Disruptions in polysilicon supply this summer, as well as demand for solar PV during the ongoing pandemic, have added a new source of supply risk to project finance and construction that can lead to price risk and make projects unviable. (See Polysilicon pricing expected to remain rocky for six months, but more supply is on the way, published yesterday on PV Tech.)

Considering the wide availability of polysilicon, long-term price increases above $10/kg would be unsustainable for a large portion of the industry, which has adjusted to lower-priced modules for making projects pencil in a highly competitive industry.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Recent price hikes are more reactionary in nature, as the sudden unavailability of production from fires and floods coincided with longer-term trends of supply going offline. GCL-Poly’s utilisation of its 70,000-ton nameplate capacity had already been declining over time to around 80% before the 21 July explosions. Other domestic producers followed suit, performing more maintenance operations, and slowing output during COVID-19 lockdowns in China when demand was at an all-time low.

OCI, a South Korean polysilicon producer, took two of its three production facilities offline in February of this year, citing oversupply (i.e. collapse of market price) as a key reason. South Korean news outlets cited OCI’s remaining capacity at 6,500 tons out of its original 52,00 tons of capacity. Also during February, Hanwha Solutions announced it would exit the polysilicon production business after Chinese anti-dumping duties on South Korean polysilicon made its operations unviable.

Meanwhile in the US industry, as China added capacity and price fell, some of its traditional competitors in the US dropped out, thereby accelerating concentration in the sector. REC closed, SunEdison closed, Wacker suffered a fire and has since targeted semiconductors and not solar, and Hemlock backed out of a new plant.

With the sudden uptick in demand stemming from strong Chinese installation expectations in the second half of 2020 and the idling or reduction of other production sources following periods of oversupply, readily available supply at low prices suddenly vanished.

This coincidence of narrowing supply chains with sudden shocks to availability is producing higher than expected price increases. Following a period of volatility, where we expect the reaction to the explosions and flooding to fan the fears of supply shortages, prices should be more stable in the future, barring more unforeseen events.

In addition, costs for polysilicon suppliers, rather than prices for buyers, are more likely to increase. Existing projects were already contracted up to a year ago, and deals currently in the pipeline were premised on the recent low module prices. Module makers will find it difficult to raise prices by much, as there is only so much farther they can go before buyers decide to wait or look elsewhere.

Some of today’s leading suppliers have comparatively higher margins and lower costs. We can expect healthy, sustainable margins to prevail, but if margins are too high, more competition will emerge in the long term.

In the domestic Chinese market, we have observed that if module prices go above $0.20/W ± $0.01/W, project developers begin suspending projects. The entire supply chain then needs to absorb some of the cost increase, or project pipelines will stall. As recently as two years ago, polysilicon was in the mid-teens, pricewise; today however a “new normal” of price expectations prevails in the industry, and prices could not approach those levels again without collapsing demand.

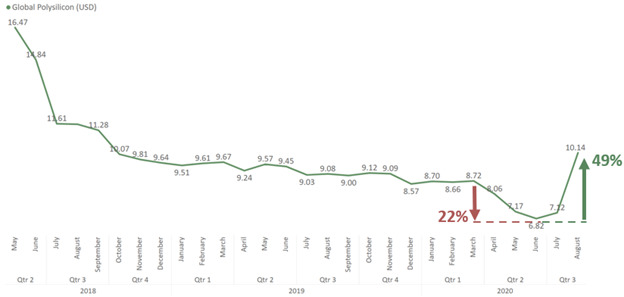

With most polysilicon pricing currently above US$10/kg and some very recent news reports citing prices above US$14/kg, domestic Chinese projects are already being pushed out several months until pricing can become competitive once again. Early hints from polysilicon suppliers indicate mid-year 2020 pricing will not be seen again until mid-Q1 of 2021 or possibly later, depending on how soon the expansions come online.

Projects in certain international markets will also need to extend timelines, or pay short-term premiums. The US is already buying higher-cost modules from Southeast Asia and is likely to experience less price changes, as suppliers have larger margins to absorb more of the cost increase. Markets in Europe and India can expect significant short-term price increases, however.

Global Polysilicon Prices Up 49 % On Average From COVID-19 Low

Source: Energy Trend | Monthly Average Polysilicon Price Tracking in USD/kg

We do not find the impact of the GCL-Poly explosions to significantly affect any single module maker. Many module producers have diversified supply sources from Dongfang, Yongxiang, Daqo, Xinte, Asia Silicon, and other localised polysilicon producers. Larger suppliers with significant ingoting and wafer cutting capacities could be more impacted, as such suppliers have large amounts of capacity needing polysilicon inputs.

Still, we do not expect any suppliers to face any significant bottlenecks in terms of available supply, only bottlenecks emerging from high prices, pushing some companies to defer purchases or pass on more costs to buyers.

Even without accidents affecting the availability of polysilicon, prices would have started recovering for modules. Both module and polysilicon prices had been at the lowest point in history following the COVID-19 outbreak and subsequent factory shutdowns.

Coupled with the recovery in the polysilicon market are increases in other module components. Glass prices are rising, fueled by increasing double-glass module production that is creating upward price pressure; strong Q3 and Q4 installations expectations from the Chinese market; and general price recovery from COVID-19 depressed demand and prices in many overseas markets, where demand is now recovering.

Newer sizing formats needed to accommodate larger modules are also presenting component suppliers with temporary challenges. New or expanded lines to handle increased widths are not that difficult or time-intensive, but may be costly at a time when many companies are carefully budgeting expansions and building cash reserves following COVID-19 lessons.

Commodity prices impacting solar, such as aluminum for module frames, are also recovering after pricing fell due to COVID-19, adding to module pricing upswing potential. Speculation is adding to higher silver paste prices — silver has more than doubled since its recent low in March, to over US$27 an ounce — and EVA/POE supplies are currently strained, as suppliers look to procure components compatible with larger module formats.

All being said, CEA foresees polysilicon, glass, and EVA/POE suppliers as needing upwards of two to three quarters to revamp production and bring new capacity online, to meet nearly 100 GW of new module and cell capacity announcements.

Other materials such as silver paste may need even longer to stabilize in price, with COVID-19 and recessionary conditions persisting in many parts of the world. After the 2007-2009 recession, speculators and investors seeking safe havens drove the price of silver over US$45 an ounce, with peak pricing not being reached until April 2011 and surpassing US$55.

Along with more projects being pushed into 2021, first due to COVID-19 and now due to pricing instabilities, global solar installations are expected to remain very close to 2019 levels, while 2021 is looking to be a brighter year for solar.

")