On 13 April, rumours widely circulated in the Chinese polysilicon market that several PV companies had held a “closed-door meeting” in Chengdu in early April to discuss mandatory polysilicon production cuts, the phasing out of obsolete capacity and coordinating supply chain price support.

The rumours were based on purported minutes of the meeting, which was said to have involved China’s leading polysilicon producers.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Fuelled by the news, the benchmark polysilicon futures contract hit its daily limit in afternoon trading on the same day, closing at RMB34,770/ton (US$5,097). Meanwhile, Tongwei, a leading A-share polysilicon producer, briefly touched its daily limit before ending the session at RMB17.57/share, up 7.86%. Daqo Energy rose nearly 8%, with Hoshine Silicon also posting gains.

In response, reporters sought confirmation from the two polysilicon giants named in the rumours. A representative of Daqo Energy stated that the news was false and that the company had not participated in the meeting. Hoshine Silicon also said it had no knowledge of the matter and “did not attend the meeting”.

A representative of GCL-Tech also denied the news, noting that “the company’s granular silicon cash cost stands at RMB24.03/kg, and it continues to generate positive cash flow at present”.

Lu Jinbiao, a consulting expert at the China PV Industry Association, commented: “At the end of Q1, polysilicon prices fell below the cost levels of leading producers. In Q2, further production cuts and inventory destocking are expected to bring prices back to a reasonable range. Since H2 of last year, industry players have been operating at low utilisation rates, but terminal demand has recovered slowly, and inventory reduction will take time. We must continue to lower utilisation rates, especially among leading companies with large market shares.”

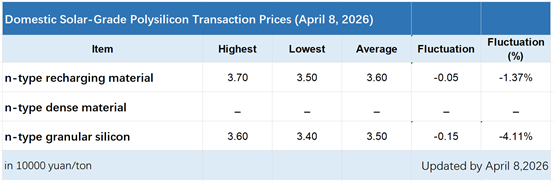

From a fundamental standpoint, polysilicon prices are still bottoming out. According to data released on 8 April by the Silicon Industry Branch of the China Nonferrous Metals Industry Association, the average polysilicon transaction price has fallen for six straight weeks.

For n-type recharging material, the trading range settled between RMB35,000 and 37,000/ ton, with the average price hitting RMB36,000/ton—a month-on-month decrease of 1.37%. Meanwhile, n-type granular silicon traded at RMB34,000 to 36,000/ton, with an average price of RMB35,000 yuan/ton, marking a 4.11% month-on-month decline.

The Silicon Industry Branch stated that the overall downward trend in the market has yet to reverse, with intensifying bargaining between buyers and sellers. Downstream buyers remain strongly inclined to push prices down, while suppliers still intend to hold prices firm. The core issue remains the supply-demand imbalance. The “buy on upticks, not on downticks” wait-and-see downstream mentality continues to grow, with purchasing frequency already shortened to weekly intervals.

According to the Silicon Industry Association, domestic polysilicon output reached 92,600 tons in March, up 9.7% month-on-month. April output is estimated at 85,000 to 86,000 tons, representing a month-on-month decline of around 8%. That said, demand remains weak, so meaningful inventory destocking across the industry will be difficult to achieve.

")