Global renewables capacity will reach 7.3TW by 2028 under existing policies and market conditions, but this growth trajectory will still be falling short of the target of tripling global renewable energy capacity to 11TW set at the COP28 summit in Dubai by the end of the decade.

This is according to the International Energy Agency’s (IEA) Renewables 2023 report. In the report, the IEA said the current growth trajectory would enable global renewables capacity to increase to 2.5 times its current level by 2030 under the current policies and market conditions, surpassing 9TW.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

However, in the accelerated case forecast, which assumes enhanced implementation of existing policies and targets, the global renewables capacity could reach over 8,130 GW by 2028. Such progress could put the world on track to meet the global tripling goal.

Additions around the world

Last year, global annual renewables capacity additions increased by almost 50% to 507GW, the fastest growth rate in the past two decades and the 22nd year in a row that renewables capacity additions set a new record.

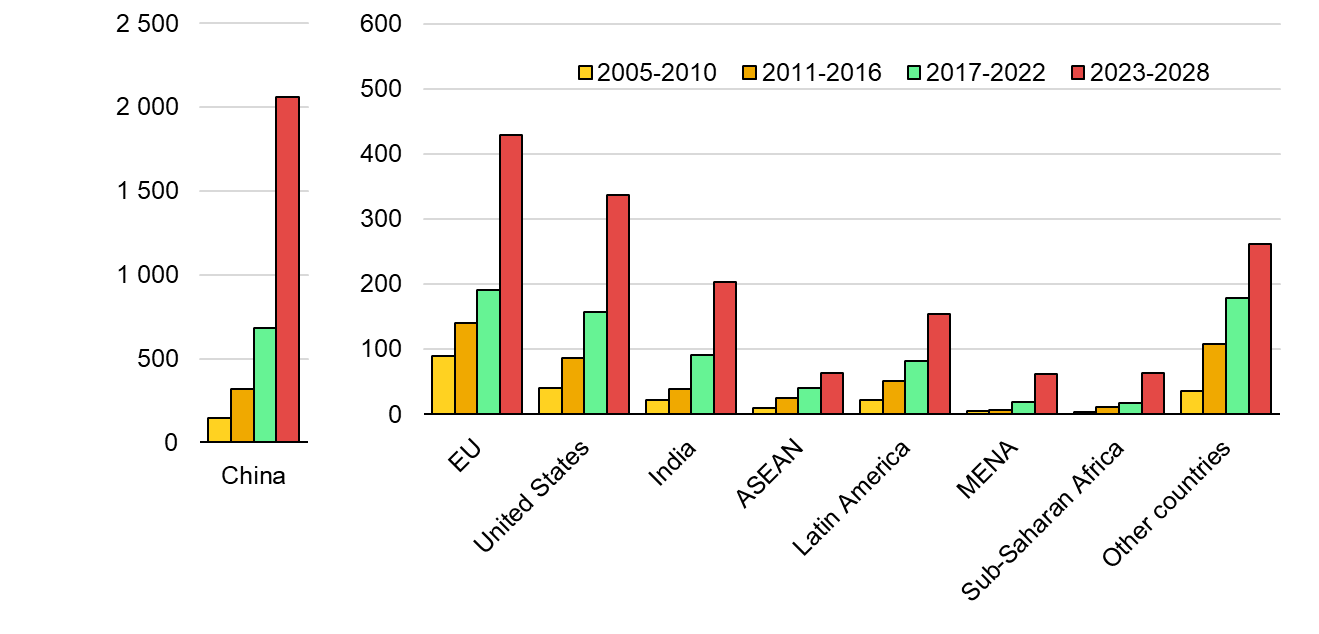

China again led the growth as its solar PV and wind additions increased by 116% and 66% year-on-year, respectively. Its renewables capacity will grow to more than 2TW by the end of 2028, more than three times higher than the capacity as of the end of 2022.

Between 2023 and 2028, China’s renewables capacity will be about five times more than the European Union and six times more than the US, as shown in the graph below. Currently, the EU and the US are the second- and third-largest growth markets.

The IEA said China’s Net Zero by 2060 target, supported by incentives under the 14th Five-Year Plan from 2021 to 2025, relies on ample availability of locally manufactured equipment and low-cost financing to stimulate its renewable power expansion over the forecast period.

In the US, expansion growth is expected to be the result of the Inflation Reduction Act (IRA). Meanwhile, in the EU, country-level policy incentives will support EU decarbonisation and meeting energy security targets.

India’s renewables capacity will reach 200GW by the end of 2028 thanks to progressive policy improvements to remedy auction participation, financing and distributed solar PV challenges. These improvements will spur faster renewable power growth through 2028.

Challenges of reaching 11TW by 2030

The IEA highlighted four challenges that could prevent countries from around the world from reaching the 11TW target by 2030, including policy uncertainties and delayed policy responses to the new macroeconomic environment; insufficient investment in grid infrastructure; cumbersome administrative barriers, permitting procedures and social acceptance issues; and insufficient financing in emerging and developing economies.

There are several areas that governments can do to increase renewables capacity. For policy uncertainties and delayed policy responses to the new macroeconomic environment, the IEA suggested that governments can adapt auction designs to the new macroeconomic environment by indexing contract prices to various macroeconomic indicators specific to each renewable technology, such as relevant commodity prices, inflation and interest rates for different stages of project development.

Governments can also align and integrate the planning and execution of transmission and distribution grid projects with broad, long-term energy planning processes, ensuring that regulatory risk assessments allow for anticipatory investments.

When it comes to insufficient financing in emerging and developing economies, the IEA said higher interest rates could prevent renewables developers from accelerating the expansion of renewables capacity. Additionally, the lack of affordable financing remained the most important challenge to renewable project development in most emerging markets and developing economies.

Currently, G20 countries account for almost 90% of global renewables capacity. According to the IEA, the G20 could triple their collective installed capacity by 2030 in the accelerated case. While some developing countries do not have renewables targets or supportive policies now, the IEA said these countries still need to increase the rate of new installations in order to contribute to the tripling of renewables capacity.

Commenting on the possibility of tripling global renewables capacity to 11TW, energy think tank Ember’s programme director Dave Jones said that when considering the level of deploying renewables in 2023, the goal is “entirely achievable”.

“The twin COP28 goals of a tripling of global renewables and a doubling of energy efficiency could help push energy CO2 emissions down by 35% by 2030. This means we are increasingly on track not only for a peaking of fossil fuel use this decade, but for sizable falls in fossil fuel use,” he said.