The global energy landscape is undergoing a dramatic transformation, with solar PV technology at the forefront. Crystalline silicon (c-Si) PV is poised to play the central role in meeting the world’s growing energy demands, potentially supplying 80% of the global energy mix by 2050. This dominance will be defined by technological advancements and the cost-effectiveness of c-Si technology, though there are challenges that must be overcome to achieve this ambitious goal.

Crystalline silicon: the dominant force in solar

Crystalline silicon technology has become the industry standard, accounting for roughly 95% of the global PV market [1]. Its proven reliability, established manufacturing infrastructure, and falling costs have fueled its rapid adoption. While other technologies exist, c-Si’s continuous innovation makes it the leading candidate for large-scale energy production.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

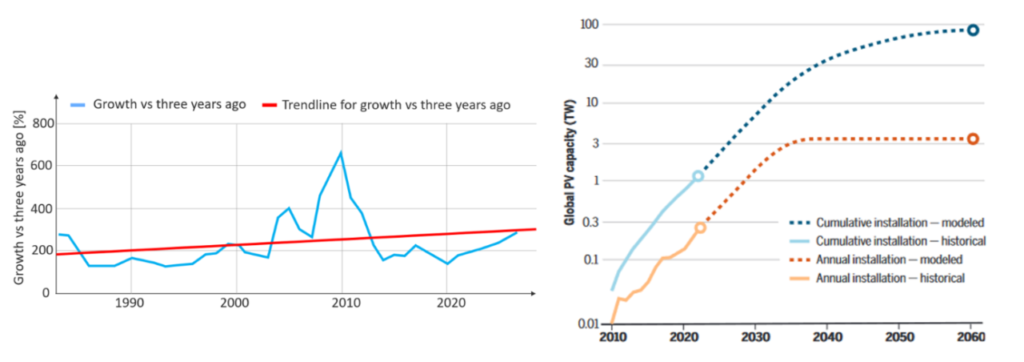

Exponential growth trajectory

PV installations are set to double approximately every three years over the next four decades (see Figure 1 below). While this exponential pace may moderate as we approach 2050, projections still indicate an impressive 80TW of total PV capacity, demonstrating solar’s capacity to meet a significant share of global energy needs. This growth is not just a trend; it is a testament to the technology’s increasing affordability and efficiency

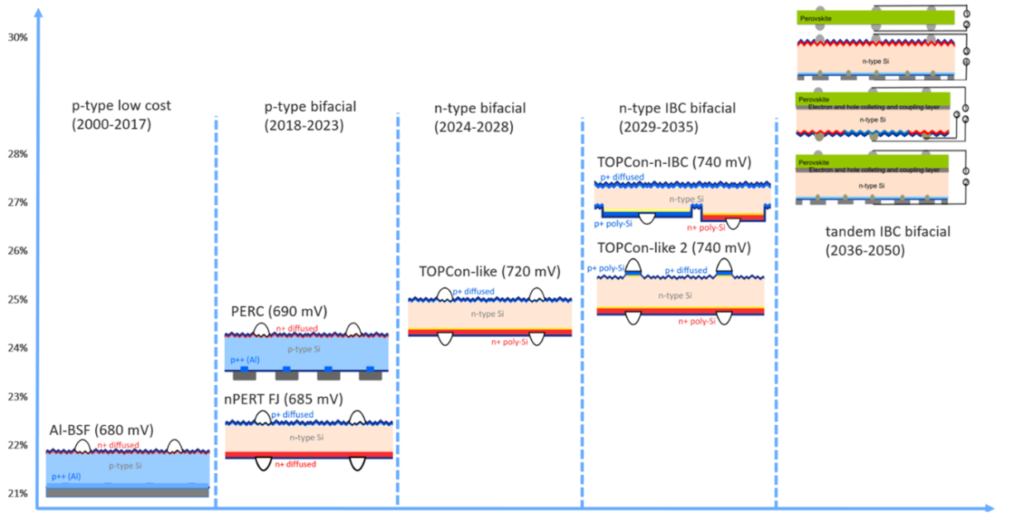

A story of continuous improvement

The success of c-Si technology is rooted in its consistent evolution. Since the 1980s, advancements in cell design and efficiency have defined the progression of c-Si manufacturing (see Figure 2 below).

- Aluminium Back Surface Field (Al-BSF) Era (1980s-2017): This era established the foundational structure, improving efficiency by reducing recombination losses.

- Passivated Emitter and Rear Cell (PERC) Era (2018-Present): PERC revolutionised the industry by incorporating a rear-side passivation layer, significantly improving light absorption and charge carrier collection, achieving efficiencies of 20-23%.

- Tunnel Oxide Passivated Contact (TOPCon) Era (2020s): TOPCon further enhances efficiency (23-25%) by adding a tunnel oxide layer and polysilicon passivated contact, reducing recombination losses and enhancing bifaciality (the ability to capture sunlight from both sides).

- TOPCon-IBC (TBC) Era (Future): Expected to emerge, TBC combines tunnel oxide passivation with interdigitated back contact (IBC) architecture, aiming for efficiencies exceeding 27%.

- Tandem technologies in 2-4 Terminal approach are on the horizon, but, to our understanding, will not enter the market with a high impact (< 10% of market share) as there are still many challenges such as process homogeneity, stability, reverse behaviour and cost.

Even without enhancing the efficiency of conventional single-junction c-Si photovoltaic technology above its practical limit, and with the incorporation of energy storage, c-Si is poised to become the most cost-effective energy source worldwide.

Solar’s cost-effectiveness

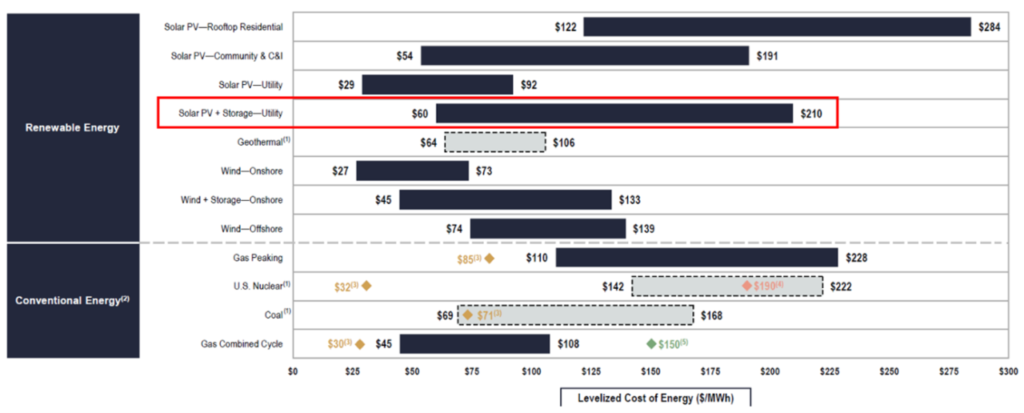

The Levelised Cost of Energy (LCOE) is a critical metric for evaluating the economic competitiveness of energy sources. Advancements in c-Si technology have driven down its LCOE, making solar an increasingly affordable option compared with traditional fossil fuels.

Figure 3, derived from analysis by Lazard, reinforces this point. The report highlights solar PV’s cost-effectiveness as the cheapest form of electricity generation, even when incorporating storage solutions, partially by implementing bifacial tech [3]. The analysis also shows that solar, in several scenarios, can generate power more affordably than natural gas, coal, or nuclear energy, again including the cost of storing electricity.

The declining cost of solar, particularly coupled with energy storage, is reshaping the energy landscape. As fossil fuel costs rise, solar is poised to become the most economically attractive option, revolutionising global energy economics.

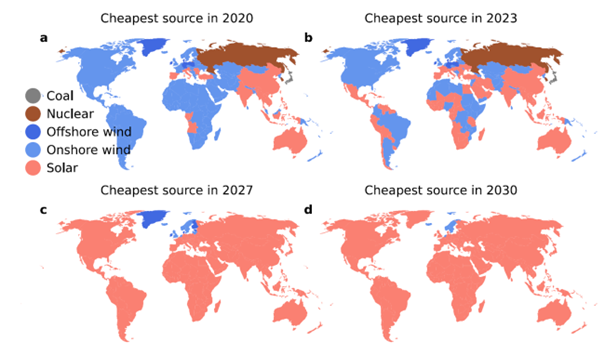

Solar’s increasing dominance

The LCOE values of Figure 4 below, which show PV as the cheapest source of electricity, are expected to emerge in all countries soon. Figure 4 illustrates solar PV’s potential for cost-effective electricity generation worldwide. According to Nijsse et al. [5], fossil fuels are no longer experiencing cost reductions; indeed, they tend to become more expensive.

Consider Pakistan as a case study in how the development shown in Figure 4 can unfold. The impressive 22GWp of PV capacity installed in Pakistan in 2024 [6] is even more noteworthy when considering that the country does not have any feed-in tariff or tax credit for PV. This enormous single-year expansion was driven by sharply decreased prices for PV modules combined with rapidly rising electricity prices for end consumers in Pakistan, which have increased by approximately 160% since 2022. Notably, the vast majority of the 22 GWp was installed behind the meter; only about 3GWp was installed under the net metering scheme in 2024 [7].

This latter fact is significant when considering forecasts from well-known institutions (IEA, BNEF, etc.) regarding the global development of annually installed PV capacity. For over 15 years, these forecasts have consistently – and incorrectly – predicted that the growth pattern shown in Figure 1 (doubling every three years) would not persist into the future. They primarily justify this, especially in recent years, by relying on the increasing difficulty for electricity grids to absorb and distribute fluctuating power generation from PV and wind plants. Scenarios like the one in Pakistan demonstrate the potential for many gigawatts of PV capacity to contribute to a country’s energy supply without having to wait for grid expansions and storage capacity additions. As a result, the competition for the cheapest source of electricity will be primarily between PV and wind energy, with projections indicating PV’s global dominance by 2027. Given that c-Si technology is poised to improve its average module efficiency from 23% (TOPCon) to nearly 26% (TBC) within the next seven years, the growth will be fulfilled without the need to pursue complex and financially unproven tandem technologies. By approximately 2033, a manufacturing capacity of 3TW (as depicted in Figure 2) will be achieved.

A solar-powered horizon

Crystalline silicon PV technology has firmly established itself as a cornerstone of global renewable energy systems. Its continued progress, decreasing costs, and scalability position it as the most practical choice for satisfying the world’s growing energy requirements. While challenges persist, continuous developments in material science, production methods, and recycling technologies are laying the groundwork for a solar-driven future. With solid policy backing and ongoing innovation, c-Si PV technology will play a pivotal role in transforming the global energy landscape, leading the way to a sustainable and economical energy future. In the next 5 to 10 years, establishing local photovoltaic (PV) production beyond China should focus on advanced crystalline silicon (c-Si) technologies, particularly bifacial back-contact (BC) modules.

This objective is a key component of our large EU project, IBC4EU.

A more comprehensive version of this analysis will be published in PV Tech Power soon.

Radovan Kopecek is co-founder and director of ISC Konstanz; Joris Libal is project manager in technology transfer at ISC Konstanz; Wolfgang Jooss is director of technology at RTC Solutions; Peter Fath is CEO of RTC Solutions.

References

[1] Fraunhofer Institute for Solar Energy Systems ISE. (2023). “Photovoltaics Report.”

[2] Haegel, Nancy M., et al. “Photovoltaics at multi-terawatt scale: waiting is not an option.” Science 380.6640 (2023): 39-42

[3] Kopecek, R., & Libal, J. (2018). “Bifacial Photovoltaics: Technology, Applications, and Economics.” nature Energy

[4] 2024 LCOE+ Report, Lazard, 2024, https://www.lazard.com/media/xemfey0k/lazards-lcoeplus-june-2024-_vf.pdf, last accessed on September 15, 2024

[5] Nijsse, F.J.M.M., Mercure, JF., Ameli, N. et al. The momentum of the solar energy transition. Nat Commun 14, 6542 (2023). https://doi.org/10.1038/s41467-023-41971-7

[6] https://cleantechnica.com/2025/04/04/pakistans-22-gw-solar-shock-how-a-fragile-state-went-full-clean-energy/

[7] https://tribune.com.pk/story/2481602/historic-hike-electricity-rates-soar-by-rs-2253-per-unit-over-two-years[8] Bai, X., et al. *”Efficient recycling of quartz crucibles used in solar-grade silicon production.”* Journal of Cleaner Production, vol. 234, 2019, pp. 720-729