European Union (EU) member states awarded a record 25.2GW of new solar PV capacity through auctions in 2025, according to SolarPower Europe.

This was alongside deals completed for just under 6GW of new capacity through corporate power purchase agreements (PPAs) last year.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

These are the latest figures to come from trade body SolarPower Europe’s latest report, ‘Auctions and Corporate PPAs: European Market Review 2025’. These figures reflect a record-breaking year for European renewables, in which solar and wind accounted for more of the continent’s electricity generation than fossil fuels for the first time in history, and highlight the differences in attractiveness of two key financing mechanisms: national auctions and corporate PPAs.

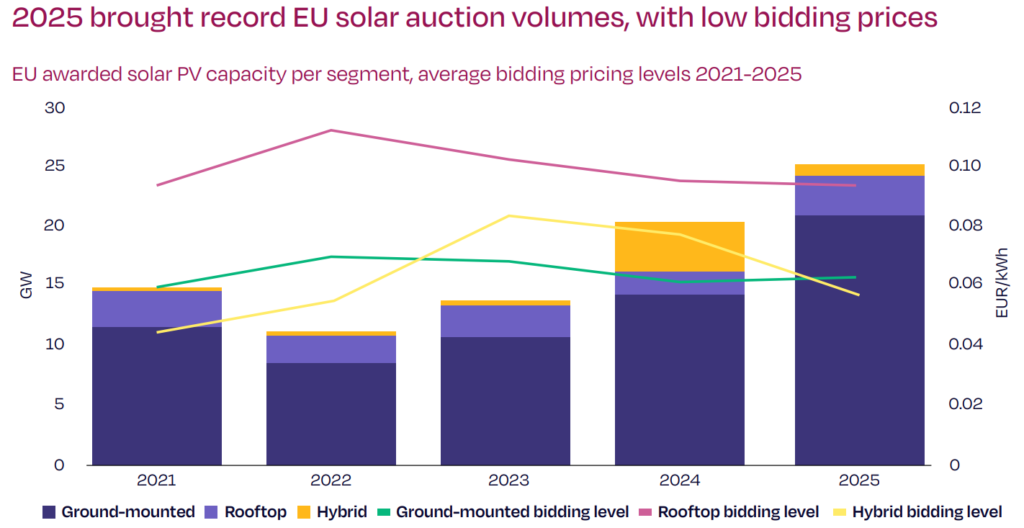

In the former space, the EU’s 25.2GW of new auction-backed solar capacity is a record, up from 23% the previous year. Europe has seen its solar PV capacity awarded through auctions increase each year since 2022, the year of Russia’s invasion of Ukraine and the resulting energy crisis; as SolarPower Europe puts it, these kind of auctions have been essential in “helping protect citizens and businesses during and after the energy crisis.”

The graph above shows how total capacity awarded through auctions has changed over time, compared to bidding prices for that capacity, split by technology type. The general trend has been towards more capacity awarded through auctions, and falling bid prices, which SolarPower Europe attributes to an easing of “inflationary tensions” and a decline in equipment costs. In 2025, ceiling tariffs were, on average, 22% higher than bidding prices, compared to 2022, when awarded bid prices were, on average, 12% higher than the ceiling tariffs on offer.

The report also argues that better economic conditions have driven the shift towards a greater reliance on utility-scale solar. Between 2024 and 2025, the contribution of utility-scale capaciry to the total solar PV capacity awarded through auctions increased by more than ten percentage points to break the 80% threshold, and SolarPower Europe argues that “consistent competitive bidding” helped keep bid prices low, and provide “clear economic incentives” for investors to participate in auctions for utility-scale solar capacity.

The benefits of clear government support are also evident in the report, which points out that Italy awarded an “exceptional” volume of solar PV capacity in 2025 through its Fonti di Energia Rinnovabile (FER) X auction scheme. SolarPower Europe puts the total capacity awarded through the scheme at 10.8GW, which compares to the 7.7GW of capacity awarded that was reported in December, and means that Italy accounted for more than half of the capacity awarded across the continent in 2025.

The report also notes that Germany, which has long lead the industry in government auctions for renewable power, has almost hit the milestone of awarding 25GW of solar PV capacity through auctions since 2022. SolarPower Europe says that these awards have been “one of the most impactful deployment instruments” behind the growth in Germany’s solar sector, and these two countries illustrate how government auctions can help drive up investments in new solar capacity in both the short and long term.

Growth in utility-scale batteries

The report also notes that battery energy storage systems (BESS), particularly in the utility-scale sector, have been helped considerably by national government support. In total, close to 60% of the EU’s operational batteries are in the residential sector; however, in 2025, utility-scale batteries accounted for 55% of new installations, an all-time high, and a shift that SolarPower Europe expects to “accelerate” in the years to come.

The report notes that of the 70GWh of utility-scale BESS procured in 2205, around 50GWh was contracted through capex-based support schemes financed through EU instruments, such as the Modernisation funds.

Indeed, on a national level, specific battery auction schemes were introduced in several countries, such as Poland, Spain and Portugal, some of which were expanded “after attracting overwhelming interest”, suggesting that there is considerable appetite for new battery projects in Europe, provided there is a form of financing to help blunt the initial capex requirements of the technology.

Europe sees slowdown in corporate PPAs

The report also describes how private finance is affecting investment trends in the European renewable energy industry, and notes that, unlike public auctions, private investment has been less influential in the solar-plus-storage sector. This is not to say that there is not considerable investment being made in batteries in Europe—the report notes that over 6.5GW of storage capacity was signed through flexibility purchase agreements in 2025—but that private investment has flowed into solar-plus-wind, rather than solar-plus-storage.

According to SolarPower Europe, private offtake agreements involving solar-plus-wind accounted for 13% of all deals including solar PV. This compares to ground-mounted PV, which accounted for 81% of all solar deals; rooftop PV, which accounted for 3%; agrivoltaics (agriPV), which accounted for 1%; and solar-plus-storage, which also accounted for 1%. Yet this is not to say that there is no interest in batteries from private investors, but that market mechanisms may not yet be appropriate for the scale of investment to properly reflect this interest.

“Combining Solar PV and BESS, whether it is with hybrid PV systems or virtually, under a single agreement, is still subject to a number of market and regulatory barriers,” explained SolarPower Europe. “Removing those will be key to unlock the next wave of private offtake agreements.”

More broadly, the report notes that the solar capacity contracted through corporate PPAs decreased from 2024 to 2025, falling to below 6GW. This is lower than both the 2024 and 2023 figures, and SolarPower Europe describes this decline as a “moderate slowdown”, rather than one that speaks to a “structural decline” in corporate appetite for signing PPAs. Yearly trends in corporate PPA deals are shown in the graph below.

Perhaps most strikingly, some of Europe’s most mature renewables offtake markets have been struck by price cannibalisation, curtailment and downward pressure on energy prices that have made renewable energy PPAs more risky in the eyes of some investors. While more than 2GW of capacity was contracted through corporate PPAs in Spain in 2025, this is a 7% decline on the capacity contracted the previous year, while Germany saw a 56% decline in solar PV capacity contracted through PPAs between 2024 and 2025.

These shifting market dynamics, and their impacts on risk perception and investment, was a topic of conversation at this year’s Solar Finance & Investment Europe event, held in February in London by PV Tech publisher Solar Media. There, Daniel Machuca, global head of project finance at Sonnedix, said that an “evolving” financing environment means that risk considerations are shifting quickly, which is perhaps dissuading large-scale private investment in European solar, particularly following record-breaking capacity investments in 2024.

Italy, meanwhile, saw a doubling of new solar PV capacity contracted through PPAs between 2024 and 2025, reflecting growing private investment in its solar sector alongside investment made through government auctions. Italy and Poland, which reported a 33% year-on-year increase in corporate contracted capacity in 2025, are the only countries profiled by SolarPower Europe to see increases in solar capacity contracted in this way between 2023 and 2024 and then again between 2024 and 2025.

Europe’s leading renewable energy financiers will meet in London for the fifth edition of the Renewables Procurement & Revenue Summit, held on 20-21 May by PV Tech publisher Solar Media. Information about the event, including the full agenda and options to purchase tickets are available on the official website.

")