United States trade policy is no longer just impacting imports to the US; it is reshaping where the world builds solar manufacturing capacity. With 92% of global PV module capacity now facing restrictions on entering the US market, manufacturers are racing to establish compliant supply chains across the world. Simultaneously, domestic producers are accelerating efforts to build US-based cell manufacturing capacity. What started with anti-dumping measures against PV modules from China has extended across Southeast Asia and beyond through ongoing anti-dumping and countervailing duty (AD/CVD) investigations.

The scope continues to expand upstream, now covering PV cells and potentially Chinese polysilicon through the ongoing Section 232 investigation. Companies targeting the US market are scouting new locations for manufacturing capacity spanning the entire value chain, strategically avoiding countries and regions subject to trade restrictions. Foreign Entity of Concern (FEOC) rules add an additional layer of complexity to an already labyrinthine procurement landscape.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The data underpinning this article is drawn from the latest edition of PV Tech Research’s ‘PV manufacturing and technology quarterly’ report, the definitive benchmarking resource for the PV technology value chain.

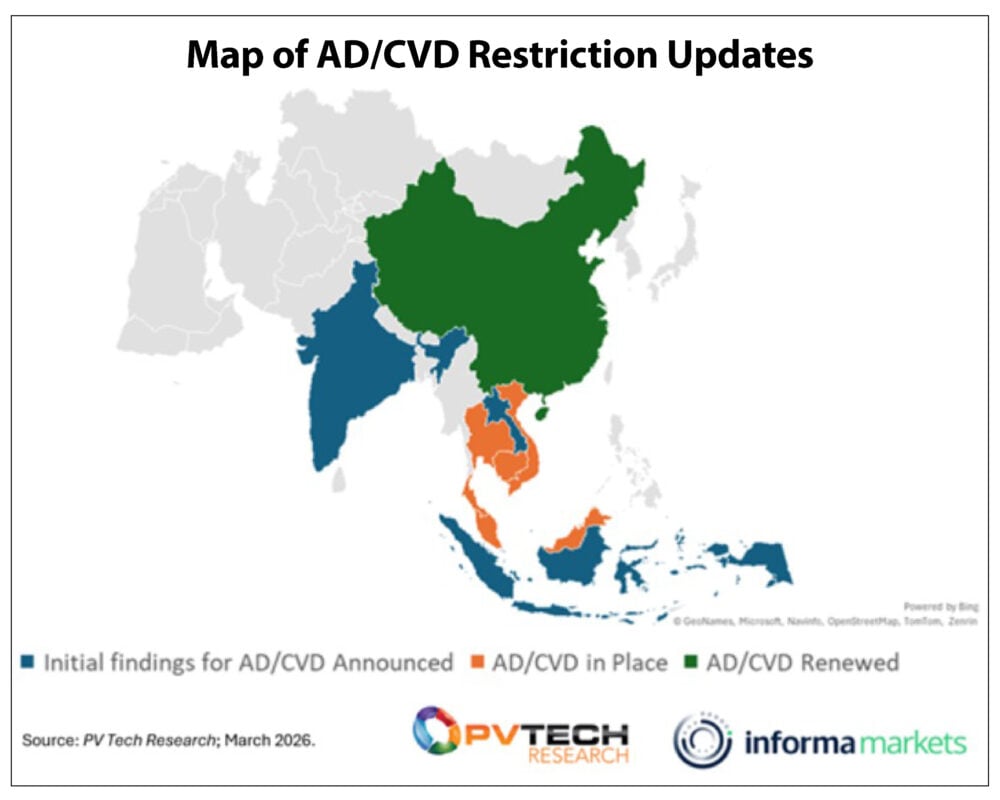

Nearly the entire global PV industry now faces US restrictions

As of March 2026, more than 92% of the world’s PV module manufacturing capacity faces some form of restriction on entering the United States, primarily through anti-dumping and countervailing duties (AD/CVD), according to data from PV Tech Market Research. This figure reflects the preliminary results of AD/CVD investigations targeting India, Indonesia and Laos, as well as the extension of existing duties on China. The scope continues to widen: the Department of Commerce has received a petition from the Alliance for American Solar Manufacturing demanding another AD/CVD investigation, this time targeting cells produced in Ethiopia.

The highly anticipated results of the Section 232 investigation into polysilicon supply are expected in the first half of 2026, though the timeline remains uncertain. This investigation represents a fundamental departure from previous trade enforcement tools. Unlike traditional AD/CVD measures that target finished products like cells or modules, Section 232 focuses on polysilicon, the raw material at the foundation of the solar supply chain. Depending on the scope of restrictions imposed, all modules and cells manufactured from non-US polysilicon could face substantial tariffs, effectively reshaping the entire global solar value chain at its source.

This upstream approach could eliminate the need for ongoing AD/CVD rulings by directly targeting and disrupting Chinese manufacturers’ value chains at the source. While the results are likely to create both winners and losers, depending on how polysilicon from various sources is managed, in the meantime, the prolonged uncertainty has already destabilised the market, with manufacturers struggling to determine which supply sources will remain viable for US market access.

FEOC rules are reshaping ownership structures

In addition to AD/CVD duties, the United States has implemented FEOC rules that create another significant barrier for foreign manufacturers seeking to access the US market. FEOC regulations prohibit clean energy projects from using equipment manufactured, owned, or controlled by entities tied to China, Russia, Iran, or North Korea if they wish to qualify for federal tax credits, including Section 45X for manufacturers and Sections 45Y and 48E for developers.

Most interpretations of the FEOC rules currently assume that 25% represents the threshold for significant ownership in manufacturing operations; however, this remains an assumption pending official clarification. Earlier this year, the US government released Material Assistance Cost Ratio (MACR) calculations for developers requiring at least 50% of solar component costs to be sourced from non-FEOC countries. In a typical market, this requirement might be manageable. However, China maintains a dominant position across the entire solar supply chain, especially further up with polysilicon and wafer production. This dominance explains why the United States has adopted these measures to enable domestic supply chain development.

These restrictions targeting China have produced significant unintended consequences. The locations of new manufacturing capacity have become more geographically diverse than ever before, with some of the world’s largest solar manufacturers expanding into the Middle East and North Africa. Substantial capacity has been announced or is already under construction in Saudi Arabia, Oman and Egypt.

In these new locations, Chinese companies are increasingly establishing joint ventures to navigate both regulatory and financial challenges. The 24.9% ownership threshold has emerged as a critical figure in manufacturing partnerships, appearing repeatedly in recent months as companies structure investments to remain below the presumed 25% FEOC threshold. Canadian Solar resumed direct oversight of US market manufacturing through a joint venture in which the Chinese-listed entity holds exactly 24.9% ownership. Similarly, JA Solar owns 24.9% equity in an Omani manufacturing facility, while LONGi has reduced its stake in Illuminate USA, a US manufacturing joint venture with Invenergy, to comply with FEOC considerations.

The new solar manufacturing map

A new grouping of companies is emerging, most of which are set up exclusively to supply the US market from countries not subject to AD/CVD tariffs or FEOC restrictions. These are smaller, more agile, usually privately held and able to quickly set up manufacturing capacity without committing to long-term expansion plans in just one country. Examples of these companies can be seen in sub-Saharan Africa, where PV Tech Research estimates that there is currently 11GW of PV cell manufacturing capacity operational, with additional capacity coming online this year. However, these manufacturers face significant regulatory risk. The evolving legislative landscape can quickly make compliant locations non-compliant, as demonstrated by the current situation in Ethiopia.

There is also significant PV cell and module manufacturing capacity up and running in Türkiye; until recently, this was almost all to supply the domestic market. However, US trade policies have opened up opportunities for exporting products. Türkiye’s PV cell manufacturing capacity is forecast to increase from 1GW in 2023 to about 7GW by the beginning of 2027, and its module capacity from 13GW to 30GW in the same timeframe. This has been driven by the HIT-30 high-tech investment incentive programme, launched in 2024, to strengthen the country’s position in the global solar energy market.

Five companies were selected to receive support on the basis that they reach an annual cell manufacturing capacity of 5GW. Most of this capacity will be targeted at exports, with the US the key market for these. CW Enerji, one of the selected companies, has already secured cell supply contracts with US buyers worth nearly US$30 million and holds a memorandum of understanding to supply US$750 million worth of modules to a US client through 2030.

Turkish manufacturers are currently very attractive to both module manufacturers and purchasers, as they offer lower FEOC risk, though these rules may change down the line. Some manufacturers are even vertically integrated beyond current regulations, with wafer and ingot production capacity in the country.

The US cell bottleneck is becoming critical

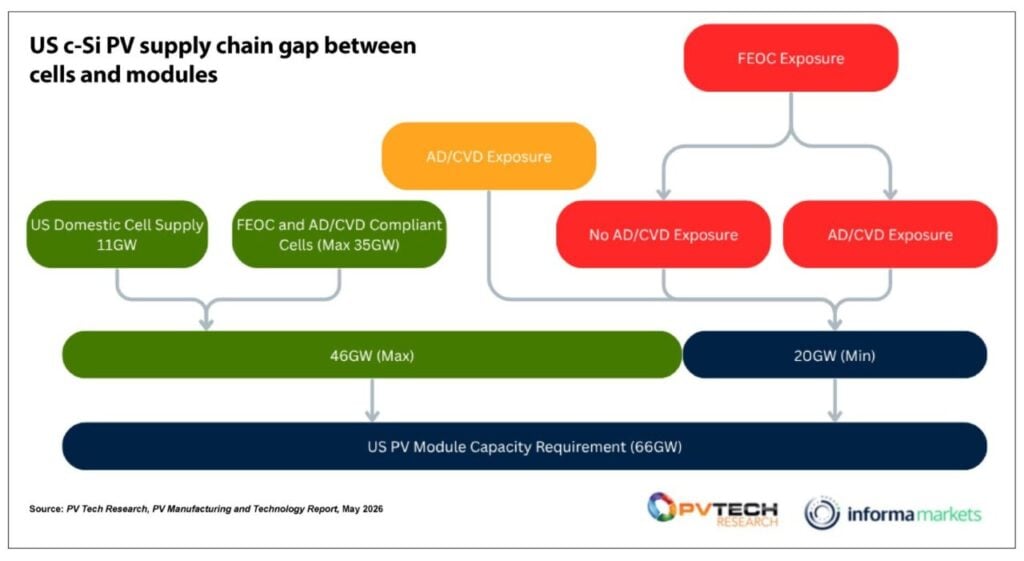

Excluding thin-film technology, the United States currently has over 66GW of domestic module manufacturing capacity, supplied by just over 11GW of domestic cell capacity, according to PV Tech Research’s data. With over 92% of the world’s cell capacity under some form of restriction from entering the US, filling the gap between cell availability and module capacity is becoming increasingly challenging. However, the US benefits from being the most profitable market globally, meaning that cell manufacturers that remain eligible to ship to the US will continue to do so.

We estimate that the remaining cell capacity outside the US across all FEOC-compliant countries free of AD/CVD restrictions totals just under 35GW. Even if this entire capacity were dedicated to supplying the US market, it would still not be sufficient to meet module manufacturing demand, leaving a gap of at least 20GW in the impossible yet best-case scenario of all compliant cells worldwide being shipped to the US.

This supply constraint forces US module manufacturers and project developers to navigate a tiered procurement strategy. The top tier consists of cells that are both AD/CVD-compliant and FEOC-compliant, offering maximum supply chain security and full eligibility for federal tax credits.

The middle tier includes cells subject to AD/CVD tariffs but FEOC-compliant, which still qualify for tax credits. In this case, the manufacturer will have to pay the relevant AD/CVD tariff depending on the country of origin. However, down the line, it can still claim the 45X manufacturing credit, and the developer can claim the 45Y production credit. The viability of these will depend on pricing from the original manufacturer, the relevant tariff rate and the product’s availability. India is a prime candidate for this type of cell, but given the demand for locally produced cells from its domestic market under India’s ALMM-II mandates, which come into effect in June, availability is likely to be a key constraint in this category.

Cells in the bottom tier have FEOC exposure, whether AD/CVD-compliant or not; they face tariffs and, more importantly, are ineligible for tax credits.

This tier has two subcategories. The first is cells with FEOC exposure but no AD/CVD tariff; these cells are in the smallest supply and would come from a FEOC-exposed company building a facility outside its home country.

The second subcategory is cells exposed to both FEOC and AD/CVD, so the manufacturer would have to pay a large tariff on imports and would not be able to claim any manufacturing credit, and the developer would not be able to claim any production credit. These will also be the cheapest possible cells; viability will mainly depend on the willingness to do business, the tariff rate and the pricing available for modules ineligible to claim tax credits.

An alternative scenario to the choices outlined above, albeit an unlikely one, would be that some of that 66GW of operational module capacity would remain idle until the domestic cell supply chain catches up with demand. While the very high utilisation rate we have been seeing in the US in recent months makes this unlikely, it could become a possibility as import policies continue to tighten.

These supply constraints can be viewed as temporary growing pains in the US solar manufacturing landscape. Significant domestic cell capacity is currently under development and expansion. This year, ES Foundry tripled its production capacity. Later this year, T1 is expected to bring its cell manufacturing online, and Suniva has announced additional cell capacity for next year. This can be seen as a timing mismatch between the module production capacity already operating and the cell capacity still ramping up. However, until domestic cell production reaches scale, the market faces serious volatility as manufacturers and developers navigate the complexities of trade restrictions, compliance requirements and supply availability, as outlined above.

Winners, losers and the next phase of the trade war

The clear winners in this environment are primarily US manufacturers with domestic value chains, particularly those with vertically integrated operations and secure access to compliant cell supply. Companies able to establish FEOC-compliant structures through joint ventures or regional partnerships are also emerging in stronger positions, especially across Türkiye, MENA and parts of sub-Saharan Africa.

Meanwhile, manufacturers that relied heavily on Southeast Asian cell supply chains now face growing pressure as Indonesia and Laos become increasingly restricted routes into the US market. The challenge is particularly acute for companies with significant US module assembly capacity but insufficient domestic or compliant upstream cell manufacturing capability.

The global manufacturing response has become increasingly fragmented. Larger manufacturers are pursuing long-term investments in Türkiye and MENA, often through carefully structured joint venture arrangements designed to comply with FEOC thresholds, while smaller, more agile players continue shifting production between jurisdictions as regulations evolve.

At the same time, the industry faces mounting uncertainty around the pending Section 232 investigation into polysilicon, which could further reshape compliant supply chains by targeting upstream materials rather than finished products. The result is a market increasingly driven not just by manufacturing cost and scale alone, but by political alignment, ownership structure and trade compliance.

It is important not to forget that all this is not happening in a vacuum; energy demand is growing in the US as the country looks to reindustrialise and, more importantly, to compete in the AI race. In this environment, a successful solar manufacturing industry is no longer defined solely by cost competitiveness or scale, but by control of the supply chain.

The current cell bottleneck already demonstrates the risks of depending on a limited compliant supply, with domestic module capacity far outpacing the availability of unrestricted cells. For the US solar industry to scale sustainably and competitively, manufacturing expansion must move further up the supply chain. Building module assembly capacity alone is no longer sufficient; securing domestic production of cells, wafers, ingots and polysilicon is becoming essential to ensuring long-term supply security, regulatory compliance and the resilience of the US solar manufacturing ecosystem.

The companies at the centre of America’s burgeoning c-Si supply chain will offer in-depth insights into their work at our annual PV CellTech USA conference in San Francisco on 13-14 October. From polysilicon through to cells, the event will explore the opportunities and challenges in the rapidly evolving US PV manufacturing landscape through the experiences of the supply-chain innovators leading the way. For full details and booking, click here. PV Tech readers can save 20% with code PVT20.