The European solar module market has reached a “state of equilibrium” in recent weeks, with stable prices and regular demand.

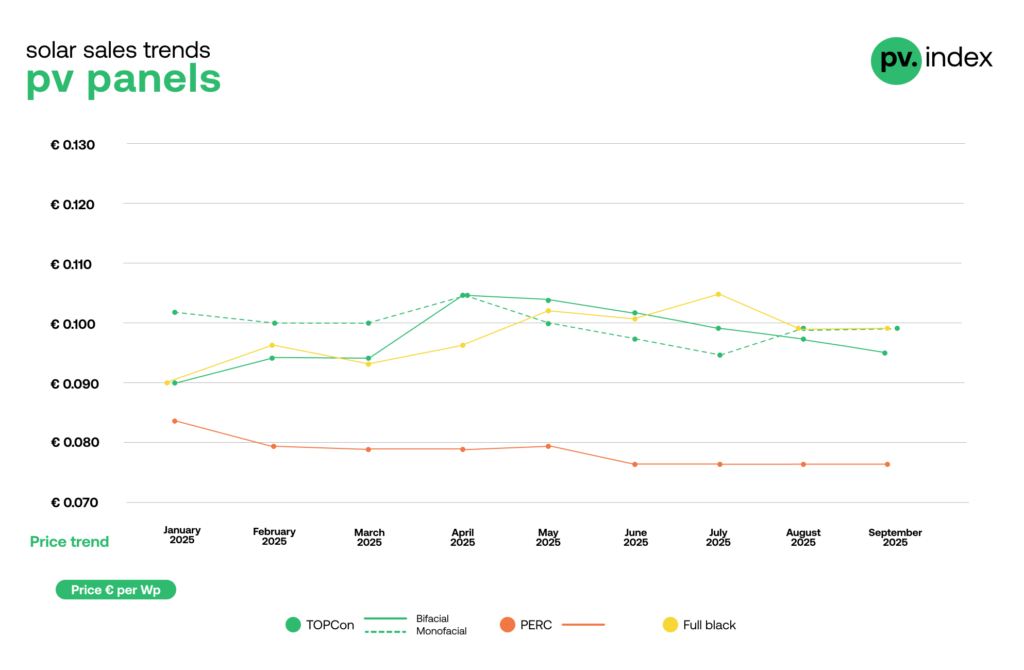

The latest pv.index report from online solar marketplace sun.store shows that prices for passivated emitter rear contact (PERC), monofacial tunnel oxide passivated contact (TOPCon) and full black modules all remained steady in September 2025. The report said that the stability reflected “balanced supply and stable demand” of TOPCon modules and the attraction of cheaper PERC panels for “cost-driven projects”.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Only bifacial TOPCon modules saw a slight, 2% price decline, from €0.097/Wp (US$0.11/Wp) to €0.095/Wp, which sun.store called a “moderate” change after months of stability.

“After two years of rapid price corrections, the sector is now finding balance between production capacity, pricing and demand,” said Filip Kierzkowski, head of partnerships and trading at sun.store.

Sun.store’s Purchasing Managers’ Index (PMI), which gauges buyers’ interest from sun.store users, showed a slight increase in September, from 65 to 66. A score above 50 indicates “positive market outlook” and the overall intention to buy modules among respondents.

Of those surveyed, 45% expect to buy more modules next month than they did last month, while 42% anticipate no change and just 13% expect to buy fewer.

“This rebound suggests that distributors are gradually replenishing inventories after the slow summer months, anticipating steadier Q4 activity,” the report said.

“Stable module prices, slower inverter depreciation, and a modest improvement in PMI together signal a more sustainable market environment,” Kierzkowski said.

Stability in the module market is reflected in the inverter market, sun.store’s data shows, which is “mature” and “characterised by consistent brand preferences and strong customer loyalty among European installers.”

The leading suppliers for both hybrid and string inverters are split between European and Chinese firms. Huawei tops the list of both, followed by Deye, Goodwe, Austria’s Fronius and Sungrow for hybrid inverters and SMA Solar, Sungrow, SolarEdge and Fronius for string inverters.

Leading solar module suppliers

One change in September was the replacement of Chinese solar module producer Aiko in the top five European module suppliers by international solar manufacturer Canadian Solar.

Sun.store said Canadian Solar’s entry into the top five shows both its “strong European footprint” and a “somewhat reduced interest in Aiko”.

The top five list is now as follows: LONGi, JinkoSolar, Trinasolar, JA Solar and Canadian Solar.

“The entry of Canadian Solar into the top five brands and Huawei’s strengthened position in both inverter categories highlight how market leadership is consolidating around a few highly competitive global players. Heading into Q4, the focus will likely shift from price competition to operational efficiency and strategic stock management,” Kierzkowski said.