By Markus Fischer, Director of R&D Processes, Hanwha Q CELLS GmbH; Alexander Gerlach, Senior Specialist, Hanwha Q CELLS GmbH

The crystalline silicon (c-Si) module price has been fluctuating slightly around the US$0.72/Wp level for the last 18 months. This pricing, at an estimated cumulative PV module shipment volume of 149GWp, indicates a trend change for the PV industry. C-Si module pricing appears to be currently above the production cost and should therefore yield a profit margin. However, there is still a mismatch between manufacturing capacity and future market demand. A closer look at the pricing figures reveals that there is no indication to give the allclear during the ongoing consolidation process in the PV industry. C-Si module pricing is not reflecting the

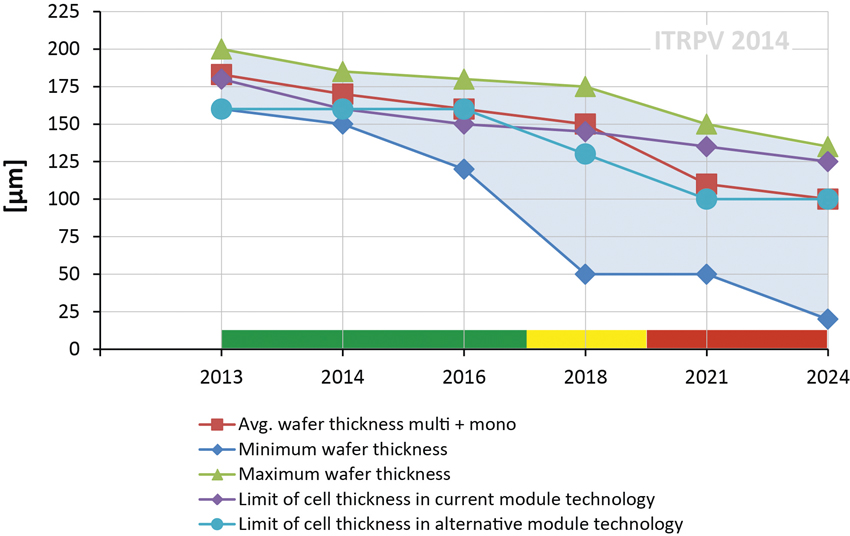

increase in polysilicon and wafer prices, and therefore the pressure to reduce the cell and module conversion costs remains a looming fact. This paper describes state-of-the-art c-Si cell manufacturing solutions that are in line with identified trends in materials, processes and products recently published in the 5th edition of the International Technology Roadmap for Photovoltaic (ITRPV). Currently available c-Si cell technologies offering higher efficiencies as well as materials savings will be discussed. The need for implementing these technologies in mass production without significantly increasing the cost per piece and in the face of more complex manufacturing processes will be established. The findings of the ITRPV regarding the reduction in levelized cost of electricity (LCOE) will be discussed, leading to the conclusion that contemporary cell technology supports the long-term competitiveness of PV-based power generation.