Recently, I wrote an extensive article on PV Tech about the looming solar PV manufacturing downturn in 2024, ‘Can anything prevent a PV manufacturing downturn in 2024?’

The article showed that the leading indicators today for PV manufacturing are strongly suggesting that next year almost all the crystalline-silicon (c-Si) based suppliers are going to struggle to operate at break-even status, or simply accumulate significant operating losses during the year.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

In this article, I forecast that only one major PV module supplier will largely be immune to the chronic overcapacity and pricing declines impacting the c-Si sector. Moreover, this company is set to have potentially its most prosperous year ever and could emerge as the only leading module supplier globally to accumulate retained earnings by the end of 2024.

The company in question is First Solar.

The rest of this article seeks to explain the timing of First Solar’s probable golden year in 2024 and why the concurrent c-Si downturn could be a catalyst in forcing policymakers and other key industry stakeholders to reset their global competitive strategies going forward.

In this respect, I focus on two of the key metrics that could define 2024, if it does end up being a chronic downturn period for c-Si based manufacturers: capital expenditure (capex) and return on assets. Specifically, I show trends for these parameters going back more than ten years, comparing First Solar with the four major Chinese global module suppliers during this period (JinkoSolar, JA Solar, Trina Solar and Canadian Solar). I have excluded LONGi Green Energy from this China grouping for two reasons: a later entry into the sector as a module supplier, compared to the other Chinese companies listed before; and a business model that has significant revenue streams from non-module-based sales (in this case wafers).

To get the full picture however, it is necessary to forecast each of these companies/groupings (across all manufacturing and financial metrics) out to the end of 2024, based on a range of assumptions (yet to happen of course), at the company level and across the industry/landscape as a whole. Therefore, there is plenty of risk to this: but even more so – as in the case largely of the c-Si based sector – the underlying assumptions for 2024 are based on this being a year of a c-Si specific manufacturing downturn that could be more than six months away in terms of company reporting.

Why 2024 for First Solar?

Over the past few weeks, this is a question I have been thinking about and how best to summarise my thoughts.

After more than 20 years of upstream PV manufacturing, being the only survivor out of a tumultuous thin-film investment phase that saw hundreds of casualties, having had an on/off upstream/downstream business model that was finally ended in order to allow for pure-play module operations, and being the only meaningful alternative of recent to the PV industry being entirely c-Si and Asian-controlled: I rephrase the question: why 2024? And just as the silicon-based sector could be set for a potentially chronic downturn in fortunes?

There are a few basic reasons I think fortunes are set to peak soon for First Solar, and one very striking one explaining why 2024 will likely see the highest earnings reported in the company’s history. Interestingly – and while not fully decoupled – I think the timing of the silicon-based industry’s likely malaise next year is mostly coincidental (although it was likely to happen at some point in the near future, if not 2024).

Again, while not specific to 2024 being the year in question, one of the most important decisions by First Solar, contributing to its current uptick in fortunes, was when the company committed fully to being a module supplier back in 2016. This was not a foregone conclusion. At the time, there was likely a plausible argument to exit the manufacturing space and concentrate on downstream operations. In the end, module manufacturing won through, and the rest is history.

This leads us nicely onto capex; why this captures First Solar’s post-2016 existence, and how it compares to the main Chinese competition (labelled here China Top-4 c-Si, or just shortened to China Top-4).

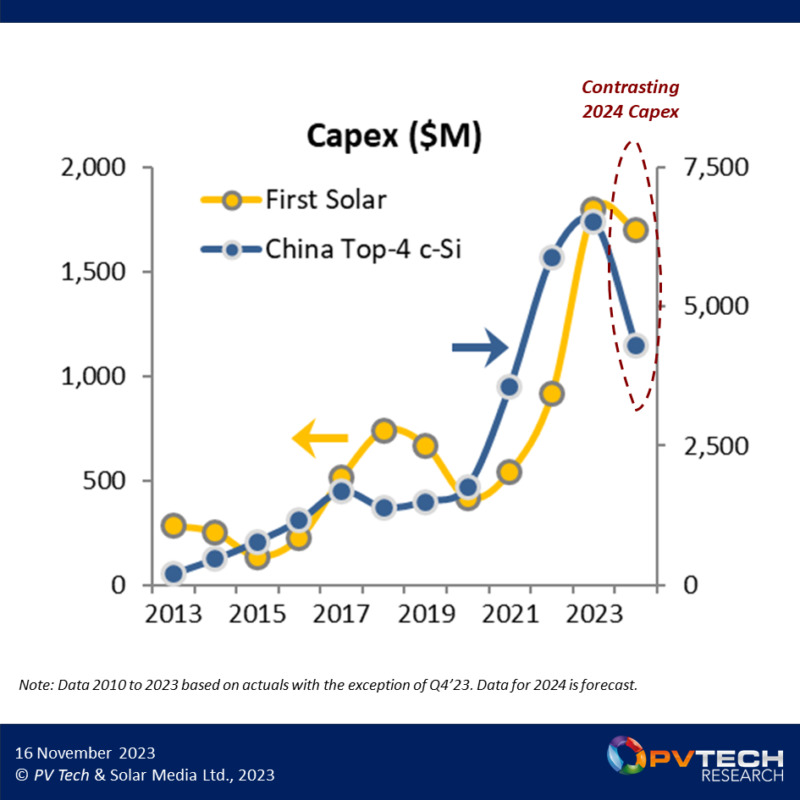

Figure 1 below shows First Solar’s annual manufacturing capex back to 2013 and forecast out for 2024. Plotted alongside is the cumulative manufacturing capex for the four Chinese module suppliers noted above and labelled in the graph legend as China Top-4 c-Si. In the case of the c-Si capex, this includes spending across the ‘equivalent’ value chain to First Solar: ingots, wafers, cells and modules.

In figure 1, First Solar’s annual capex is shown by the yellow line, plotted on the primary vertical axis to the left. The cumulative capex of the China Top-4 is shown in blue on the secondary (right) axis.

Since 2019, capex from both First Solar and the China Top-4 has increased significantly, with 2023 levels for each about three to four times higher than just a few years ago (2020).

However, in 2024, I expect to see the capex trajectories of the two to start to move apart. First Solar is almost certain to keep spending at current record highs for the company, largely on the back of new fabs under construction now in Alabama (slated to come online in 2024) and Louisiana (2025). From a risk standpoint, the spending allocations for capex in 2024 from First Solar are largely a tick-box exercise, and one could probably also say this with confidence for 2025 too.

By contrast, forecasting the capex from the China Top-4 grouping in 2024 is far from a done deal, and this could play out in many different ways. Most of the intended capacity expansions planned from JinkoSolar, JA Solar, Trina Solar and Canadian Solar in 2024 are coming from another round of massive capacity additions in China, with partial spending across countries in Southeast Asia (Thailand, Malaysia and Vietnam in this case) and even lower allocations to GW-scale module-level additions in the US.

Looking at the expected capex from this China Top-4 grouping in 2024, the uncertainty today comes from how much new capacity each wants to add in mainland China, not in Southeast Asia (so long as the tariff landscape to export to the US here is favourable), and not in the US (although the real capex in the US during 2024 is nowhere near the ‘investments’ quoted by these companies of recent).

For Trina Solar and Canadian Solar, there is the additional question of how much ingot, wafer and cell capacity in China will be added next year. These companies are more likely than JinkoSolar and JA Solar to pause on non-module capacity additions and have a flexible wafer/cell supply policy, as has been their modus operandi in the past.

Currently, none of the China Top-4 has fully committed to capex guidance for 2024. Even in a good year, it is normally not until March/April each year that the annual capex levels start to be discussed openly. If 2024 is going to be the downturn for c-Si manufacturers I predict, then one could expect that dodging the capex question will become commonplace for the foreseeable future.

Regardless of whether the China Top-4 go on the record or not with 2024 capex allocations, I would expect that the brakes are put on the China expansion build outs, or that some of the planned investments are cancelled altogether. The net result of this is that the cumulative capex from JinkoSolar, JA Solar, Trina Solar and Canadian Solar is likely to fall by anywhere from 30% to 50% in 2024 and maybe even also (but to a lesser extent year-on-year) in 2025 (although we are definitely a way off from this call now).

As the sole custodians today of China-owned/US-listed company reporting, it may be that JinkoSolar and Canadian Solar are the ones forced to address the capex question the most, of all the Chinese-owned c-Si companies.

As such, we are probably about four to six months away from knowing conclusively whether or not the c-Si industry-wide capex declines I am predicting for 2024 will come to fruition. During this period, there is likely to be no shortage of data points that help in building up the overall picture.

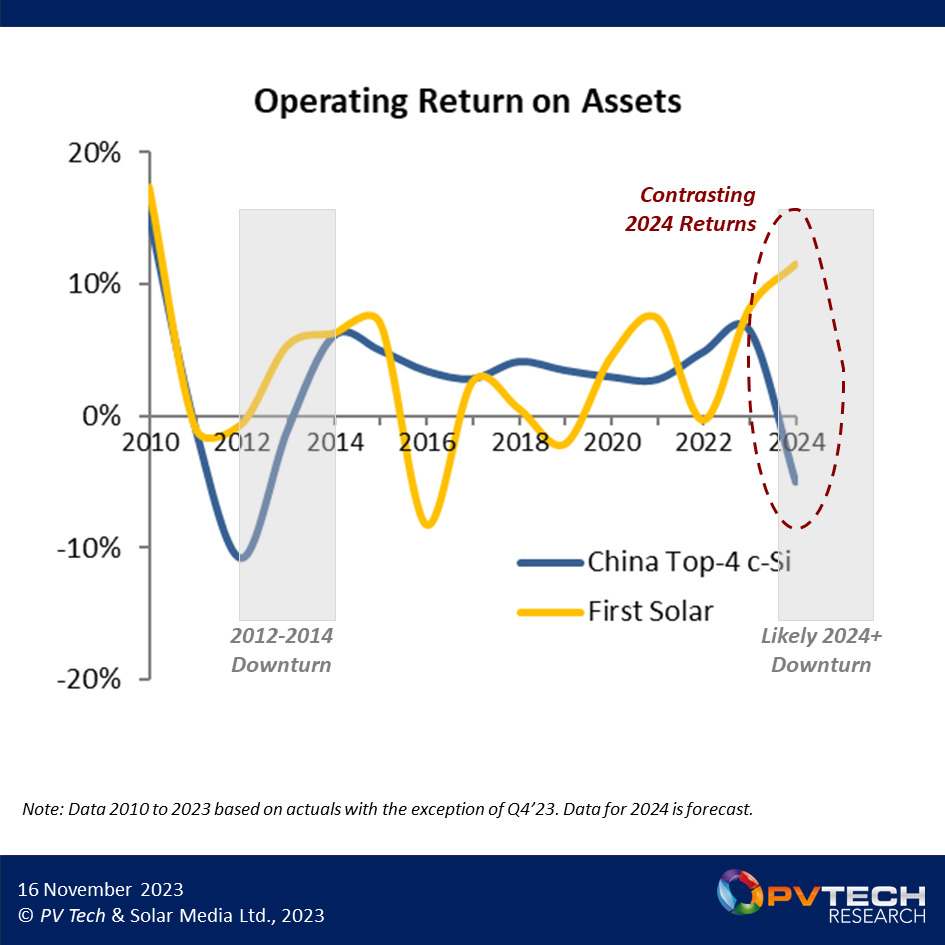

The other metric I alluded to at the start of this article was ‘return on assets’. In fact, this is just one of a host of profit-related accounting ratios that is used in practice to view company-specific operations, or in comparison to industry peers.

Actually, the metric I use in the following comparison of First Solar to the China Top-4 is ‘operating return on assets’. It turns out that using operating returns, as opposed to net returns or EBIT (earnings before interest and taxes), is a better metric when factoring in some of the changes in US/non-US accounting practices. Trina Solar and JA Solar are listed in China; JinkoSolar and Canadian Solar have their manufacturing activities in owned entities in China also now.

This is a small nuance to be honest. If I had used net income/loss or EBIT based ratios, the key findings would have been similar. For now, simply view the following discussion on how profitable the companies are, relative to their size (total assets).

Ratioing operating returns to total assets is important to get a benchmark of profitability. In the case of the China Top-4, the final return on assets percentage is derived by using the sum of the operating returns of all four and dividing this by the sum of the total assets of all four. (In effect, fully weighted.)

Similar to the capex benchmarking above, I have used a bunch of assumptions to get to the final operating returns for the year (2024), and the average total assets during this 12-month period. Again, remember this is a tough forecast at any time, far less on the brink of a downturn; so it is best to look at the trends for 2024, as opposed to the exact numbers shown below.

Figure 2 now compares the annual operating return on assets for First Solar and the China Top-4 grouping, going back as far as 2010.

In figure 2 above, one can clearly see that the fortunes of First Solar and the China Top-4 dipped during the last industry downturn of 2012-2014. Between 2014 and 2022, it is not entirely a direct comparison, as First Solar’s cycles here are more a function of the company going through various operational changes with some of the highs being influenced by the timing of legacy downstream revenues or project (or owned pipeline) sales. However, the trajectory of the China Top-4 during this (upturn/prosperity) period (for the industry as a whole) is more representative of how many c-Si based manufacturers operated.

However, what happened in 2023 to each of First Solar and the China Top-4 could not be more disconnected. Almost to the point where each was in principle doing the same thing (selling PV modules), but in reality operating on totally different trajectories.

The full narrative of what happened to the c-Si sector (including the China Top-4 grouping) was covered extensively in my article a few days ago on PV Tech: ‘Can anything prevent a PV manufacturing downturn in 2024?’

Conversely, in 2023, First Solar seemed to have the stars come into alignment. Unprecedented demand for its modules in the most desirable end market in the world today (the US), on-time ramp up of almost all new or upgraded production lines, Series 7 costs by year-end matching the legacy Series 6 production lines, and the pièce de résistance – a gilt-edged 17c/W incentive for US manufactured product courtesy of the Inflation Reduction Act (IRA).

It is hard to imagine how 2023 could have been better for First Solar. But it is in 2024 that this will all fall into place, at least to the outside world.

I actually think that this was going to happen for First Solar, irrespective of the likely downturn in 2024 for the whole of the c-Si segment. But now, the contrast in fortunes in 2024 is probably going to look all the more dramatic. The consequences of this could be far reaching.

For now, I am going to pause on this last comment. Let’s wait and see what unfolds in 2024, or at least until there are enough datapoints to support my 2024 predictions. There will be curveballs, of course. The question is whether they stop 2024 becoming a year when First Solar flies high, and for a while at least, the Western world has a success story and a non-China/non-silicon narrative to champion.

To subscribe to PV Tech’s Market Research reports, the PV Manufacturing & Technology Quarterly report or the PV Moduletech Bankability Ratings Quarterly report, please contact us here. To understand how the contents of this article are likely to impact PV module buying in Europe in 2024, you may wish to attend our forthcoming PV ModuleTech Europe 2023 conference in Barcelona, Spain on 28-29 November 2023, attendance details for which are here.