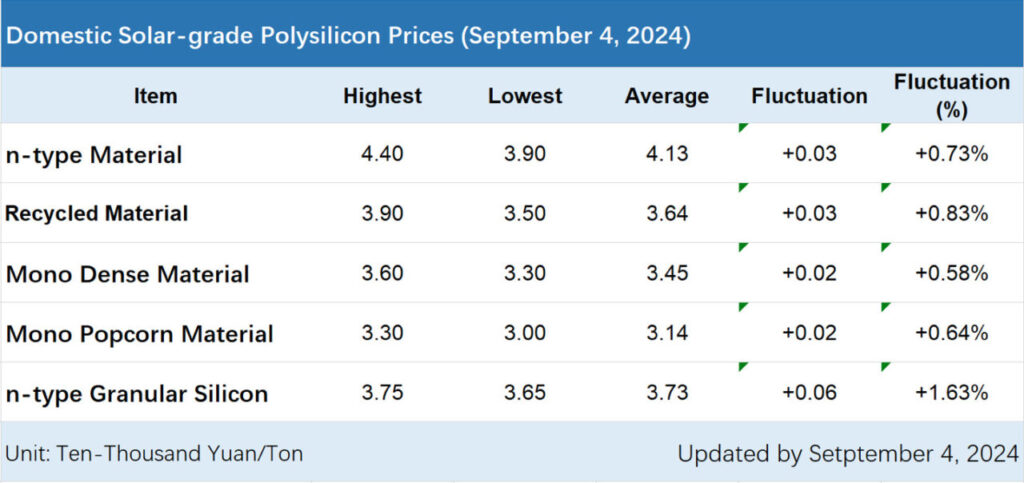

On 4 September, the Silicon Industry Branch of the China Nonferrous Industry Association announced the latest polysilicon prices, with a slight increase in silicon material prices across the board this week.

Among them, the transaction price range for n-type rod silicon is RMB39,000-44,000/ton ((US$5,481-6,184), a month-on-month increase of 0.73%; the transaction price range for mono dense material is RMB35,000-39,000/ton, averaged at RMB34,500/ton, a month-on-month increase of 0.58%; the transaction price range for n-type granular silicon is RMB36,500-37,500/ton, averaged at RMB37,300/ton, a weekly increase of 1.63%.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

According to the Silicon Industry Branch, the current polysilicon price has risen across the board. The mainstream orders signed are mainly n-type silicon products or mixed-packed materials. Only a very small number of companies have separate p-type materials for sale, and the prices of these products have risen to some extent. Due to its price advantage, the demand for granular silicon orders is high and the margin available for sale is relatively tight, leading to a slight price increase.

According to the Silicon Industry Branch this round of price rises is mainly supported by two factors: on the one hand, after the concentrated maintenance and load reduction in August, supply had reached a historical low for this year. In September, some companies planned to increase or resume production, so during the short period when supply-demand pressure is at the lowest, the silicon material companies are willing to maintain the price.

On the other hand, a slight increase in raw material price is acceptable. The price of downstream wafer sector also increased accordingly. Therefore, at present, polysilicon companies have relatively consistent price increase expectations, and quotations to downstream suppliers, future deals and spot deals all increased. However, the transaction volume this week is limited, resulting in only a small increase in the average market price.

Statistics show that the domestic supply of polysilicon in August was about 129,700 tons, a month-on-month decrease of 6.01%. Polysilicon supply in September is expected to remain at about 135,000 tons.

Price drop, capacity release, polysilicon companies’ performance is under pressure

It is worth noting that leading companies in silicon materials and wafers have recently released their semi-annual reports for 2024. Companies that previously flourished have begun to lose money. The profits in H1 of this year of Tongwei, GCL Tech, Daqo and Xinte Energy are all negative.

The other side of price and performance is the continued release of polysilicon capacity. According to statistics from the Silicon Industry Branch, in H1 of 2024, China’s polysilicon output was about 1.0687 million tons, a year-on-year increase of about 64%.

In the face of a complex and changeable market environment, polysilicon companies have all taken active measures to improve polysilicon quality and cost reduction, enhancing their operational resilience during the hard times. Under the operating pressure of upside-down costs, some companies are also looking abroad for additional demand.

In June this year, GCL Tech announced that the company is exploring potential cooperation opportunities with Mubadala Investment Company PJSC. The first overseas FBR granular silicon project will land in the United Arab Emirates. Once completed, it will also become the world’s largest polysilicon R&D and manufacturing base outside of China.

Following the successful development of overseas markets in 2023, Daqo stated that, “Daqo will continue to increase its efforts to develop overseas markets, strive for overseas orders, and ensure that it maintains a certain profitability amid market price fluctuations.”

")