Just when it looked like the underlining trend for Tesla’s shift away from using third party mainstream solar panel suppliers was set in stone, as manufacturing partner Panasonic started ramping Gigafactory 2 production, the latest data for the third quarter of 2018, goes completely in a different direction.

Inverter and smart energy manufacturer SolarEdge has a back catalogue of solar-themed parody videos but this year’s effort, Solar Joy, has raised the bar.

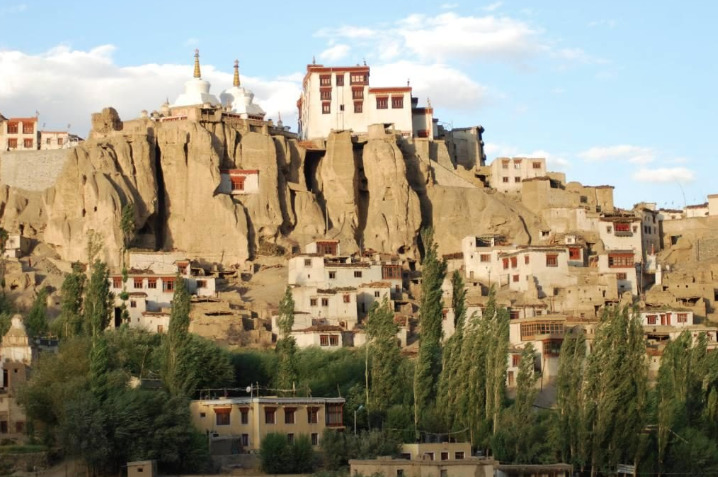

PV Tech looks behind last week's Indian government announcement that it would issue a 7.5GW solar tender in the high altitude mountain desert region of Ladakh.

Technology investments into advanced PV cell manufacturing have been at record levels in the past few years, with high-efficiency concepts seeing investment levels not seen since the days of turn-key thin-film lines a decade ago.

Finlay Colville, head of market research at Solar Media, details precisely how the UK’s post-subsidy solar pipeline has soared to just shy of 3GW, while simultaneously forecasting something of a revival for UK solar in 2019 with 500MW to be developed.

While Filipino policymakers ponder a controversial bill that would allow a solar company to set up a micro-grid and transmission franchise aiming to improve power supply across the country, a small town on the island of Mindoro is already enjoying round-the-clock electricity for the first time ever.

The solar industry gets to grips with the bewildering array of new module technologies at the second edition of the PV ModuleTech event in Penang, Malaysia. The conference raised a huge number of questions such as how to evaluate bifacial technology and whether it might rise faster than predicted, how long p-type multicrystalline has left in the running and the perennial issue of quality, to name a few.

SPONSORED: Emerging module technologies offer greater opportunities for differentiation among suppliers, but reliability will always be the key metric for Chinese manufacturer Astronergy.

PV manufacturing capacity expansion announcements in the second quarter of 2018, were slightly higher than the previous quarter, although activity slumped specifically in June, after China’s decision to suddenly cap utility-scale and distributed generation (DG) projects (531 New Deal). But large-scale multi-gigawatt production plans in the first half of the year may have hidden an inevitable slowdown, despite the impact on downstream demand from the 531 New Deal.