United States trade policy has not only reshaped where solar products can be imported from; it has also fundamentally altered how manufacturers and developers must think about cell procurement. With more than 92% of global PV module manufacturing capacity now facing some form of restriction on entry into the US market, the question confronting buyers is no longer simply where cells are made, but who owns the manufacturer, how the entity is structured and, increasingly, what technology it uses. In this environment, a tiered framework developed by PV Tech Research for understanding the US solar cell supply has become an essential navigation tool.

A four-tier procurement landscape

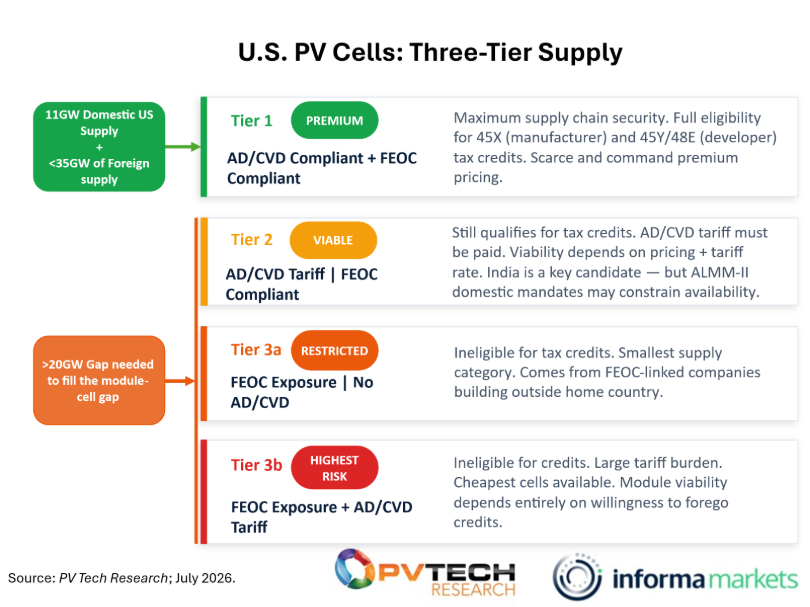

At the top of the hierarchy is Tier 1 – Premium: cells that comply with both anti-dumping/countervailing duties (AD/CVD) and Foreign Entity of Concern (FEOC) requirements, offering maximum supply chain security and full eligibility for federal tax credits under Sections 45X for manufacturers and 45Y and 48E for module buyers. This is the gold standard in the current environment, but supply in this tier is scarce and commands a significant price premium. Domestically produced US cells and a small number of manufacturers in Türkiye and parts of the Middle East and North Africa (MENA) region qualify, but combined volumes remain well below market demand. As Thus, the supply-demand imbalance is fuelling a race to expand production, especially in the US.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The next level down is Tier 2 – Viable. This category includes cells that remain FEOC-compliant but are subject to AD/CVD tariffs. The important feature is that tax credit eligibility is preserved: the manufacturer can still claim the 45X manufacturing credit and the developer the 45Y production credit, with the relevant tariff representing an additional cost burden on top. Viability at this tier depends on the pricing offered by the original manufacturer, the applicable tariff rate and product availability. India is the prime candidate in this category, but its domestic content mandates set out in the Approved List of Models and Manufacturers List-II, set to come into force in mid-2026, are expected to constrain the extent of Indian cell capacity available for export to the US market as domestic use is prioritised, limiting the availability of cells in this tier.

At the bottom of the hierarchy sits two subcategories of cells carrying FEOC exposure, both of which are ineligible for federal tax credits – the critical commercial penalty in a market where those credits can determine project viability. The first, Tier 3a – Restricted, comprises cells with FEOC exposure but no AD/CVD tariff, and is also the smallest supply category: these typically come from FEOC-linked companies that have established manufacturing outside their home country in a tariff-exempt jurisdiction but have not reduced their ownership stake below the presumed 25% FEOC threshold. Tier 3b – Highest Risk – carries both FEOC exposure and AD/CVD tariffs. These represent the cheapest cells available globally, but viability depends almost entirely on a developer’s willingness to forego credits and absorb the tariff cost, a calculation that becomes harder to justify as the tax credit stack deepens as the product moves from manufacturer to buyer to investor. The further up the chain you go, the harder the argument becomes.

A market diverging on technology

Alongside this compliance complexity is a technological divergence that sets the US apart from the rest of the world in ways that are still developing. Globally, the industry has converged rapidly on n-type cell architectures, with Tunnel Oxide Passivated Contact (TOPCon) now dominating new capacity additions across China, Southeast Asia and MENA. Back-contact architectures are gaining ground in premium segments, and the transition away from p-type PERC has been swift and largely decisive across the major manufacturing geographies.

The US market tells a strikingly different story. A significant share of installed domestic module capacity continues to rely on PERC, the p-type workhorse technology that the rest of the world is actively retiring. This reflects the reality that much of the US domestic manufacturing base was rapidly established in response to IRA incentive structures, with PERC offering a lower capital-expenditure entry point for manufacturers racing to qualify for 45X credits before the global technology transition had time to take hold domestically.

More notable still is the direction in which new US capacity is heading. A disproportionately large share of the manufacturing capacity currently under development or recently announced in the US is based on heterojunction technology (HJT). The appeal is not limited to HJT’s efficiency and bifaciality advantages. Critically, it is a technology in which Chinese manufacturers do not hold the same entrenched production dominance they have in TOPCon, making it a strategically attractive bet for US manufacturers seeking to differentiate on both performance and supply chain compliance. However, the main reason for the appeal of HJT is the intellectual property risk exposure that TOPCon faces in the US. The US International Trade Commission is currently undertaking a Section 337 investigation into whether TOPCon solar products imported into the US violate the intellectual property rights of by US thin-film module producer, First Solar. The result is a domestic manufacturing landscape that, in its installed base, runs behind the global technology curve, while, in its new investment, may be positioning itself to sidestep the incumbent supply chain entirely, with TOPCon, the global mainstream, largely absent from the US buildout.

The cell gap remains the defining constraint

Regardless of tier or technology, the fundamental supply constraint endures. As first set out in detail in our previous analysis of the US PV manufacturing landscape, the United States currently has over 66GW of domestic module manufacturing capacity, supplied by just over 11GW of domestic cell capacity, according to PV Tech Market Research data. Combining all FEOC-compliant and AD/CVD-free cell supply globally totals just under 35GW. Even in the impossible best-case scenario in which all compliant cells worldwide are directed to the US market, a gap of at least 20GW remains. Domestic cell producers, including ES Foundry, T1 Energy and Suniva, are ramping, but the timing mismatch between module capacity already in operation and cell capacity still coming online means the market will continue to face serious volatility as manufacturers and developers navigate the complexities of trade restrictions, compliance requirements and supply availability outlined above.

Ultimately, the defining challenge for the US solar market is not module manufacturing capacity, but access to compliant cell supply. With a gap of more than 20GW between domestic module demand and the availability of compliant cells, procurement decisions increasingly depend on understanding ownership structures, trade exposure, technology pathways and manufacturing capacity.

The data and analysis of companies supplying the US market is drawn from the ‘PV ModuleTech Bankability Ratings Quarterly’ report, which provides an independent assessment of the bankability status of leading global PV module suppliers.

US cell manufacturing and procurement will be under discussion at our annual PV CellTech conference in San Francisco on 13-14 October 2026. For the full agenda and booking details, click here.