Jason Kaminsky, CEO, kWh Analytics, on how renewable asset owners and their insurers are adapting the way they assess risk from natural catastrophes and extreme weather events.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

In recent years, there has been a significant shift in the role of insurance and the way policies are written for renewable energy projects. The rapidly declining cost of the technology, federal policy changes, and energy price inflation have brought about a surge in the development and use of renewable energy sources, and along with it, the need for specialised insurance coverage to protect these projects. Inherently a risk transfer vehicle, insurance has become an essential part of the project finance puzzle. Simply put, if an asset is uninsurable, it is unfinanceable.

Although opportunities abound in the renewable industry, rapid, massive growth does not come without challenges for insurers. Clean energy is a fairly nascent asset class with the first projects of material size built in the early 2000s. Early on, renewable energy found its way into the hands of underwriters who analysed adjacent asset classes (like power or oil and gas), whose view on the risk, at the time, did not demonstrate a significant loss profile. In the years following, as carriers gained more experience, insurance coverage for wind, battery, and solar was regularly underwritten, and became more prevalent in the market, with generous terms for the insureds.

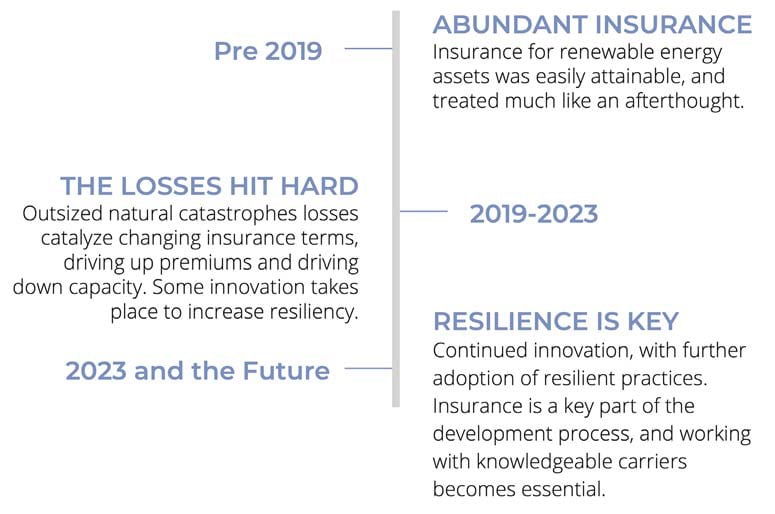

That was, until 2019.

A few factors contributed to a change in how projects were underwritten and priced. First, as an industry, we began building solar projects in regions that had greater exposure to natural hazards, such as hail storm risk in Texas. Second, cost pressures on power purchase agreement (PPA) rates resulted in tightened operations and maintenance budgets, and some of the basics in risk management (such as vegetation management) were overlooked. These two factors, combined with significant fire, flood, and hail events between 2019 and 2023 resulted in outsized losses for many renewable energy assets.

At the same time, global carriers were facing an array of losses across all business segments from the increasing impact of natural disasters, which led to a generally conservative approach to pricing property risks across the entire insurance industry. Asset owners began to experience tightened capacity and stricter terms and conditions, with some unable to secure insurance for their assets at all. We entered into what’s called a ‘hardening market’, meaning vital insurance was more expensive and more difficult to obtain.

Today, renewable asset owners and their insurers are undergoing an evolution in the way they approach risk. Using the influx of available data for solar, wind, and battery assets has become key to better understanding and protecting against exposures from natural catastrophes and extreme weather events.

Natural Catastrophe Models in Evaluating Extreme Weather Risk

To assess the risk of a renewable energy facility, underwriters typically evaluate the exposures in two categories: natural catastrophes (broken into six primary perils: hurricane, earthquake, wildfire, severe convective storm (including hail and tornado), winter storm, and flood) and attritional risks (risks that are not associated with catastrophic events, such as theft, equipment breakdown, etc). For solar assets, many of the losses are driven by natural catastrophes, while the attritional risk profile is generally stable. In contrast, equipment failures have been more significant loss drivers for both offshore and onshore wind sites.

Extreme weather risk is typically evaluated and understood using natural catastrophe (‘nat cat’) models. A typical nat cat model utilises a stochastic event set for each peril, simulating tens of thousands of hypothetical events, which yield a frequency and severity profile of events at a given location, such as the number and magnitudes of earthquakes or the number and maximum wind speeds of hurricanes.

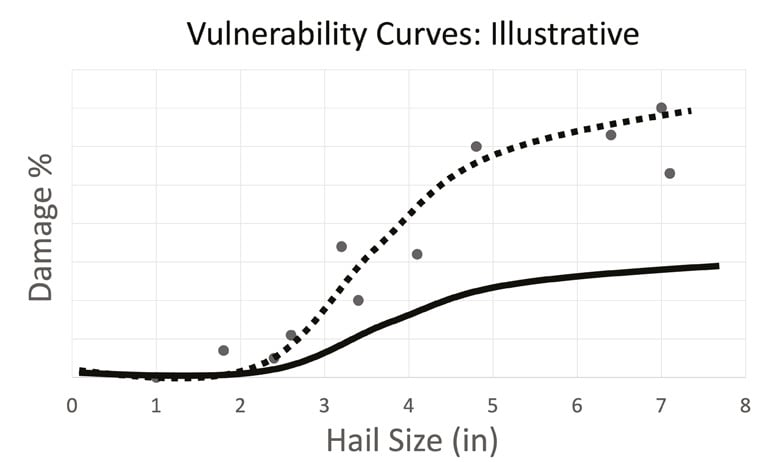

Each event in the stochastic event set is then transformed into a loss prediction using a vulnerability function. In essence, this function converts a wind speed of X into a distribution of predicted losses (in dollars) of Y. The models typically allow a user to select many characteristics of the underlying building type to generate a loss forecast: a brick building will behave differently than a steel building in an earthquake, and both will behave differently than a solar power plant. However, given the rapid growth in the solar market and more limited data available to model developers, they often use a proxy building type to mimic what they estimate may happen to a solar power plant.

As an output from the model, an insurance underwriter then receives a result that is not dissimilar from the P-values often associated with a solar generation forecast. An ‘exceedance probability’ curve conveys the results in terms of return periods: for example, a 1-in-100 year loss is a P99 risk. These are generated on a peril-by-peril basis for any given location, and are often distilled into commonly used metrics: average annual loss (AAL) – the average value of annual losses over the modeled period – and probable maximum loss (PML) – a loss expectation that is expected to be exceeded once over a defined period, such as 250 or 500 years.

While this sounds very elegant, some context is warranted about why these models are not a panacea. First, the models were developed for insurance companies to model portfolios of assets. Insurance companies purchase insurance themselves (in the form of reinsurance) and if a carrier has exposure to 10,000 homes along the Eastern seaboard, they want to know their exceedance probabilities for a bad hurricane. The models have been extended to price individual locations, but there is an element of false precision at this level of granularity. Second, there are multiple models available commercially, and some proprietary models developed by large carriers. Third, the models are most accurate for the key perils where most insurance is purchased globally, such as hurricanes, earthquakes, and flood. The underlying models to support the events most important to the solar industry, such as hail, are simply not as robust or as accurate. Fourth, the models generally lack any data on how solar assets perform, and proxy asset classes inaccurately represent solar. To put it another way, the vulnerability curves are wrong.

When you put it all together, the act of pricing an insurance policy becomes challenging. Solutions have emerged to help address these deficiencies in the market. Insurance underwriters, like kWh Analytics, have used real industry loss data to model renewable energy assets more accurately in any given location. Third party consultants, like ABS and VDE, have developed their own models to incorporate industry expertise into the results and generate a loss forecast.

Testing labs like RETC and PVEL have demonstrated that not all modules handle hail the same way and that the tilt angle of the module on a tracker can weigh heavily into the odds of a significant claim versus minor damage. Leading asset owners are developing strategies to be informed when hail is impending in order to send signals to their operators to put the trackers into hail stow.

The good news is that innovation is happening quickly, and the industry is collectively figuring out how to best apply the models and data that exist. These models and data come into play in an important debate happening right now in the industry over how much insurance should be required for an asset owner to secure project financing. Tax equity investors and lenders are not underwriting natural catastrophe risk, but they are at risk of losing their invested capital if a significant, uninsured loss happens on the site. Up until 2019, it was not atypical for an owner to be able to easily and cheaply procure full limits for their assets.

Managing Risk Through Effective Modelling

After the insurance carriers began demonstrating significant losses, it became much more expensive to procure full limits for all of the underlying perils, and in some cases impossible. Underwriters began pushing more of this risk onto the asset owner, asking them to hold higher deductibles and ‘sublimitting’ the limits for key natural catastrophe perils. This presents a challenge for the bank and asset owner alike: while we can model these risks for an exceedance probability curve, what the industry has come to appreciate is that actual losses and claims have at times exceeded even some of the worst forecasts out of these models.

As the industry continues to face various challenges, the importance of managing risk through effective modelling techniques becomes increasingly critical. With the help of data, models are now able to leverage large data sets of loss data and meteorological data to improve their stochastic event sets, leading to more accurate physical loss and performance estimations.

A critical aspect of managing risk in various industries, including insurance, finance, and even healthcare, is actuarial modelling. This statistical method utilises historical data to estimate the likelihood of future events, such as accidents or natural disasters. Actuaries use this information to set insurance rates, estimate reserves, and manage risk.

Data allows for more accurate and efficient modelling techniques. Traditionally, property insurance was based on COPE information (Construction, Occupancy, Protection, and Exposure). With the rising emphasis on the value of data, modelling firms are now able to leverage large sets of loss data to more accurately fit vulnerability curves, as well as more expansive historical weather data to improve their stochastic event sets. While nat cat modelling agencies have broadened their capabilities across industries and new construction types, model developments have lagged for renewables and especially PV, as they are relatively new asset classes with minimal historical loss data publicly available.

Generally, carriers use the recommended proxy structures, valuing a portion of the site as a building, a portion as electrical equipment, a portion as substations, etc., but not accounting for the various electrical or glass components included in this asset class, or for protective measures sites may have in place. While insurance companies have begun to address this with modifiers and credits/debits to adjust for some resiliency factors that are becoming more well-understood, e.g. stow, there are many factors which remain unaccounted for in typical insurance underwriting.

Different entities have approached enhancing solar modelling differently. For example, VDE Americas, an engineering advisory company for renewables, has developed its own hail risk assessment tool based on a blend of radar- and spotter-identified hail events to yield a theoretically more accurate event set. However, the lack of available data, intentional data collection, and rapid PV technology transformation in the industry has led to slow improvement in risk modelling for these assets, further contributing to the current hardened property insurance market. As more industry stakeholders recognise the value of data, potential efficiencies in modelling, risk transfer, and asset resiliency will continue to become unlocked. Once insurers begin to utilise the power of data to incorporate site maintenance, resiliency measures, and thorough underwriting into their risk assessments, the burden of the hardening market may ease for asset owners.

Risk model vulnerability curves are adjusted on a peril by peril basis to best align with the loss database. A consistent, but not surprising, issue is that industry standard vulnerability curves are drastically underestimating PV losses due to hail. Buildings are not a sufficient modelling proxy as most of the damage is isolated on the roof. The potential risk for a roof is also measured differently than it is for a glass panel, as the hail crack size and the value of the roof is a minor fraction of the asset compared to the value of modules at PV sites. Solar farms are also more spatially expansive and value should not be modelled as single points.

Vulnerability

The REAL model also makes further adjustments to take site resiliencies into account, shifting the vulnerability curve up or down to represent the increase or decrease in risk respectively. In the case of hail, research has been completed to suggest that stowing modules ahead of a severe convective storm can significantly reduce the impact energy of hailstones. While loss data can give indications of the impact of resiliency factors on risk of loss, evaluation of some technological improvements may rely on physics based models or lab based testing to collect data until robust field data is able to be collected and evaluated.

Addressing the Discrepancies in Renewable Energy Production Estimations

Asset energy production is another area where modelling and data can be critical, and independent engineers play an important role in the renewable energy industry by evaluating the performance of a site for financing purposes. These engineers use various models to estimate the energy production potential of a site, taking into account factors such as location, climate, topography, and equipment. By providing accurate production estimations, independent engineers help to ensure that renewable energy projects are financially viable and that energy providers can meet the demands of their customers.

Case Study

KWh Analytics has begun to address some of the modelling deficiencies caused by the lack of industry wide data by utilising their own extensive renewables database. The REAL (Renewable Energy Adjusted Loss) model accounts for equipment, performance, and management data from over 300,000 operating assets and over US$50B in loss history at solar sites to give a more accurate and fair representation of potential risks for these assets.

Site Maintenance: Properties with operations and maintenance logs and well-laid plans for vegetation management, torque audits, and general inspections of the site have a different and often more positive risk profile than other sites lacking comprehensive O&M plans.

In-depth underwriting: Nat cat models for traditional real estate utilise secondary building characteristics which consider each characteristics’ influence on modelled building exposures. Similar model modifiers and technical considerations must be made for solar to get an accurate view of risk. Example points from the REAL Assessment include:

- Hail: Stow programs considering monitoring capabilities, time to trigger hail stow, stow angle, glass thickness, and tempering will have an altered risk profile.

- Flood: In the case of flooding, solar modelling best practices have been adopted to model a solar site, as opposed to an individual building, with the implementation of site gridding (placing many points overlaying a site footprint). However, with the rapid development of solar and relatively infrequent flood map updates, models often do not consider the updated topography of a site and any site prep or build considerations. Many large utility scale sites are not laid out in a neat square. Instead they follow the natural topography and may have site cut-outs to allow for flood drainage, elevating where possible to bring sites above the 100 year or 500 year flood plains.

Resiliency Measures: Assets designed for regional perils will fare better in these extreme weather events. Sites in the central US which employ panels with thicker, tempered glass and utilise a robust hail stow program may have a significantly lower AAL (Average Annual Loss) than those without. While sites in California don’t need to consider hail, maintaining a low fire fuel load via vegetation management becomes more important. Likewise, while building in or near a flood zone, height of panels and equipment pads become a main driver of losses. The risk of a PV site raising panels and electrical equipment up to the 500 year flood elevation should be evaluated differently than PV built at a lower height.

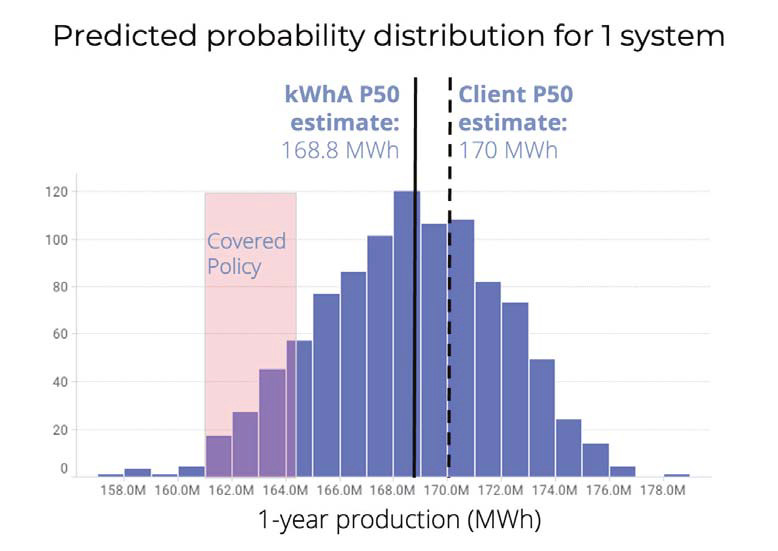

However, recent research from the 2022 Solar Risk Assessment has shown that production estimations provided by independent engineers have been nearly 8% over actual production. This discrepancy is due to a number of factors, including the fact that the models used by independent engineers do not always accurately account for the variability of renewable energy resources. In addition, unexpected changes in weather patterns and equipment performance can also contribute to discrepancies between estimated and actual energy production.

To address this issue, kWh Analytics is using more sophisticated modelling techniques that take into account a wider range of variables and provide more accurate predictions of energy production. Utilising data, companies like kWh Analytics have constructed a data-driven probability distribution that combines all of the disparate risk factors of a solar PV project into a single insured production figure, and are able to price this risk and move production volatility into the insurance markets. This lowers the risk on the cash flow streams for lenders and investors, making it a more appealing investment opportunity and improving financing terms.

From a sponsor’s perspective, protecting downside risk on renewable energy investments is pivotal. When an energy project underperforms, this has direct impacts on expected revenue, leading to potential losses. Therefore, it is important to have a holistic understanding of production risk and the included factors.

One of the primary drivers of plant underperformance is unscheduled equipment maintenance and failures. This can result in significant downtime and lost energy production, leading to lower overall project returns. In a recent analysis completed on behalf of the US Department of Energy, data modelling found that 80% of energy losses come from just 10% of maintenance tickets. When looking at the breakdown of culprit equipment, inverters cause 46% of energy losses, higher than all other components.

Trackers, transformers, and downtime related to replacing and servicing modules are also common causes of underperformance. These issues can be mitigated through proper maintenance and monitoring, but unexpected failures can still occur. Advances in data modelling find that layering probabilistic modelling on top of standard deterministic modelling allows actuaries to evaluate uncertainties not well defined with deterministic modelling alone.

Deterministic modelling: Using system design specifications to estimate the output of the system under ideal conditions.

Probabilistic modelling: Using data, such as historical weather data and insights from published studies, to estimate the uncertainty on the deterministic modeling, such as the occurrence of rare but impactful events.

In studies using actual client data, the kWh Analytics P50 forecast, while lower than a client’s estimations, has proven to conform more closely with actual production curves.

Carriers as Catalysts

With the rise of solar energy, the insurance industry has had to adapt to the unique risks and challenges that come with insuring solar sites. Modelling agencies have broadened their view to include more accurate construction and occupancy classes specific to solar sites and the advent of big data and machine learning algorithms has greatly aided in this process.

Machine learning algorithms can identify trends and anomalies in data that would be difficult or impossible for humans to detect, enabling actuaries to analyse vast amounts of data to identify patterns and make more informed decisions leading to more accurate predictions and better risk management.

As a result, models have been adapted to include solar-specific secondary modifiers to appropriately tune results based on site characteristics. With these advancements, insurers can more effectively underwrite solar sites and provide better coverage to their clients.

The growth of the sector and rapid technology improvements have led to a vastly different insurance landscape than just a few years ago. In the past, insuring renewable energy assets was uncharted territory, with few insurers having the expertise to underwrite this asset class. As databases expand and models improve to better simulate and understand risk, the industry continues to mature.

Carriers have a unique role to play, not only in the growth of renewable energy, but in the resilience of the assets. With their comprehensive understanding of property, performance, and natural catastrophe risk, carriers – and the underwriters they employ or support – can encourage resilient design, construction, and management of sites. Improved technology, such as stow capable trackers, storm detection systems, and smart cleaning systems, have made way for new and better ways to protect assets, and carriers can be at the forefront of this revolution by incentivising insureds to take advantage of these advancements. By sharing their expertise and data with their clients, insurers can help insureds to take measures that reduce the risks of natural catastrophes and other hazards, ultimately contributing to the sustainable growth of the renewable energy sector.

The renewable insurance industry has changed drastically and rapidly. Though the market has faced a recent hardening, updates to technology, data collection, and resiliency provide hope for a future where extreme weather risk is better mitigated, and overall asset risk is shared appropriately. By sharing information and incentivising asset resiliency, renewable energy asset owners and insurers can work together to create a more sustainable future for all.

Author

Jason Kaminsky is the CEO and co-founder of kWh Analytics, a provider of Climate Insurance for renewable energy assets. He is passionate about activating insurance capital into climate-forward opportunities and has helped grow the company from its creation. Prior to joining kWh Analytics, Jason spent over three years as a Vice President of Environmental Finance at Wells Fargo Bank, where he originated and financed tax-equity investments. KWh Analytics specialises in unique risk transfer products using real-world project performance data and decades of expertise, such as the Solar Revenue Put production insurance and kWh Property Insurance. The company has insured over US$4 billion of assets to date.