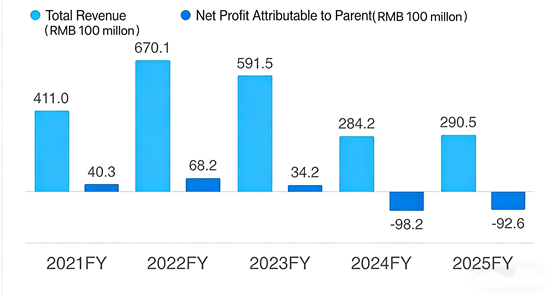

On 25 March 2026, TCL Zhonghuan released its 2025 annual report alongside announcements of executive changes. The company posted operating revenue of RMB29.05 billion (US$4.22 billion), a slight 2.22% year-on-year increase, while net profit attributable to shareholders stood at a loss of RMB9.264 billion. Though losses narrowed by 5.65% from the previous year, the company remained deeply in the red.

Alongside the financial results, the company announced a series of personnel adjustments, including a new CEO and changes to several board director roles. The move signals a strategic refocus and organisational optimisation as the industry navigates a cyclical trough.

TCL Zhonghuan’s sustained losses stem from intensified cutthroat competition in the PV industry. In his address accompanying the annual report, company chairman Li Dongsheng noted that the industry is facing severe headwinds and added that the company will adhere to the principle of “addressing crises through development and seizing opportunities amid adversity”. He emphasised that “market-driven mergers and reorganisations are the inevitable path to breaking the cycle of vicious competition and improving the industry landscape”.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Cell and module business emerges as new growth driver

Wafers remain TCL Zhonghuan’s core business, maintaining the industry’s top market share. Through rigorous cost control, the segment’s earnings before interest, taxes, depreciation and amortisation (EBITDA) improved by RMB1.92 billion yuan year-on-year. Large-format products drove growth, with shipments of the G12 series surging 40.8% year-on-year, aligning with market demand for high-efficiency, high-value products.

The cell and module business emerged as a standout performer, generating RMB9.324 billion in operating revenue in 2025—a robust 60.45% year-on-year increase—accounting for 32.10% of total revenue. Module shipments reached 15.1GW, rising more than 80% year-on-year. By developing a portfolio of high-efficiency products, including back contact and half-cut technologies, and leveraging its dual-brand strategy (TCL Solar and SUNPower), the company has established a competitive edge amid fierce market rivalry.

Li Dongsheng stated that the company will “seize opportunities during the cyclical bottom, leverage its BC patent advantages, integrate existing resources and accelerate efforts to enhance the competitiveness of its cell and module business”.

As the company’s second growth engine, the semiconductor materials business delivered RMB5.707 billion in operating revenue, up 21.75% year-on-year, with both revenue and shipments ranking among the industry’s top tiers.

Facing cyclical industry challenges, TCL Zhonghuan reaffirmed its commitment to long-term investment. In 2025, the company’s R&D spending totalled 1.06 billion yuan, representing 3.65% of operating revenue. By the end of the reporting period, the company held 4,763 valid authorised intellectual property rights, covering key technology areas such as large-format wafers, BC cells and shingled modules.

Executive team reshuffle with CEO replacement

The executive change announcement outlined a major organisational restructuring. Non-independent directors Shen Haoping, Liao Qian and Zhang Changxu stepped down from their board roles and corresponding board committee positions for personal reasons; Zhang Changxu will continue to serve as senior vice president (SVP). Simultaneously, the company nominated Ouyang Hongping and Wang Cheng as candidates for non-independent directors of the board of directors, with their terms subject to shareholder approval.

At the operational management level, Wang Yanjun resigned as CEO and legal representative to focus on overseeing the semiconductor materials business. He will remain involved in the company’s strategic development as vice chairman following his resignation. The board of directors approved the appointment of Ouyang Hongping as the new CEO and legal representative, who will also serve as interim COO. Zhang Haipeng was appointed SVP, tasked with leading the new energy PV materials business. Public records show Ouyang holds a background in industrial automation from Nanchang University and boasts extensive manufacturing experience, while Zhang previously led the company’s PV materials business group and brings deep industry expertise.

Looking ahead to 2026 in his address, Li Dongsheng noted that the global economy will remain complex and volatile, with geopolitics and AI technology reshaping the industrial landscape.

At this critical juncture of industry consolidation and restructuring, market attention is focused on whether TCL Zhonghuan can achieve a fundamental improvement in profitability through its multi-pronged strategy: consolidating its wafer leadership, accelerating module business integration, and strengthening technological innovation and global expansion.

TCL Zhonghuan is bidding for a controlling stake in module producer DAS Solar to bolster its presence in cell and module production, where it lags behind fully integrated rivals such as Longi, Trina, Jinko and JA Solar.