The Australian Electricity Market Operator (AEMO) has found that projects seeking to connect to the National Electricity Market (NEM) in Australia rose to 43GW in June 2024, a 43% increase year-on-year (YoY).

According to the organisation’s June connections scorecard, the number of projects looking to connect to the NEM, which spans south and east Australia, has sharply risen in the past year. This is primarily due to prospective large-scale renewable energy generation projects looking to contribute to the country’s decarbonisation journey.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

During June, four projects totalling 720MW received application approval and moved into the proponent implementation stage, bringing the financial year-to-date (FYTD) total to 56 projects, totalling 12GW. One project completed registration, bringing the FYTD total to 17 projects, totalling 2.4GW.

AEMO also noted that early-stage applications involving the Network Service Provider (NSP) and AEMO increased by 74% YoY, from 6.9GW to 12GW. The typical duration was also reduced by one month, from 10.9 months to 9.7 months.

BESS projects top charts for applications

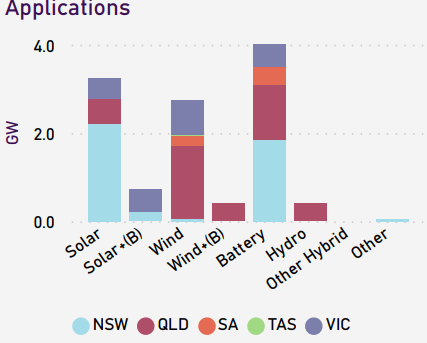

In terms of connection applications, battery energy storage systems (BESS) top the charts, with just over 6GW being made in the FYTD. Most of these have been located in New South Wales (3.2GW). South Australia is second, with around 1.2GW, closely followed by Victoria and Queensland, with around 1GW each.

Solar ranks second for connection applications in the FYTD, with around 4.5GW. Queensland ranks the highest for applications with around 2.5GW, followed by New South Wales with 1.1GW. The rest of the figure is made up of minimal contributions from South Australia, Tasmania, and Victoria.

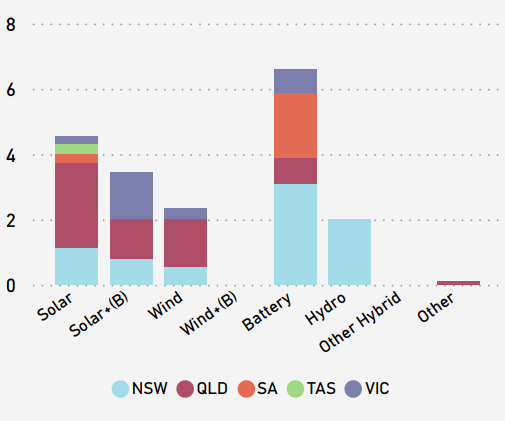

Of the technologies having seen their grid connection applications approved in the current financial year, BESS assets again claim the top spot with around 4GW. The majority of these are spread across Queensland and New South Wales, with smaller quantities having been approved in South Australia and Victoria. Tasmania has yet to see a single BESS approved.

In second place is solar, which has reached around 3.1GW. Just over 2GW of this has been located in New South Wales, with Queensland and Victoria making up the rest.

NEM needs investment to support renewable energy projects

Although one may see the figures quoted as being positive for the NEM and Australia as a whole, there must be a significant rise in investment in grid infrastructure to facilitate the transition.

A recent report by AEMO, released in late June 2024, indicated that around AUS$16 billion (US$10 billion) of investment must be mobilised to grid infrastructure. Transmission projects must be rolled out to facilitate new renewable energy, with AEMO predicting that around 10,000km will be needed.

For this, AEMO calls for the AUS$16 billion to be invested in several projects, all of which could recoup their investment costs, save consumers AUS$18.5 billion in avoided energy costs, and deliver emissions reductions valued at a further AUS$3.3 billion.

")