As federal permitting delays mount in the US solar sector, project economics are under increasing strain, with a 100MW project facing US$10–18 million in added development costs, which are often passed on to consumers.

Published earlier this month by clean energy platform Crux, ‘The Impact of Federal Permitting on Clean Energy Development’ draws on a survey of 50 renewable energy developers across the US and finds that the current policy landscape is not only slowing the rollout of new solar and wind capacity but also increasing costs across project pipelines.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Among the 50 respondents, federal permitting delays have held up 11GW of new renewable energy deployment in the US over the past year, while adding up to 10% to project development costs, according to Crux.

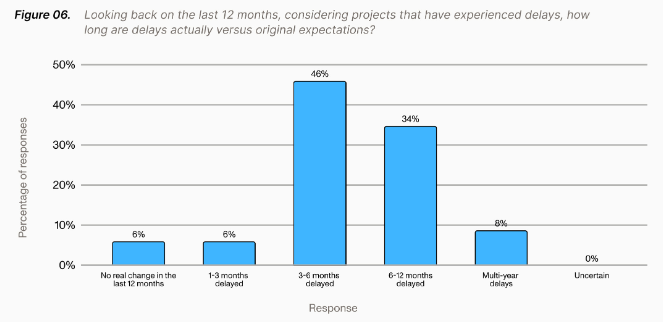

The findings highlight widespread disruption, with 94% of respondents reporting delays of at least one month over the past year, and nearly half (46%) experiencing delays of three to six months. At the same time, cost pressures are mounting, with the majority of developers reporting increases of 6-10%, and none indicating that permitting had no impact on project costs.

The report also points to a more structural shift in developer behaviour, with 82% of respondents saying they had altered project siting specifically to avoid triggering federal permitting requirements, raising concerns about inefficiencies in how and where energy infrastructure is being deployed.

PV Tech Premium spoke to Hasan Nazar, head of policy at Crux, and Nathan Smith, senior credit analyst at Crux, to explore the findings in more detail, including the growing importance of predictability in the permitting process and what these challenges could mean for the future of the US clean energy transition.

Unpredictability at the heart of permitting challenges

Developers are not primarily calling for faster timelines, but for greater certainty in how the federal permitting system operates.

Nazar notes: “The single change that developers would most like to see in the permitting system is simply a more predictable outcome with clear requirements and consistency in decision making,” noting that other options “were far lagging relative to the 72% that said more predictable outcomes matter.”

He describes a system where approvals do not guarantee progress. “You can have what you believe is all the requisite approvals to move forward with a project,” Nazar says, “and once steel is in the ground and you’re halfway through, something else pops up because of how expansive the process is.”

These late-stage disruptions—ranging from Endangered Species Act (ESA) to National Historic Preservation Act concerns—can “stop a project in its tracks, extend the timeline and effectively kind of stymie the whole project,” he adds.

For developers, the core issue is the inability to plan with confidence. Nazar highlights that projects are exposed to long-term risk because “they do not know if they are going to have a partially built stranded asset in two, three or four years if they start building now.”

This lack of clarity also plays out in the process itself. Smith adds that developers often enter permitting “not having any idea when it ends,” with projects getting caught in “unclear or exceptionally long timelines, National Environmental Policy Act (NEPA) review, inter-agency coordination requirements, ESA consultations and agency non-response.”

Ultimately, Smith says, “where projects are getting held up is in procedural aspects of federal permitting,” reinforcing that unpredictability—not just duration—is the defining challenge.

Delays, costs and distortions across the project pipeline

The survey highlights the scale of disruption, with 11GW of delayed projects identified across 50 developers—though Nazar stresses this is only a partial view. “It is 11GW that track to the 50 respondents in the survey,” he said, adding that “the number is assuredly much higher.”

Delays are widespread, with 46% of respondents reporting setbacks of three to six months and a further 8% facing multi-year delays. But beyond timelines, developers are increasingly reshaping projects to navigate the system.

According to the survey, 82% of respondents have altered project siting to avoid triggering federal permitting. Nazar describes this as “a clear market distortion that is underappreciated.”

“What is driving where energy is being built appears to be more about regulatory avoidance versus where energy is actually needed,” he says, warning that this trend is particularly problematic in regions with significant federal land and high energy demand.

He adds that the full impact is not captured in official data. “The true cost of the issues related to the federal permitting system is systematically undercounted, because the projects that never get built don’t really show up in the data.”

At the same time, permitting challenges are adding costs across entire development portfolios. Smith emphasises that the survey examines “what the cost implications of federal permitting are on projects as a whole,” noting that most respondents are managing large pipelines, with “the large majority of them [having] more than 1GW of projects planned for 2026.”

As a result, developers are not assessing projects in isolation. “They’re thinking about it as part of their overall portfolio,” Smith says, underscoring how delays and uncertainty ripple across investment strategies.

Mounting pressure on reform amid rising energy demand

The findings come as policymakers revisit permitting reform against a backdrop of structural change in the energy system.

Nazar explains that the survey aims to “inform what is a very live discussion around bipartisan permitting reform talks,” as clean energy takes a more prominent role in the pipeline.

Historically dominated by oil and gas, the system is now shifting, with Nazar noting that “as of 2024, over 60% of the electrons in the queue in NEPA are for clean energy projects.”

At the same time, broader economic and geopolitical pressures are intensifying the need for faster deployment. Nazar points to “a strong push to onshore as much of the critical supply chain, including energy supply chains, as possible,” alongside “organic growth in electricity demand.”

These dynamics are reinforcing the importance of energy as a strategic priority. “The through line for all of this is energy,” he says, highlighting both affordability and national security considerations.

Against this backdrop, developers are clear about what needs to change. Nazar says “clear requirements and consistent decision making is incredibly important,” adding that if the process were predictable, “there’s a lot of tolerance” for complexity and rigorous review.

Instead, uncertainty continues to deter investment. As Nazar put it, “a quick no is better than a long yes,” arguing that developers would rather redeploy capital than remain stuck in prolonged approval cycles.

The stakes for the energy transition are significant. With policy support already shifting, Nazar warns that maintaining permitting barriers could have a compounding effect. “If you reduce that support for those technologies, and at the same time keep in place a barrier for deployment, it is effectively a double whammy. There’s going to be less deployment at a time where we need it most.”