The second day of our inaugural PV CellTech conference in Kuala Lumpur on 17 March 2016 turned out to be equally informative, engaging and thought-provoking as day one. Among the many takeaways from the two-day event in general, the final session addressed head-on one of the most hotly debated issues in the industry today – the technology roadmap!

Within the 17 presentations, day two saw CTOs and heads of R&D and cell production from JinkoSolar, Panasonic Corporation, GCL System Integration, First Solar (TetraSun) and Yingli Green Energy. Sessions included a fascinating two-hour period on n-type cell production, half of which was specific to heterojunction, including a great talk by Panasonic with efficiency breakthroughs so far in 2016.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

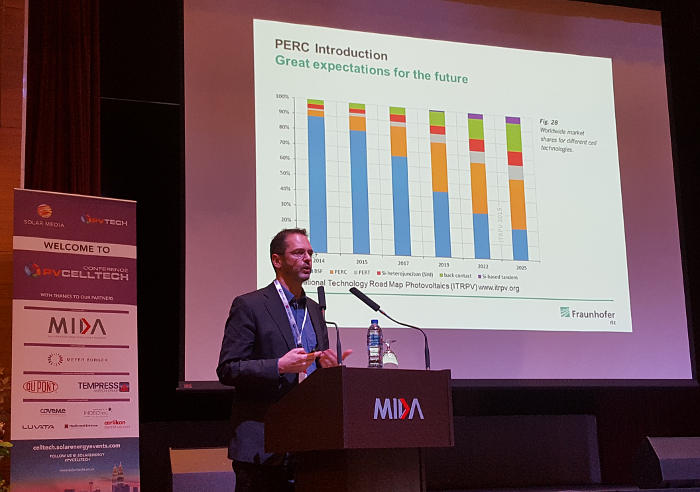

But the end of the session was perhaps the most illuminating, as it featured talks on “what next”. And within this was Markus Fischer of Hanwha Q CELLS who chose the PV CellTech conference platform to launch the latest edition of the ITRPV roadmap. This was complemented by our own in-house forecast for PV cell production and capex, looking in detail out to the end of 2018.

The overall conclusions from the different methodologies are starting to emerge as being really good ways of looking at the industry, with each offering key findings in different areas, and certainly on a different level from almost all other market research studies from the solar industry that are very much geared to what is happening at the policy level for downstream end-market demand forecasting.

It is probably not too much of a surprise that this conclusion was reached yesterday at the end of the PV CellTech conference. Generally to forecast technology, you need to understand it in the first place, and that takes many years of being in the industry in order to have any credibility with the companies and research institutes that are in reality doing the work in production.

As we got to 5pm and the event finished, it suddenly dawned on me that the audience in that one room in Kuala Lumper was not simply discussing the PV technology roadmap – it was the PV technology roadmap.

I have thought for years – wouldn’t it be great if you got all the CTOs and heads of cell processing from all the leading cell producers in the industry, add in the heads of the main PV research institutes, and have the most important equipment and materials suppliers alongside them.

Welcome to PVCellTech 2016 from the past two days

The ITRPV roadmap takes on a daunting task – what will the technology of the PV industry look like in 10 years! It is a massive challenge, and as Markus Fischer highlighted succinctly in his talk yesterday, it is best not to get hung up on the exact percentages for different technology metrics 10 years from now, but more to look at the trends and which options are possibly going to gain or lose share of the market. It draws heavily on a blend of industry experts to form a long-term picture, not so much diving into what may change right now on a quarterly basis. Possibly, it has most use from a long-term strategy perspective.

Our new in-house cell technology roadmap methodology at Solar Media, the parent company of PV-Tech, does things in a very different way by looking closely at a shorter time period, confining to the most recent past and the near term, and having a quarterly breakdown across a different set of metrics. In fact, we do this by following capex and other measurables that are leading indicators of what is changing right now, not 10 years from now. As a complement to the ITRPV roadmap, our technology findings are probably more tactical in nature and impacting on activity going out 1-2 years.

We will be discussing the findings of the conference in much more detail over the next few months, as there is much to ponder from all the speakers and discussions during the day and into the evenings. And with the launch of our new PV Manufacturing & Technology Quarterly report just last week, doing side-by-side analyses of the conference topics and the report findings.

The two most important questions though from the conference were, beyond a shadow of doubt, these two very simple options:

• p-type or n-type

• mono or multi

And thinking the day after, I am actually delighted about this. If we had started off the PVCellTech conference two years ago, the questions may have been: when is capex going to come back, why is nobody prioritising cell technology today, or who is going to be around in five years time?

The fact that almost every CTO or head of cell technology came to the event and (within entirely reasonable limits of confidentiality) wanted to discuss the challenges behind getting efficiencies for all cell variants north of the 20% mark is maybe due in part to the realisation that it is much easier to move production metrics forward by being part of a dialogue with your competitors, than to talk to no-one and gamble in doing it all yourself. Few win going it that way alone.

Since the early research phase leading up to 2005, how long has the PV industry waited for this to happen?

Well, the answer is 11 years. And during this 11 years, there have been many bankruptcies, failed technologies and aborted efforts to move R&D into mass production way too early.

It is way too early of course to say that we have just arrived in a brave new world of openness, but the signs are certainly there, and you could actually feel that something was really happening over the past two days that is going to be fascinating to watch from a technology standpoint.

Given the bashing the solar industry often gets in the mainstream press from its financial dealings, government squabbling and employee redundancies, it would simply be a breath of fresh air to see any type of collaborative effort to really drive technology forward and the day when people talk about solar fabs in the same way they measure semiconductor industry metrics.

If PV CellTech can play just a small part in getting there by being the mechanism that makes sure all the relevant stakeholders are under the same roof for two days every year, and forces the talks and presentations to confront the right issues head on, then it will have more than served its original aims.

The only downside is I now have to wait 51 weeks to find out the answer to this by way of PV CellTech 2017! But that gives plenty of time to try work out what it all means.