Australia leads the world in residential rooftop solar, with 22GW of household capacity installed, but its commercial and industrial sector has deployed only 5.6GW, despite consuming more electricity than households, according to a new report from the Institute for Energy Economics and Financial Analysis (IEEFA).

The report, ‘Unlocking the Clean Energy Potential of Australian Business Rooftops’, describes the commercial and industrial (C&I) segment as the “missing middle” of Australia’s energy transition, which is regarded as too large to access the residential incentives that have driven household solar adoption and too small to qualify for the frameworks designed to support utility-scale generation.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Australia is a world leader in household rooftop solar, but businesses have installed only 5.6GW, despite consuming more electricity than households, the IEEFA said.

IEEFA estimates the technical rooftop solar potential across Australia’s C&I building stock could reach between 17GW and 31GW by 2050 under different growth scenarios, and as high as 86GW when rural and agricultural buildings are included.

The gap between current deployment and that potential, the report argues, reflects structural problems rather than a lack of commercial appeal. IEEFA’s analysis found that solar and battery storage projects on business premises typically deliver strong financial returns, with payback periods of five to seven years in many cases.

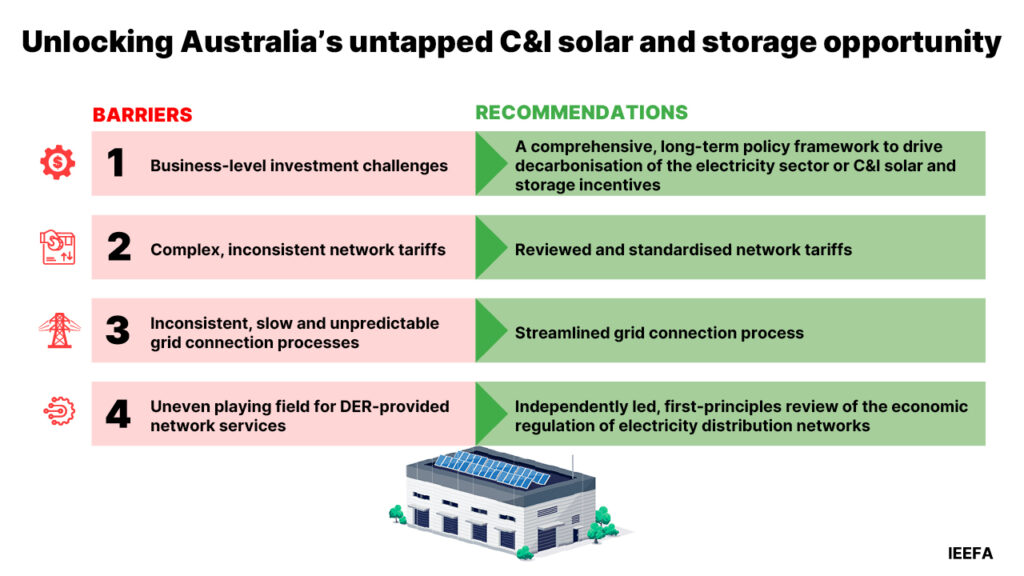

Annual C&I installations have flatlined in recent years after an initial growth spurt in the mid-2010s, constrained by four key barriers identified through stakeholder interviews and analysis: business-level investment challenges, complex and inconsistent network tariff structures, a fragmented and slow grid connection process, and an uneven policy and regulatory landscape across jurisdictions.

Four barriers, one missing middle

The business-level investment problem is compounded by the prevalence of rented commercial premises.

Because most businesses rent their premises, landlords are typically the final decision-makers on solar and battery investments. Since landlords do not pay the energy bill, they see little to no financial benefit from these systems and have limited incentive to advance projects.

This split-incentive problem has been well documented in energy efficiency research and applies equally to solar and storage.

On network tariffs, Australia’s 16 distribution network service providers have each developed distinct tariff structures, creating a fragmented, inconsistent landscape for C&I distributed energy resource project proponents operating across network boundaries.

Demand charges, which can constitute up to 40% of a business’s electricity bill, are inconsistently applied across providers, making it difficult to model investment returns or develop nationally scalable business models.

The grid connection process presents a further obstacle. IEEFA found that connection timelines for C&I solar and storage projects are frequently unpredictable, with processes that vary across jurisdictions and network operators adding cost and uncertainty to projects that are already competing for capital against core business expenditure.

The report’s fourth barrier is an uneven policy landscape, in which state and federal support mechanisms for the C&I segment are patchy, overlapping in some areas and absent in others.

The financial stakes of inaction are well documented elsewhere. The Climate Council has estimated that solar and battery storage offer Australian businesses and households protection against fuel price shocks that run to AU$1 billion (US$700 million) per month, a figure that has become more relevant as wholesale electricity price volatility has reasserted itself through 2025 and 2026.

As PV Tech’s NEM Data Spotlight for May 2026 documented, utility-scale solar prices hit AU$225.88/MWh during a mid-month generation shortfall, with the pricing spike driven precisely by the kind of supply gap that embedded commercial generation could partially offset.

Policy recommendations and market context

IEEFA recommends a combination of targeted financial incentives to address business-level investment barriers, standardisation of network tariff structures across distribution zones, streamlined grid connection processes for C&I-scale projects, and a more consistent policy framework at both state and federal levels.

The report argues that these measures would unlock a resource that is currently stranded on rooftops that are already built, owned and in many cases well-positioned for solar installation.

The scale of the opportunity sits within a broader Australian solar market that continues to grow at the utility scale.

Rooftop solar’s annual generation contribution to the NEM has also grown steadily, though the IEEFA analysis makes clear that the residential segment is doing most of the heavy lifting.

Australia’s technical rooftop potential across C&I areas alone could approach 40GW, but some estimates suggest the figure could fall well short if barriers are not addressed, with CSIRO projecting slow growth to just 17GW by mid-century under a constrained scenario.

The materials embedded in that potential capacity also have broader supply chain implications. Speaking exclusively to PV Tech Premium, UNSW researchers have warned that accelerating solar deployment at all scales increases pressure on silver supply chains, with current consumption rates raising questions about material availability within years if recovery and recycling rates remain low.

A C&I rooftop buildout of the scale IEEFA describes would intensify those supply dynamics considerably, adding further weight to the case for parallel investment in module recycling infrastructure.