PV-Tech’s flagship PV ModuleTech conference returns, through an online platform, on 9-11 March 2021, with a focus on providing utility-scale site developers and investors a comprehensive understanding of the new module formats being sold to the market today.

The event comes a few months after the PV CellTech 2020 Online event that outlined the PV technology roadmap for 2021-2025, including cell efficiencies and wafer size format changes.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

This article previews the topics for PV ModuleTech Online on 9-11 March 2021, including the range of session topics, and why the sessions over the three days will be invaluable to downstream stakeholders during 2021 and beyond.

From module power density to raw power from larger format sizes

The rate of change of module availability during the past couple of years has been fast and furious, moving the industry quickly from 72-cell p-multi modules (circa. 315-320 Watts) to mono-based 400-600W variants being supplied today.

The key push for this change has come from the upstream manufacturing segment, with downstream users being forced quickly to change site design and yield projections. For most investors and developers however, there is a great deal of confusion here, mainly caused by the industry no longer having a mainstream silicon-based offering for utility-scale projects globally.

To understand the changes – and indeed what may happen over the next 12 months – it is necessary to split out module supply into a few key issues and then see what the impact on each of these is today; and how this may change going forward.

In essence, this forms the basis of the session topics to be covered at PV ModuleTech Online during 9-11 March 2021, with speakers being invited to contribute where best suited.

Before looking at more detail across the session topics of the event, it is worth re-emphasizing one point that is often overlooked in the push for higher module power ratings: power density is a function of cell efficiency and module power ratings result from the number of cells used in the module format.

The more cells that are used (or cut up into halves or strips) and then assembled into a module, the higher the power. However, the power density comes from the cell efficiency, and changes here are gradual in nature year-on-year. Ultimately, there is a balance between the size of the module and other issues such as transportation, handling and reliability. This is where all the activity falls today, in assessing the various options from suppliers to the industry.

Of course, there is also the question of bifaciality, glass thickness and bill-of-materials. These issues exist for any module supplier/panel-format, but some of these issues (especially at the BoM level) are all the more pertinent when radically new module sizes are being offered.

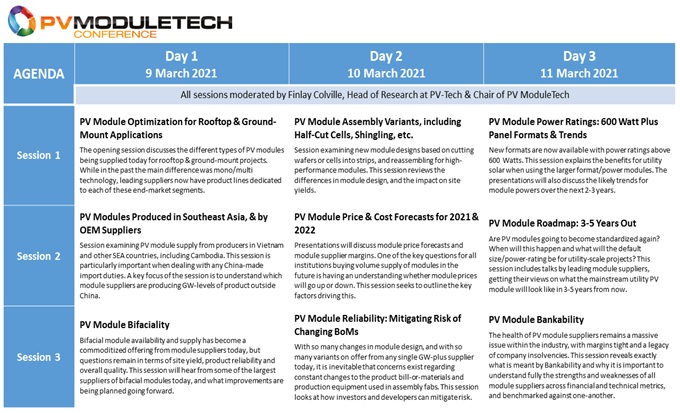

A closer look at the PV ModuleTech Online agenda

The online event has 9 sessions across 3 days (9-11 March 2021). Each session is 2 hours in duration, with 3 invited talks per session. In total, 27 invited talks are given over the duration of the event. Each of the talks are prepared through extensive advance discussions with the speaker and the PV ModuleTech team. In this way – similar to PV CellTech Online last October – the content and value of the talks combine to form a unique platform during times when face-to-face travel is unavailable.

The 3 sessions each day are scheduled to overlap with APAC, Europe and US time zones, with the focus of each session geared to the audience needs in each region. This is explained in more detail now.

First, here is the overall agenda for PV ModuleTech Online.

Day 1 – 9 March 2021

The opening session of the event will address the basic module design and availability for rooftop and ground-mount applications. This has become a key differentiator in module supply today, and also often in the range of companies focusing on each of these segments.

The PV industry still has some long-time players that focus mostly on rooftop markets (such as LG Electronics and REC Group for example), trying to get the higher ASPs here and also avoiding a losing battle for large ground-mount sites with the global market leaders. This was a tactic that was attempted in the final days of Japanese module production, before the end of Japanese manufacturing for PV recently.

Go back five years, the only main difference between rooftop and ground-mount solar was mono and multi (all 60-cell panel sizes). Today, the 60-cell (or similar sizes) are almost exclusive to rooftops, with larger panels often deployed on large commercial rooftops.

As such, there are now different module suppliers and panel specifications being targeted at rooftop and ground-mount sectors. Globally, the PV industry has yet to fully understand this issue. Moreover, some of the suppliers for rooftops are only active in a handful of regions or countries.

Session 2 on Day 1 focuses on OEM module supply, a key issue that has impacted most on imports to the US market in recent years. OEM production – and indeed the whole manufacturing footprint across Southeast Asia – has been in a constant state of flux for the past five years. This continues in 2021, with different factory ownership/output across cell and module fabs in Vietnam, Cambodia and Indonesia, for example.

The theme highlights the need for module buyers to understand who makes what and where. One would imagine this should be relatively simple to track, but this appears far from the case. There remain many PV module suppliers ‘claiming’ to have manufacturing capacity in Southeast Asia, but this often simply means they have OEM deals with other companies to label product. It is a trend that sits all too often in the background, when it comes to PV module production, and has been used extensively also by Japanese and Korean PV suppliers in recent years.

The final session on Day 1 – overlapping with US east-coast/west-coast time zones – will offer the current status of bifacial modules for utility solar. The industry has moved on a couple of years since bifacial supply can to the fore, and there is now good field data on just how much yield can be expected from utility-based sites.

Day 2 – 10 March 2021

The second day of the event starts with a session on module types that involve changing the basic 6-to-8 inch cell size aspect ratio, the most common of which has been to cut cells in half, post cell manufacturing, ahead of module assembly.

However, several other variants now exist, in particular changes arising from the use of larger wafers now.

This session will seek to explain to module buyers/users why this matters when comparing module types, and what risks are introduced through these (often bespoke) technologies.

Session 2 of Day 2 addresses what everyone buying modules in 2021 wants to know: where will module pricing go during 2021 and (longer-term) through 2022. This is understandably one of the most common questions I get day-to-day. The topic seems to come up most at the start and end of each year.

Normally, at the start of the year, a narrative gets propagated by module sales teams that module pricing will go up during the second half of the year, and perhaps it would be a nice idea if people placed orders now rather than wait until later in the year.

This happens every year. The reasons normally are pulled from a list: pending under-capacity, short-supply of raw materials, threat of trade issues pending or current, etc.

The reality is the module pricing fluctuates, but normally ends the year lower than when it started out. How much pricing declines is always more than suppliers ‘guide’.

While many module buyers often think module pricing methodology is often confused and without much basis, there are a few key issues that ultimately guide that the leading module suppliers sell at.

This session will provide some guidance in this regard, hopefully giving listeners some key tools when looking at this issue over the next 12-18 months.

The final session on Day 2 focused on PV module reliability. With the timing of the final session again being early-evening Europe and US daytime, the narrative will be firmly on module reliability issues pertinent to European/US-based due-diligence criteria. This is important to clarify, as module reliability due-diligence is different across key PV end-markets in Asia, including India also.

Module reliability testing is something that really has to be done by a dedicated test centre, and be specific to the module product type under consideration by an investor/development-stakeholder. Therefore, the issues being factored in by investors/lenders for module procurement do generally become country-specific, and local test-centre focused.

This session will address module reliability from different perspectives, hopefully providing a good overview of how to best mitigate against risk in supplier or product selection under contract.

Day 3 – 11 March 2021

The first session on Day 3 of the event addresses one of the major developments in 2021: the availability of ultra-high power rated modules, including panels now specified above 600 Watts.

What are the benefits and risks using these panel formats? What advantages and challenges are involved in utility-scale site design, build and optimization?

Similar to most of the sessions during PV ModuleTech Online, talks will come from different parts of the value-chain, including module supply and downstream site building. Clearly, for different stakeholders looking at designing plants in 2022 and beyond, knowing how the higher power trends will continue is imperative, and this topic will hopefully be addressed also during the session.

The second session of the final day will expand upon this theme, looking at how module power and design will evolve over the next few years. This will allow factoring in some of the conclusions from the recent PV CellTech 2020 Online event, where cell efficiency and substrates (n-type or p-type) were examined across leading module supplier roadmaps. Additionally, the offering from thin-film suppliers should be addressed here, as these naturally have different roadmap deliverables.

The final session is perhaps the key one for the event this year: PV module supplier bankability. It is now about 18 months since PV-Tech introduced its detailed PV ModuleTech Bankability Ratings reports to the industry, and the findings here are now driving module supplier due-diligence selection processes for many of the major high-volume module users globally.

Bankability is something that is now more clearly understood, including the role of financial health coupled with manufacturing strengths. This session will include the latest rankings of leading global module suppliers, specific to volume supply and utility-scale deployment, and the factors that are guiding short-listing for large-scale solar during 2021 and beyond.

Getting involved in the event this year

During the coming weeks, companies and speakers for the different sessions will be revealed on PV-Tech. This will show that all the issues for module supply need to be addressed from the perspectives of the module producers, module buyers/investors, and independent parties looking at bankability, reliability and product quality.

There are still a few speaking slots open still for the event. Anyone interested in being part of the new online PV ModuleTech conference this year can contact me through the tabs at the event website here. Similarly, registering to attend the event can also be accessed via this link.