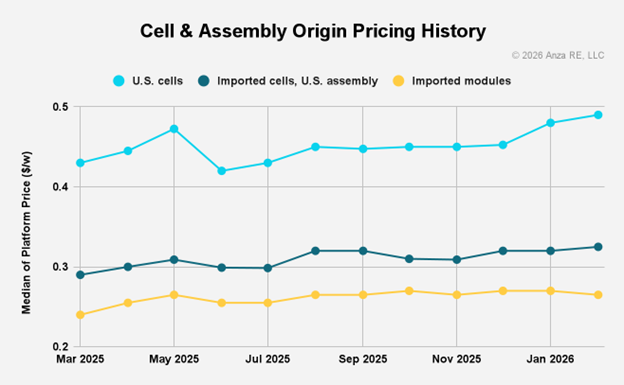

Price of US-made solar cells up 8.2% since November

The appetite to secure domestically made goods has also impacted the price of those components compared to their overseas counterparts. Anza notes that the price of a solar cell made in the US has jumped 8.2% between November 2025 and February 2026, reaching US$0.49/W, reflecting increased demand for US-made cells so that projects can comply with domestic content rules.

Similarly, the integration of cells made overseas into modules made in the US has been a cornerstone of many companies’ efforts to meet domestic content bonus credit thresholds, considering that the US has far more operational module producing capacity than cell manufacturing capacity. This is reflected in Anza’s data, where cells imported from overseas, which are ultimately integrated into US modules, saw their prices increase 4.9% to US$0.325/W in February, up from less than US$0.3/W a year earlier.

Meanwhile, imported modules saw their average price trickle downwards to US$0.265/W in February, which Anza attributed to “continued global overcapacity”. Anza said that February saw “multiple major policy risks converge simultaneously”, yielding the component prices by country of origin as seen in the graph above.

More storage manufacturers, more stable prices

There is a similar trend in the storage sector, where developers are keener than ever to use US-made components in their projects, driving demand for new manufacturing capacity. Anza expects the number of domestic solar cell manufacturers to increase from 12 to 15 by the end of the second quarter of this year, but the number of operational BESS suppliers to more than double, from six in operation at the end of the first half of 2026 to 13 by the end of the first half of 2027.

BESS prices, however, remained more stable than in the solar sector. The Anza report splits batteries by size and scale, and shows that distributed generation-sized projects—specifically a 10MW, 4-hour AC wrap system—saw a “modest” 3.4% decline in price between November last year and February this year. This type of battery ended February with an average price of US$203/kWh.

For larger systems—specifically a 200MW, 4-hour AC wrap system for use in utility-scale projects—the price fell by 8.6% since November 2025, but remained stable since January 2026. The price of this type of battery hit US$178/kWh in February.