During the period 2006 to 2011, equipment spending for solar manufacturing was a really big deal for capital equipment suppliers. Companies such as GT Advanced Technologies (then GT Solar) and Applied Materials (serving thin-film and c-Si expansions alike) were clocking up billion-dollar plus backlogs.

For a short time, these companies – alongside Meyer Burger and centrotherm photovoltaics – were hitting annual revenues at this level. With many equipment companies publicly traded, clear visibility on PV specific revenues, bookings and backlogs was provided, and analysis on market-share and trends was therefore relatively easy to compile.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

This all changed during the overcapacity of 2012-2013, and many of the equipment companies filed for insolvency, folded their PV business units, or wrapped PV tool activities into a more generic sub-segment in reporting. Gone were the days of PV tool metrics to the outside world.

Today, you can count the companies reporting PV-only quarterly solar equipment revenues on one hand, with digits to spare! Fortunately, one of these companies is Amtech Systems (incorporating its main solar subsidiary Tempress Systems).

This blog looks at Amtech Systems (Amtech) solar equipment revenues since the start of 2013, comparing them to the cell capex figures that feature in our bottom-up analysis of PV cell manufacturers, available in our PV Manufacturing & Technology Quarterly report.

We then forecast out what may be expected in 2017, if Amtech’s solar revenues continue to track overall PV cell capex in the same way as the period 2013 to 2016.

By doing this direct comparison, it raises many issues impacting on PV equipment suppliers today, especially those serving cell production, and the fine balance between chasing the new greenfield fabs that are often in new emerging regions (Malaysia, Thailand, Vietnam and Estern Europe) or dedicating sales and marketing efforts to existing capacity upgrades.

Why Amtech is a good match to track PV cell capex today

While, as stated above, the range of companies providing specific solar equipment revenues on a quarterly level is minimal today, the fact that Amtech is one of them is of value.

In particular, the company plays at only one part of the value-chain: c-Si cell production. Also, tool supply covers dominant supply of diffusion furnaces (mainly for new capacity) across both p-type and n-type cell architectures, and solar revenues are a combination of new line installs and (importantly) upgrades.

Therefore, in order to determine if Amtech is a benchmark for PV capex and equipment spending, there should be some kind of correlation between Amtech’s recognized revenues and the cell-specific capex (backed out of upstream capex, covered in the PV Manufacturing & Technology Quarterly report methodology).

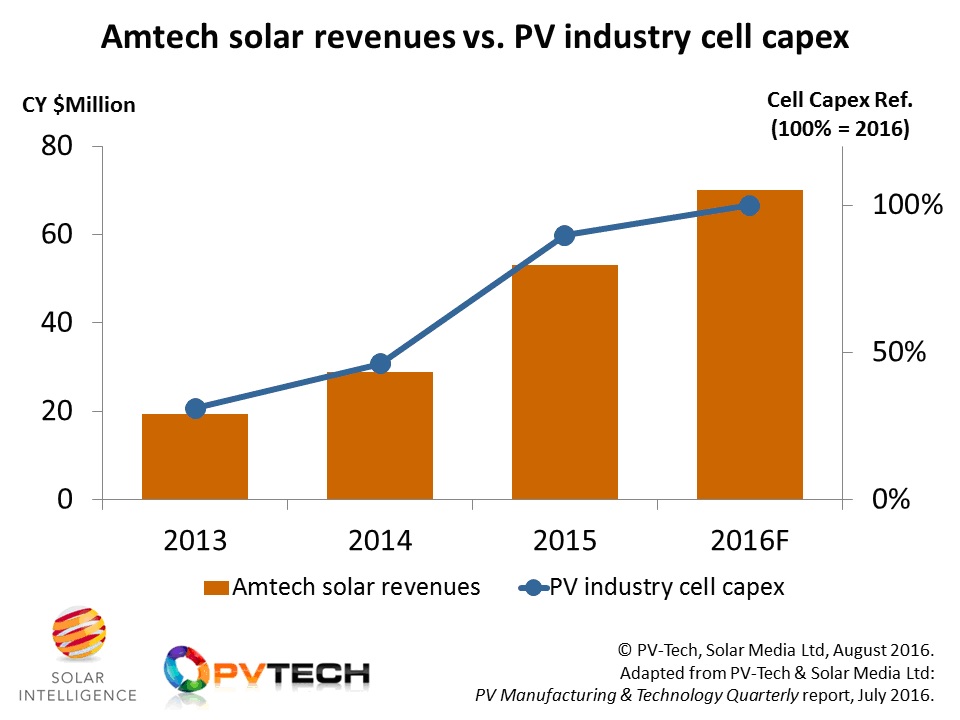

To do this, we have taken calendar year solar revenues from Amtech covering the period from 2013 to 2016. We have modelled out the company’s projected solar revenues for 2H’16, based on backlog and historic tool shipment/rev-rec trends. This is shown in the bars within the graphic below.

Against this, we compare the cell-specific PV capex from the PV Manufacturing & Technology Quarterly report. To best compare the trending, we have normalized the industry PV cell capex total relative to the peak in 2016. This is shown by the line within the graphic below.

In reviewing the correlation above, the match is probably way better than we had envisaged before mapping out the two datasets. In fact, Amtech’s share of PV cell capex during 2013 and 2014 was almost exactly the same (3.5%), before dipping only fractionally to 3.3% in 2015. Our forecast out to the end of 2016 sees Amtech at 3.9% of this year’s PV cell capex allocations.

This explains just how good a benchmark Amtech is becoming when doing a check on PV capex, derived bottom-up from the PV manufacturers’ capex data.

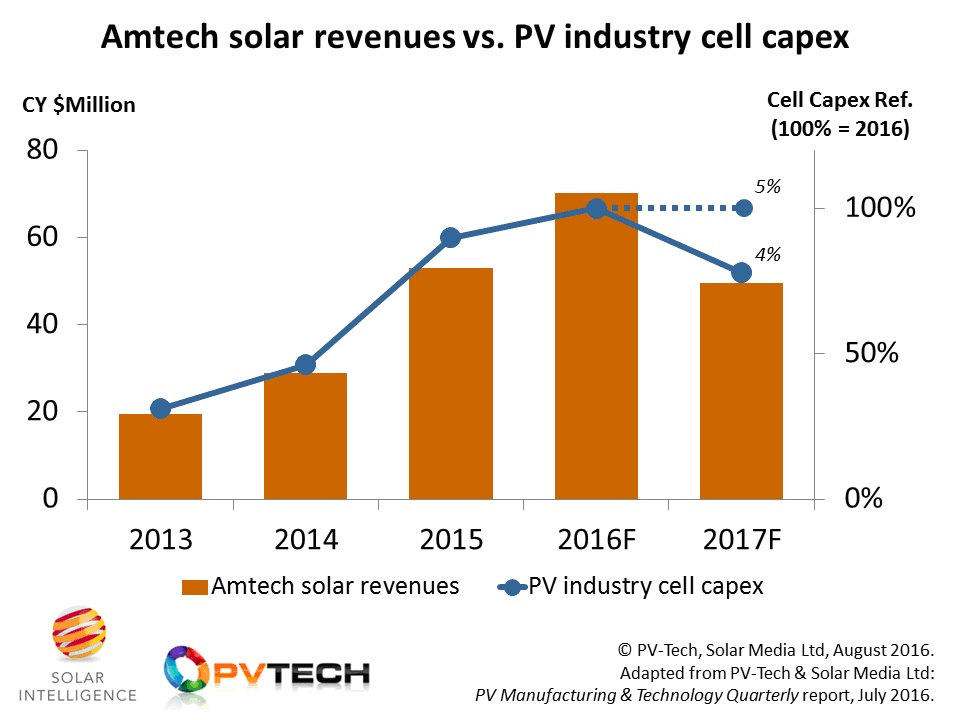

Recently, we discussed on PV-Tech what the expectation was for PV capex during 2017, with an expected decline, most notably at the cell and module stages. Therefore, it is interesting to project the above graphic out by 12 months, this time forecasting Amtech’s solar revenues relative to our forecast for PV cell capex in 2017.This is shown in the graphic below.

To maintain solar revenues at similar levels to 2016, Amtech’s share of forecasted PV capex would need to increase from just 4% to 5%, something that can easily be achieved by winning extra upgrade business to existing cell production lines.

If Amtech’s share of PV cell capex remains close to 2016 levels (circa 4%), then a decline in solar revenues would be expected, given the forecast for PV cell capex to decline to 2015 levels. However, in order to maintain revenue levels static in 2017, relative to 2016, the company would need to increase its share of cell capex from 4% to 5%.

While in the past, having a 25% growth in market-share in relative terms within a 12 month period may have been considered a significant challenge, the PV capex climate today is much more receptive of these changes. This is because a much larger portion of PV cell capex today is coming from upgrade tooling, as compared to new line builds.

Finally, just to emphasize this even more was Amtech’s announcement earlier this week of winning 400MW of new PECVD business (not historically Amtech’s leading tool contribution by revenues) that should be recognized within the next 12 months. A few more of these announcements over the next few quarters would go a long way to getting that capex contribution from 4% to 5%, and potentially bridging to gap during what should hopefully only be a mini downturn cycle for PV equipment spending at the cell level during 2017/2018.

The PV Manufacturing & Technology Quarterly report is released every three months, and is available by subscription, more details on which can be found here.