The global PV inverter industry is undergoing a profound transformation, driven by evolving policies and regulations aimed at reshaping the renewable energy landscape. These policy shifts are influencing manufacturing strategies, supply chains and market dynamics across key regions. This article explores the critical policies across various regions around the world affecting the PV inverter sector and their implications for manufacturers and markets. Leveraging insights from our in-house market research team and the ‘PV InverterTech Bankability Ratings Report‘, this article uses analysis of the leading 26 companies in the utility-scale PV inverter market.

Key US policy changes driving industry transformation

A combination of trade tariffs and legislative measures is helping bolster the US solar inverter manufacturing landscape by making domestic production increasingly competitive. Section 301 tariffs impose duties ranging from 7.5% to 25% on Chinese-manufactured goods, including photovoltaic inverters, significantly increasing the cost of imported equipment. These tariffs create immediate price advantages for domestically produced inverters and incentivise manufacturers to establish US-based production facilities to avoid these additional costs.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The Inflation Reduction Act (IRA) reinforces this shift through its tax credit structure and Foreign Entity of Concern (FEOC) restrictions. Under the IRA, solar projects can access a base 30% Investment Tax Credit (ITC), with an additional 10% domestic content bonus available for projects that meet minimum US manufacturing thresholds. More critically, FEOC rules—which took effect 1 January 2026—restrict tax credit eligibility for projects using components from Chinese or other prohibited foreign entities above specified percentage thresholds. These thresholds tighten progressively each year, effectively creating a compliance timeline that pushes developers toward non-Chinese supply chains.

For inverter manufacturers, this policy environment creates a strong market pull: companies that establish US production facilities can offer products that help developers qualify for maximum tax credits while avoiding tariff costs. This dual pressure from tariffs and FEOC rules is driving major inverter manufacturers to invest in American manufacturing capacity, favouring localised production. These measures primarily impact major manufacturing hubs such as China, the United States and Europe.

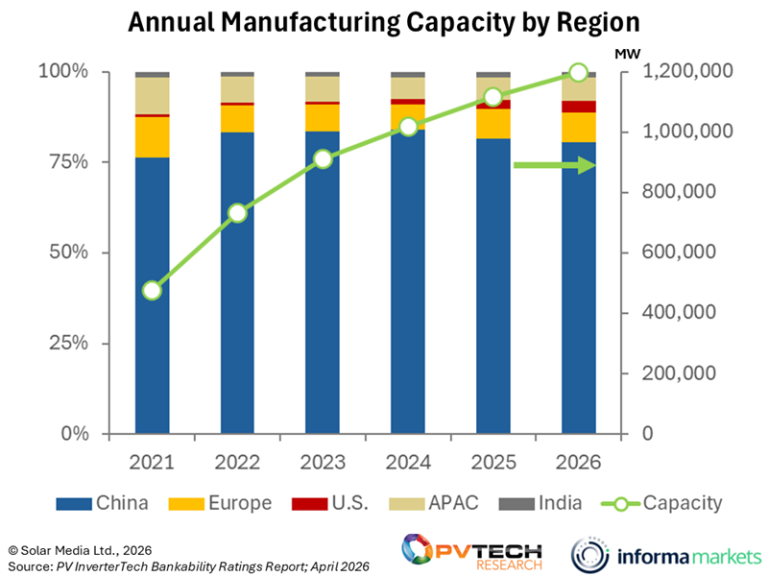

As illustrated in Figure 1 below, the manufacturing capacity of the top 26 inverter manufacturers is still predominantly based in China. However, the share of manufacturing in the US is gradually increasing, with over 3% expected by the end of 2026 (almost 40GW). European companies such as Power Electronics and SMA Solar are also investing in US-based facilities, with Spain’s Power Electronics planning a 20GW inverter factory and SMA Solar restarting US production this year through a partnership with Tennessee-based Create Energy.

Europe’s push for regional manufacturing

Figure 1 also highlights the steady growth in European manufacturing capacity from the top 26 inverter manufacturers, with Europe’s share projected to rise to 9% by the end of 2026 (over 100GW).

Europe is focusing on reducing dependency on Chinese imports, leading to a gradual increase in domestic manufacturing capacity. This shift is part of a broader strategy to address supply chain vulnerabilities and comply with local regulations. The Net-Zero Industry Act, for instance, aims to have 40% of annual deployed net-zero technology manufactured domestically by 2030.

Chinese manufacturers, such as Sungrow, are adapting by establishing production facilities within Europe, including a factory in Poland to meet local regulatory requirements. However, export rebate cancellations and material restrictions are expected to pose significant challenges. Export rebate cancellations, which have been implemented in China, remove financial incentives for manufacturers exporting goods, increasing production costs and reducing competitiveness in global markets. Material restrictions, such as limitations on the availability of critical components such as semiconductors, rare earth metals and polysilicon further complicate production and supply chain operations. These challenges are likely to impact Chinese manufacturers’ ability to maintain their global market share, particularly in regions like Europe and the US, where domestic production and compliance with local regulations are increasingly prioritised.

India’s policy-driven growth in the inverter market

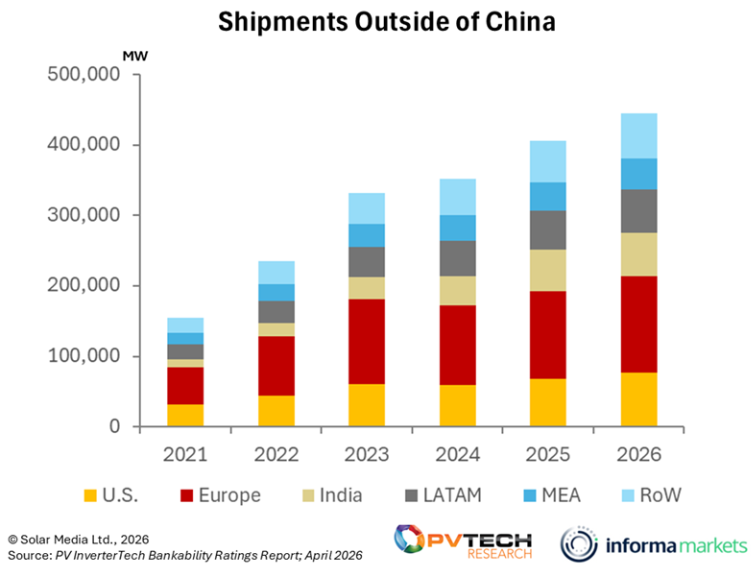

India has emerged as a key growth market for PV inverters, driven by supportive government policies and increasing demand for renewable energy. It has seen the largest recent increase in shipments, driven by its growing renewable energy market. However, rising costs for manufacturers relying on foreign components may pose challenges. India has implemented policies to encourage local manufacturing, such as the Production Linked Incentive PLI scheme, with import duties on certain components and incentives for domestic production. While these policies aim to boost local manufacturing, they can make imported components more expensive, therefore increasing production costs for manufacturers who still rely on foreign parts. To address this, many companies are ramping up their presence in the region by increasing shipments, establishing production facilities, investing in vertical integration and increasingly partnering with or sourcing components from local suppliers to reduce costs. Sungrow leads the Indian market with over 30% market share and operates a 12.5GW inverter manufacturing facility in Bangalore. Sineng follows closely with a 10GW facility in Bengaluru, further solidifying India’s position as a key growth market for inverter manufacturers.

The shift in focus toward India highlights the strategic importance of diversifying production and shipment strategies to mitigate risks associated with regional policy changes and fluctuating demand in traditional markets like Europe and the US.

Challenges in the European and US markets

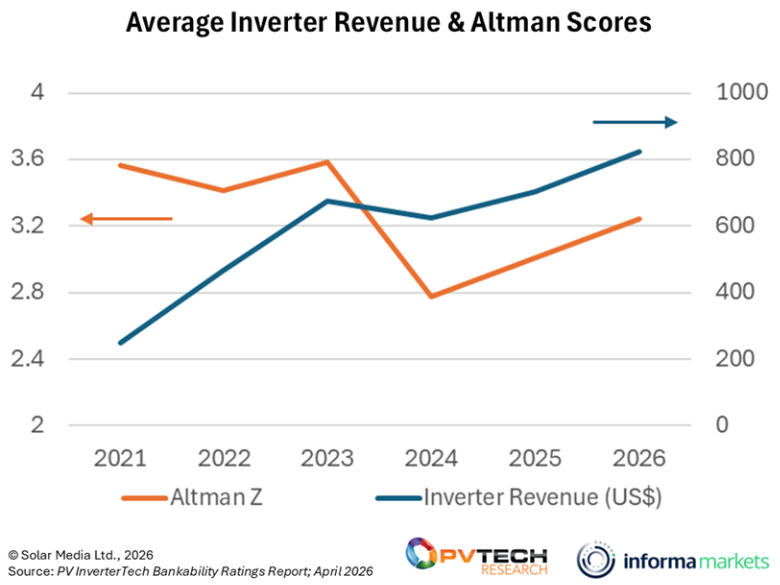

In 2024, average inverter revenues across all companies in the report declined, with shipment growth limited to just 10% compared to 2023. This slowdown was attributed to elevated inventory levels, reduced demand in key residential markets (notably in Europe and the US) and intensifying price competition from Chinese manufacturers.

Despite policy-driven efforts to boost domestic manufacturing, the European and US companies face challenges, including reduced demand in key residential markets, intensifying price competition from Chinese manufacturers, supply chain disruptions and fluctuating raw material costs. Additionally, inconsistent or evolving government policies, with increasing labour and energy prices, further threaten their ability to recover both inverter revenues and shipment volumes in the near future.

Following years of rapid growth, the sector entered a normalisation phase, as overstocked distribution channels significantly curtailed new orders from Western manufacturers such as SolarEdge and SMA Solar. Meanwhile, aggressive competition from Chinese players such as Huawei and Sungrow led to sustained price declines across all inverter product categories.

These challenges directly impacted share prices and eroded investor confidence in 2024, negatively influencing the average Altman scores of companies. However, signs of recovery emerged in 2025, with further improvement anticipated in 2026. This recovery is expected to be driven by a strategic shift toward the energy storage system (ESS) market, which is likely to enhance investor confidence further. Policies supporting ESS adoption will play a crucial role in shaping the future of the PV inverter industry.

Conclusion

Evolving global policies are reshaping the PV inverter industry, driving a shift toward regional manufacturing and diversification of supply chains. While challenges remain, particularly in traditional markets like Europe and the US, policy-driven growth in regions like India and the strategic focus on ESS offer a pathway for recovery and long-term sustainability.

Manufacturers that adapt to these policy changes and align their strategies with regional requirements will be well-positioned to thrive in the evolving global landscape. As the renewable energy sector continues to grow, the role of policy in shaping the future of the PV inverter industry cannot be overstated.

All data and analysis shown in this article come from our in-house market research. Full details on how to subscribe to our PV InverterTech Bankability Ratings Report can be found here.