To uncover the story behind the evolving top ten PV module manufacturers (by shipments), we must first understand the forces that have shaped today’s PV market landscape. For over a decade, PV Tech Market Research has been at the forefront of tracking the PV industry, providing in-depth analysis of production capabilities, shipment trends and financial resilience. The aftermath of a turbulent 2025 has left many companies grappling with a market in flux—defined by oversupply, shrinking profit margins and tightening policy constraints.

Slowing capacity expansion

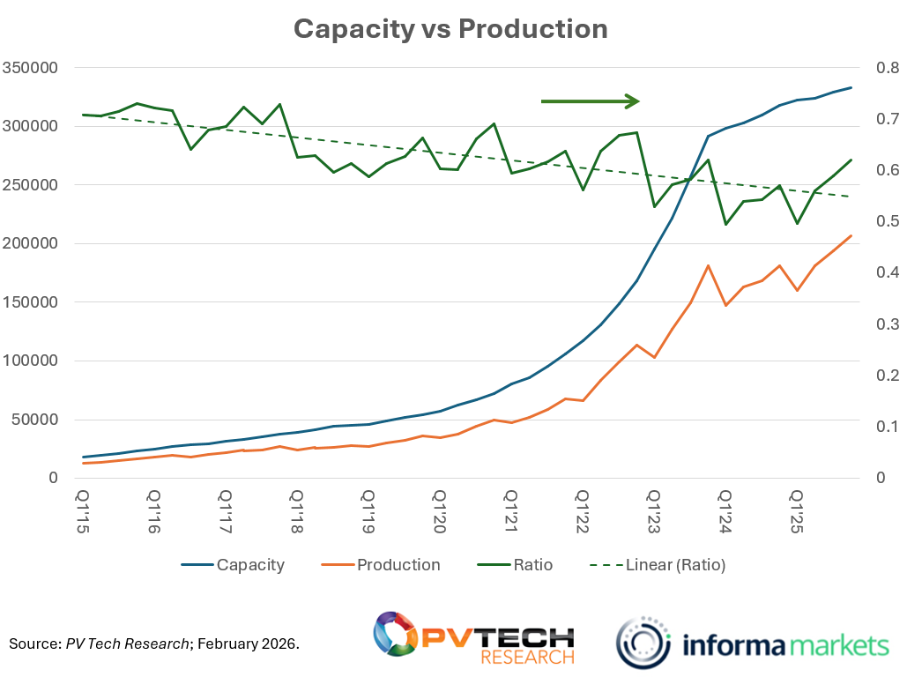

The previous two years have seen a significant slowdown in the addition of new solar production capacity. Up to 2023, the PV industry was experiencing exponential growth in module capacity expansions; this growth has slowed dramatically since Q1 2024.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Much more notable is the issue of utilisation (the ratio of capacity to production output). The utilisation ratio, while cyclical, has shown a clear downward trend, rising consistently above 70% between 2015 and 2018 and now hovering around 60%. To put it another way, today, between 35% and 40% of global solar module capacity is sitting idle. You can see the trend in the graphic below starting nearly a decade ago.

PV manufacturing capacity utilisation has been falling steadily over the past decade. Image: PV Tech Research.

The main driver for this reduction in utilisation is that the industry has pursued capacity expansion to quickly secure market share and maintain control over it. While this strategy benefited the industry, leading to lower prices and accelerated technological advancements driven by competition, it inevitably created a systemic challenge for module suppliers, who are now unable to compete solely on price. Adding to the complexity, the resulting oversupply has prompted many countries to impose market restrictions to either encourage or protect their domestic manufacturing capacity.

The oversupply has led to market saturation across most regions and has now shifted the dynamic into a negative loop of oversupply, where any positive price movement results in oversupply flooding the market, forcing manufacturers to either sell at cost or below it. There are several strategies manufacturers are employing to work around this issue: while many are looking for new markets, others are investing in new technologies such as back contact or multi-junction/perovskites. The choice usually depends on the manufacturer’s size, with smaller players often opting to enter new markets.

Impact on financial resilience

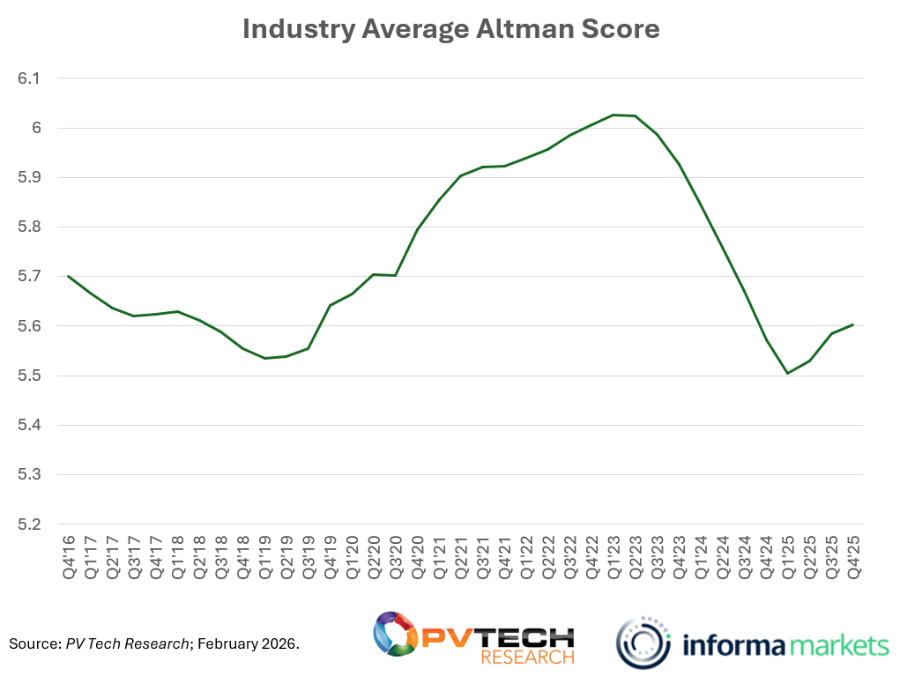

A direct consequence of the new market dynamic has been a significant erosion of financial resilience across the industry. This can be quantified by the Altman Score, a metric that many financial institutions use to assess a company’s resilience and its probability of default. In mid-2023, the average Altman score of the module manufacturers we track in our PV ModuleTech Bankability Ratings Report was over 6; however, it has since dropped significantly, wiping away any additional financial resilience gained since 2019. On a brighter note, metrics have shown improvement since Q2 2025, following multiple initiatives by governments and large players to address the underlying issues.

There are also other signals that the industry has started to recover across the value chain. The most promising indicator came from Daqo Solar, which has seen an increase in the shipment volumes and price of polysilicon. The demand was even high enough to start drawing down the manufacturer’s 2024 inventory stockpile. The market is also much more optimistic about the outlook, with the polysilicon manufacturer’s share price rising substantially.

However, the full picture is not all rosy either. For the first time, our data shows a decrease in polysilicon production worldwide. This is understandable, given that many players simply chose to produce less due to the low prices and inventory stockpiles that have plagued the value chain in 2024 and early 2025.

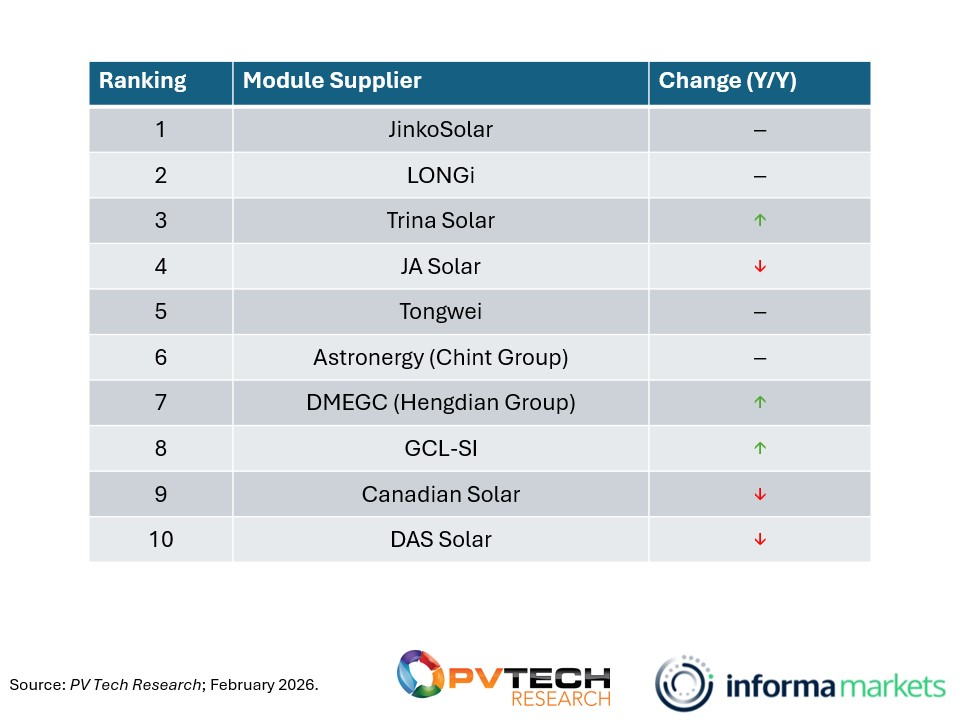

Jinko in top spot with Longi as close second

Compared to the previous year, the top ten rankings in 2025 have undergone notable changes, with one major exception: Jinko retained its position as the top-ranked module supplier for the fourth consecutive year. This achievement comes despite Jinko shipping slightly fewer modules in 2025 than in 2024, according to PV Tech Research’s PV Manufacturing and Technology Quarterly report. Jinko has been the leading module supplier by volume for eight of the last ten years.

LONGi came in a very close second to Jinko, but what stands out most is its impressive year-on-year growth compared to other players. If sustained, we believe LONGi would become the largest player by shipment volume in 2026. LONGi’s rise is particularly interesting as the company seems to have anticipated a downturn earlier than its competitors. After shedding nearly 30% of its workforce in Q2 2024, LONGi achieved an incredibly low-cost structure, giving it greater leverage when negotiating prices for materials and components (especially within Chinese supply chains). Prior to 2024, LONGi had strong technology differentiation; however, that has eroded as the rest of the market shifted toward TOPCon. To regain its edge in a highly saturated market, LONGi is now focusing on back contact technology, aiming to reestablish its position as a leader in innovation.

In the third and fourth quarters, there is a clear shift between Trina and JA Solar. While Trina saw the second-largest increase in shipment size among the top ten manufacturers, JA was in contrast the only company in the top five to see a marginal reduction in shipments. This dynamic allowed Trina to claim the third position, overtaking JA Solar.

In fifth position is Tongwei, which has emerged as one of the most significant players in the solar industry today. Tongwei started out much further up the value chain but has since integrated vertically, creating a highly resilient business model. However, what sets Tongwei apart isn’t just its vertically integrated supply chain, but the scale of its capacity across every step. Currently, Tongwei accounts for over a third of global polysilicon production, making it the most influential player in the early parts of this value chain.

DMEGC emerged as a new entrant in 2025, prioritising market diversification and displacing Risen from the top rankings. Early on, DMEGC strategically expanded its presence across Japan, China and Europe, while also entering the US market that same year. This diversification enabled DMEGC to redirect shipments in a highly challenging market environment. Currently, DMEGC primarily focuses on Europe and China, but has demonstrated the ability to adapt swiftly as needed. Market diversification has proven to be a critical strategy, and while many competitors strive for it, few achieve the same level of success. However, DMEGC now faces increasing competition in several of its established markets, particularly in India.

In 2025, the top ten module suppliers by volume collectively represented over two-thirds of global module deployments. While some manufacturers in the top ten saw a decline in shipment volumes, the number of solar manufacturers shipping at least 10GW reached an all-time high of 15, with two non-Chinese manufacturers (First Solar and Waaree) highlighting the growing diversification in the global solar market.

Despite a challenging financial year for major Chinese solar manufacturers, the top 10 PV module suppliers still shipped over 500GW of modules in 2025. Looking ahead, 2026 is shaping up to be a pivotal year for mergers and acquisitions, as larger players aim to strengthen their positions through consolidation. Notable examples include TCL’s acquisition of DAS Solar and HY Solar taking over the operations and management of the Suntech brand. This suggests that the long-awaited market consolidation might finally be here.

Ongoing consolidation efforts and other indicators of recovery, point to a more optimistic outlook for 2026, both for shipments and financial resilience. While 2024 and 2025 were challenging years, they represented a long-awaited and necessary market correction in an oversaturated industry. This new stage emphasises stability and sustainable growth rather than relentless expansion, a sign that the industry is entering a new stage of maturity that favours stability over endless growth.

Numbers used for this article include some end-of-year forecasts for 2025, as some manufacturers have yet to release their final end-of-year results.

The Q1 edition of the ‘PV manufacturing and technology’ quarterly report, the definitive benchmarking resource for the PV technology value chain, is out now and available here. Moustafa Ramadan is head of PV Tech Research, Informa Markets.