A new analysis from energy data and procurement platform Renewabl suggests that the renewable procurement strategy delivering the strongest protection against electricity price volatility is also the one that performs best under emerging hourly carbon accounting.

The findings point to a growing convergence between financial risk management and Scope 2 reporting, with implications for how corporate buyers and solar developers structure future power purchase agreements (PPAs).

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

PV Tech Premium spoke to JP Cerda, CEO and co-founder of Renewabl, about what the findings mean for Europe’s corporate solar market, why solar PPAs are increasingly being judged on the hours they actually cover rather than annual volumes, and how developers may need to adapt as buyers place greater emphasis on hourly matching.

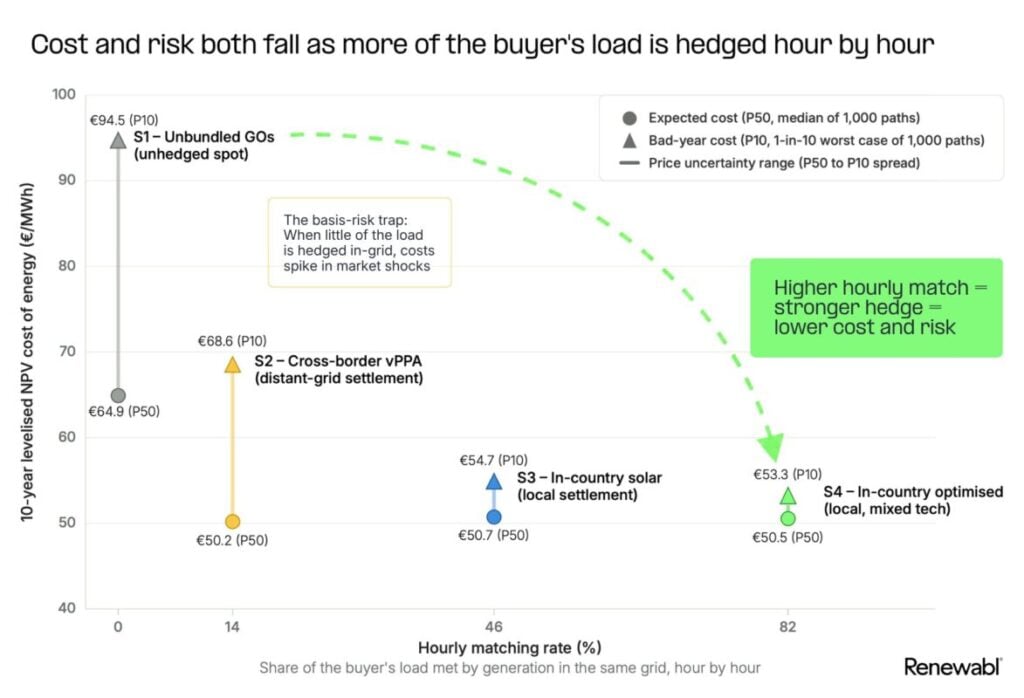

The discussion follows the publication of Renewabl’s report, European PPA strategies and the hidden cost of cross-border basis risk. The study modelled four procurement strategies across 1,000 ten-year electricity price simulations between 2027 and 2036 in France, Germany, Italy and Spain.

Using Pexapark’s June 2026 PPA price benchmarks, it compared an unhedged procurement strategy based on unbundled Guarantees of Origin (GOs), a single cross-border virtual PPA (vPPA), an in-country solar PPA and an optimised in-country portfolio combining renewable technologies.

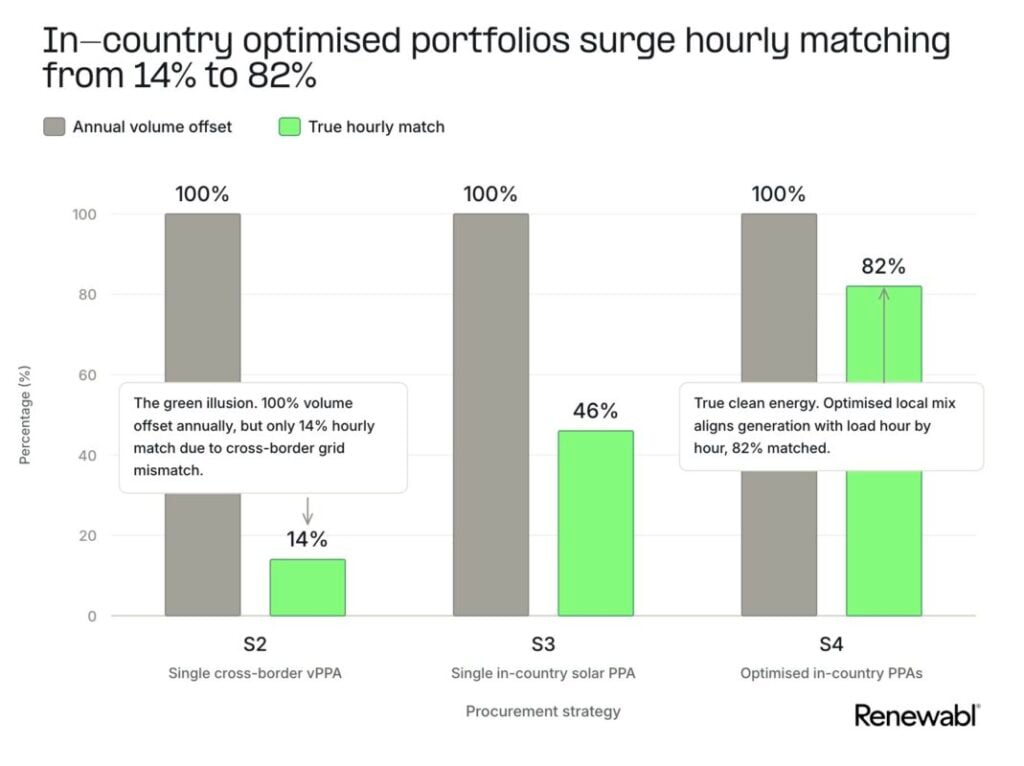

While all three hedged strategies produced similar median electricity costs of around €50/MWh (US$57/MWh), the differences became apparent under adverse market conditions. According to the report, optimised in-country portfolios removed between 85% and 91% of long-term cost uncertainty, compared with around 40% for a single cross-border vPPA. The optimised portfolio also achieved around 82% hourly matching, compared with roughly 46% for an in-country solar PPA and about 14% for a cross-border vPPA.

For Cerda, solar remains central to the European corporate PPA market, but the analysis highlights an important limitation of relying on standalone solar contracts.

“Solar sits at the centre of this analysis, because solar is where most European corporate buyers have started,” he says. “It dominates corporate vPPA volumes, it carries the lowest average strike prices, and projects come online faster in southern markets.”

However, he notes that electricity markets settle hourly, meaning a solar contract only protects buyers during the hours when generation is available.

“The finding that applies most directly to solar: a solar PPA hedges a buyer’s bill in the hours the sun is generating, and does very little outside them,” Cerda explained. “A buyer can hold 100% annual coverage and still sit well below 50% on an hourly basis if the portfolio is solar-heavy.”

Wind, he argues, complements solar by producing more consistently overnight and during winter months. Rather than weakening the case for solar, the research reinforces the value of combining technologies and measuring performance on an hourly basis.

From lowest strike price to hourly risk management

The report also raises questions about how developers structure corporate PPAs. Cerda believes the market has already begun moving beyond traditional long-term, single-technology agreements focused primarily on securing the lowest strike price.

“For most of the last decade, the model was simple: a long, single-technology solar contract, priced on volume and sold on a low headline strike,” he says. “The priority has moved to compliance and hedging.”

According to Cerda, buyers are becoming increasingly cautious about committing to fixed contract structures over long periods, particularly as cannibalisation effects and unmatched generation hours become more significant.

“Pricing conversations will start from the buyer’s load profile rather than the cheapest available megawatt hour,” he explains. “The developers who can answer ‘which of your hours does this cover?’ will have an easier sell than those leading on strike price alone.”

The findings may also challenge the role of cross-border corporate PPAs, which have historically enabled buyers to source renewable electricity from markets such as Spain while consuming power elsewhere in Europe.

Cerda stresses that cross-border agreements remain valuable, particularly for companies seeking straightforward renewable procurement, but said the report identifies clear limitations where price risk is concerned.

“What the analysis shows is where that structure stops protecting the buyer,” he says. “A cross-border vPPA settles in the generator’s market rather than the buyer’s, which leaves basis risk.”

He adds that the solution is not abandoning cross-border PPAs but adapting them to changing buyer requirements.

“For developers who’ve relied on cross-border solar, this is a signal to localise rather than a reason to panic,” Cerda highlights. “The opportunity is to meet buyers in their own market and pair solar with the local wind or storage that covers the rest of their day.”

Hourly carbon accounting strengthens diversification

Another driver behind these changes is the gradual shift towards more granular carbon accounting. While annual matching remains the basis of current Scope 2 reporting, Cerda expects forthcoming reporting frameworks to increase the importance of hourly matching over time.

“It could be significant, though I’d frame it as much about timing as volume,” he says. “Under today’s annual accounting, the strategies we modelled all look equivalent on the claim; hourly accounting would not, which changes what a buyer is paying for.”

He pointed to several policy developments, including the Science Based Targets initiative (SBTi)’s revised standard and the expected phased implementation of updated GHG Protocol Scope 2 guidance beginning in 2028, arguing that corporate buyers are increasingly preparing for that transition rather than delaying renewable procurement altogether.

The analysis also strengthens the commercial case for hybrid renewable projects incorporating wind and storage.

When asked whether the findings could accelerate hybrid deployment, Cerda says, “Yes, and I think that’s the most constructive read of the whole analysis. The point of an hourly-matching lens is that it shows you exactly where a portfolio is exposed, which is the same as showing you where storage or a second technology earns its money.”

“A well-matched portfolio of solar, wind and storage is also what delivers the clearest commercial case in the market.”

Hybrid projects and local procurement

Market conditions, however, differ across Europe. Cerda believes countries with strong domestic demand and complementary renewable resources are well-positioned to adopt in-country procurement strategies, while heavily solar-dependent markets face greater challenges.

“Spain is the clearest example,” he emphasises, pointing to increasing negative-price periods and declining solar capture rates. “That doesn’t make these markets unattractive for solar. It makes standalone, solar-only, cross-border deals struggle, and it pushes the value towards storage, hybridisation and shaped products.”

Looking ahead, Cerda expects hourly matching to become an increasingly important commercial differentiator rather than simply another compliance requirement.

“The main opportunity is that hours become priced,” he said. “Today a megawatt hour of solar at noon and a megawatt hour of firm supply overnight are treated as equal for an annual claim. Under an hourly lens, they aren’t.”

He believes this creates opportunities for developers able to offer more tailored products, allowing projects to compete on how effectively they cover customer demand rather than purely on headline strike prices.

“It becomes a differentiator, yes, but as a practical journey, not a switch that flips,” Cerda concludes. “Treat the baseline as something to improve rather than a test to pass, and the differentiation follows.”

")