The global solar manufacturing landscape is poised for a significant transformation in 2026, marking a rebound in capital expenditure (capex). This resurgence follows dramatic drops in capex during 2024 and 2025, primarily caused by a systemic oversupply of solar modules in the market, particularly in China. The oversupply dampened investment activity across the industry, creating a challenging environment for manufacturers worldwide.

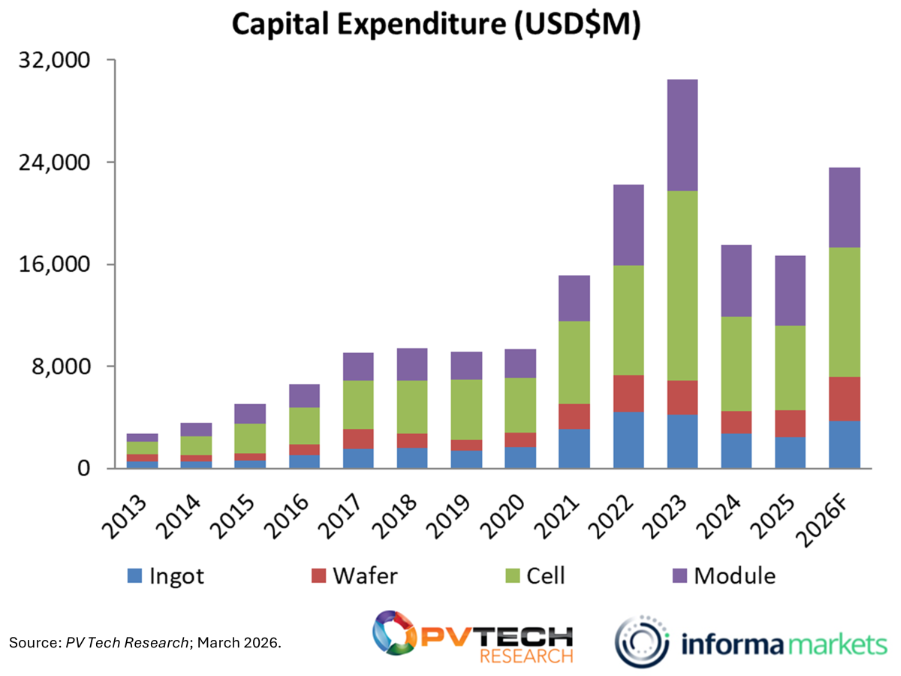

However, the tide is turning, and a global capex rebound is now expected. After reaching over US$36 billion in 2023, total capex fell to US$22.45 billion in 2024 and then again to US$21.2 billion in 2025. But this year, our data forecasts that capex spending will rise to US$29 billion. Cell capex will increase notably, rising from US$6.4 billion in 2025 to US$9.9 billion in 2026. The figures are revealed in the Q1 edition of PV Tech Research’s ‘‘PV manufacturing and technology quarterly’ report.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The capex rebound is being driven by three key factors. In the US and India, a significant ramp-up in domestic PV capabilities is offsetting reduced capex spending in China and Southeast Asia. Globally, the focus on upstream segments of the solar supply chain is intensifying, driving increased investment in cell manufacturing. Meanwhile, regions such as the Middle East are becoming key players in the global solar manufacturing landscape, with countries such as Egypt and Oman rapidly building capacity, supported by strategic partnerships and export-oriented production models.

All of these shifts are being intensified by a growing global movement to diversify supply chains outside of China and strengthen local production. This objective is being driven by domestic incentives in the US and India, and by regulatory changes, such as anti-dumping and countervailing duties (AD/CVD) and Foreign Entities of Concern (FEOC) rules in the US, and new requirements under frameworks such as Europe’s Net Zero Industry Act (NZIA).

Our 2026 forecast is based on a detailed analysis of current spending trends within existing facilities, coupled with projected expenditures for factories that have already commenced construction. By analysing these data points, we aim to provide a balanced outlook that reflects both ongoing operational investments and the anticipated contributions of new developments.

Why capex is Increasing in the US and India

The United States and India are at the forefront of the global solar capex rebound, driven by distinct yet complementary factors.

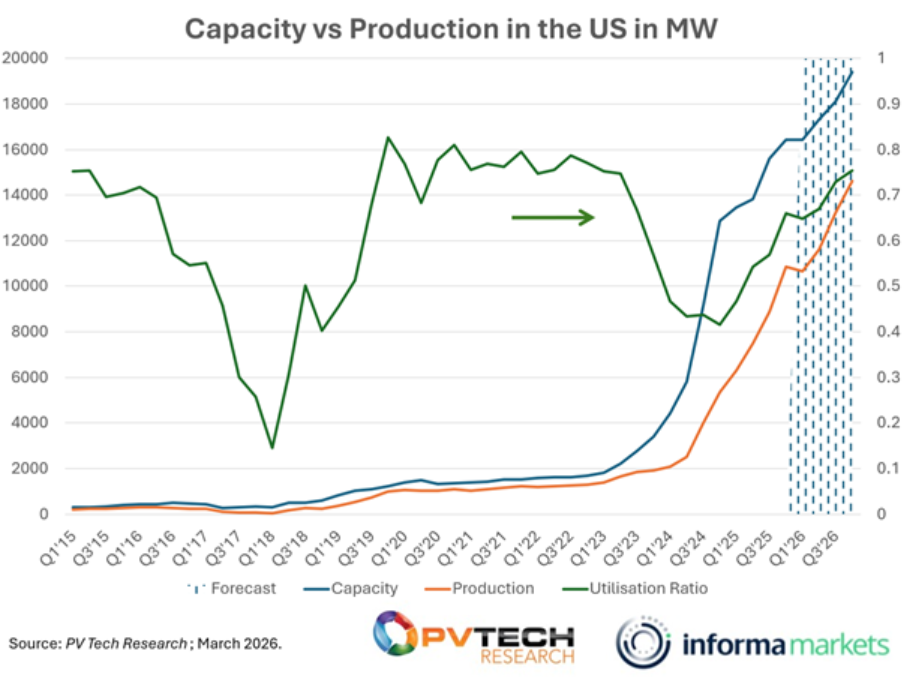

In the US, the solar manufacturing sector is experiencing robust growth, supported by a combination of financial incentives and regulatory measures. The expansion of anti-dumping and countervailing tariffs (AD/CVD) has played a pivotal role in encouraging domestic production. These tariffs, initially introduced to counter unfair trade practices, cover China and several Southeast Asian countries. India, Laos and Indonesia are also under investigation, with preliminary countervailing measures imposed on these countries in February. The antidumping investigation is ongoing. Meanwhile, new FEOC rules place further emphasis on local production and reducing reliance on foreign-controlled supply chains. Alongside federal tax credits, these measures have spurred significant interest in building domestic manufacturing capacity.

The demand for domestically manufactured PV modules is clearly reflected in utilisation rates across the US manufacturing landscape. Utilisation rates across US manufacturing facilities are approaching 80%, which is considered full capacity. This strong demand is expected to absorb any future capacity additions in the short to medium term.

However, the US still faces supply chain gaps, particularly in upstream segments. Current data reveals that cell capacity covers only 50% of module production, wafer capacity covers just 10% of cell production, and polysilicon capacity accounts for a mere 5% of module production. Addressing these gaps is critical to sustaining the growth of the US solar manufacturing sector.

Several players are capitalising on these opportunities. For instance, Hemlock (Corning) launched wafer production at the end of 2025, while ES Foundry has tripled its cell capacity. These developments highlight the ongoing shift in capex focus from modules to upstream segments such as cells, wafers and polysilicon. Underpinning this is a shift in regulation, with recent AD/CVD rulings covering cells, FEOC requirements, and the upcoming Section 232 on polysilicon.

India: competing on the global stage

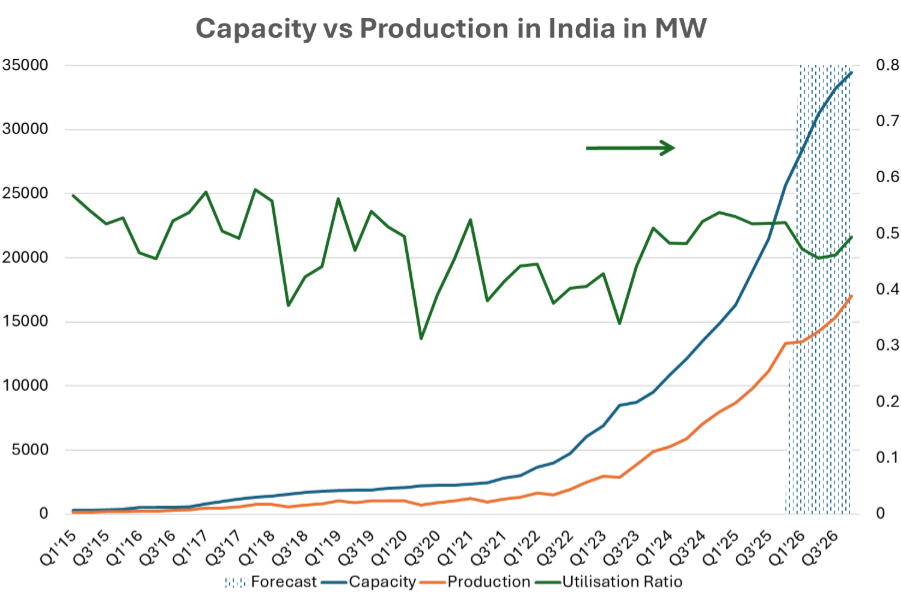

India’s solar manufacturing sector is also witnessing significant growth, driven by government support and competitive market dynamics. The Indian government has been one of the largest drivers of manufacturing growth in the country, specifically through the large government tenders. However, while government support initially set out to provide Indian-manufactured PV modules for the domestic market, we are seeing Indian producers becoming much more competitive on the global stage and pursuing new markets that were historically dominated by China.

Indian companies such as Waaree have become important players in the US market, while others are exploring opportunities in Europe. The inclusion of India in the list of countries affected by US countervailing and, possibly, anti-dumping measures (depending on the outcome of this part of the ongoing investigation) underscores its growing importance as a manufacturing base and the competitive threat it poses to established players.

Despite these positive trends, questions remain about the sustainability of India’s capacity expansion. Utilisation rates have generally ranged between 50% and 60%, indicating steady use of added capacity. However, the decline in utilisation rates before 2023 – when the industry was booming – raises concerns about the sustainability of this growth. Bridging the gap between module and cell capacity will be a key determinant of India’s capex outlook. By the end of 2025, module capacity stood at just over 82GW, while cell capacity was at just under 30GW, highlighting the need for further investment in upstream segments.

The rebound in cell capex

Historically, the largest share of solar capex has been allocated to cell manufacturing, primarily driven by technological advancements in this segment. The rebound in cell capex can be attributed to several factors.

Chief among these is the example of the US and India, where module capacity has grown to such an extent that cell production must now catch up to enable supply chains to become fully localised. Again, measures such as trade tariffs, FEOC rules and other incentives and regulations are providing the carrots and sticks to drive that localisation process, which is now increasingly including the upstream segments.

Added to this is the fact that cell production is more complex and more costly than module manufacturing, requiring greater capex investment. A key related factor is the technological evolution underway, as many large players transition from tunnel oxide passivated contact (TOPcon) to back-contact technology and move towards tandem, driving the need for new investments in cell manufacturing.

Emerging manufacturing hubs: the Middle East and beyond

Outside the US and India, other regions are benefiting from the global solar capex rebound; we are seeing investments across the board in China, Turkey, Egypt and Oman, with further expansions announced in European capacity.

The Middle East has emerged as a key player, with Egypt and Oman notably leading the charge.

Egypt has demonstrated remarkable speed in building solar manufacturing capacity. Elite Solar established a 5GW cell-and-module facility (2GW cells and 3GW modules) within just 14 months of signing contracts. This efficiency has made Egypt an attractive partner for six other PV manufacturers looking to locate capacity in the country.

Oman has completed a polysilicon facility capable of producing enough material for 40GW of solar panels. Additionally, it hosts a 400MW solar module plant for JA Solar. These developments position Oman as a significant player in the global solar manufacturing landscape. However, many of the facilities opening up in the Middle East aim to export most of their production; it remains to be seen how much of that production will be used in the domestic market.

On this front, Turkey stands out. Turkey’s solar manufacturing sector is growing organically, driven by domestic demand and proximity to European markets. While its capacity figures are smaller compared to other Middle Eastern countries, Turkey’s strategic location makes it a key player in serving European and US markets.

Conclusion

The global solar capex rebound in 2026 marks a turning point for the industry, driven by investments in the US and India, alongside emerging opportunities in other regions. The expansion of module and cell manufacturing capacity, coupled with favourable policies and incentives, is reshaping the solar manufacturing landscape. However, challenges remain, including supply chain gaps in the US and questions about the sustainability of India’s capacity expansion.

As the focus shifts upstream to cells, wafers, and polysilicon, the industry must navigate regulatory changes and technological transitions to sustain growth. Emerging manufacturing hubs like Egypt, Oman and Turkey are playing an increasingly important role, highlighting the global nature of this rebound.

Looking beyond 2026, our forecasts through 2030 build on current spending patterns and this year’s projections as a baseline. These longer-term outlooks incorporate broader economic trends, such as inflation, shifts in global supply chains and industry growth trajectories, to outline potential growth scenarios and provide a forward-looking perspective on the evolving market.

By 2030, we anticipate investments outside of China will continue moving upstream, with markets increasingly focusing on wafers and polysilicon as cell manufacturing capacity expands. Governments are expected to play a pivotal role in shaping these priorities with a strategic focus on building domestic supply chains to enhance energy security. Meanwhile, investments in China are expected to grow alongside technological advancements and the next phase of PV cell technology, further solidifying its role as a leader in cutting-edge solar manufacturing.

The capex rebound highlights how the industry is addressing supply chain gaps, embracing technological advancements, and diversifying production bases and positioning itself to meet the growing demand for clean energy and resilient supply.

The Q1 edition of the ‘PV manufacturing and technology quarterly’ report, the definitive benchmarking resource for the PV technology value chain, is out now and available here.