Reforms to the UK’s grid connection process for renewable energy projects are underway, aimed at easing the logjam of applications. Molly Green explores how a well-intentioned process has been hampered by confusion and delays.

In April 2025, the UK’s energy market regulator Ofgem approved a plan to radically change the way that the National Energy System Operator (NESO) handles applications for grid connections by renewable energy developers.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The queue of renewable energy projects waiting to connect to the UK electricity grid reached 756GW in February 2025, 587GW of which was at the transmission scale. A large proportion of this was considered to be taken up by “zombie projects” – those that are put forward speculatively and never carried through.

So, NESO set out to clear that queue. Under the new system, projects are divided into one of two ‘gates’: those that meet criteria for connection will be designated ‘Gate 2’ and will get a confirmed modification offer that includes updated connection dates, site details and required network reinforcement works as applicable.

On 8 December, the operator announced nominal results of the transmission connection queue reshuffle. A total 283GW of projects were given Gate 2 allocations, with 132GW ‘Phase 1’ projects due to connect before 2030 and 151GW of Phase 2 allocations given dates up to 2035.

Projects determined not to meet the criteria, totalling 216GW, received Gate 1 offers, which means they will remain in the system with a provisional deferred connections offer and will be allowed to reapply for Gate 2 status through biannual application windows.

One developer characterised Gate 1 as containing projects that “essentially do not exist as far as the system operator is concerned”.

To demonstrate that their project belongs in Gate 2, developers had to prove it to be both “ready” and “needed”. The readiness criterion is relatively straightforward: having land rights secured or a planning application made (the latter in the case of large-scale solar projects classified as nationally significant infrastructure projects).

Showing that a project is needed has proved harder. In brief, a needed project would align with the various requirements outlined by the UK government in its Clean Power 2030 (CP30) action plan for achieving an energy system entirely powered by renewables by the end of the decade.

Proving a project is needed

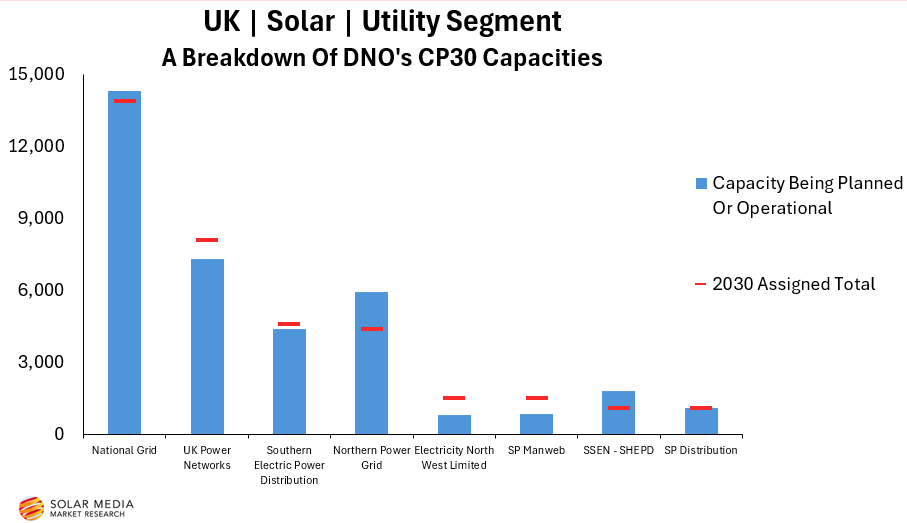

Part of CP30, which acknowledged grid connections as a key barrier to deployment, saw NESO set out rough capacity allocations by region across the UK, which the government adopted in its planning.

Compared to those allocations, the solar projects due to receive Gate 2, Phase 1 connection offers will have a combined capacity of around 30GW, actually falling short of projected need for CP30 (although this does not account for private-wire and rooftop installations, which will be counted toward the target).

Post 2030, Phase 2 projects see oversupply in most UK regions, but three areas (T3, T8 and T9) still have available capacity.

Once offers are accepted (or not) and progress begins to be made, applications will reopen for Gate 2 for the capacity need not met by this first round, providing an opportunity for projects currently not in the planning system to move up in the queue. It is worth noting that NESO said that “projects which applied earlier took priority” in the solar offers it gave.

The sector that will see the most disruption as a result of the reforms is battery energy storage. All of the capacity awarded Gate 2 connection offers (83GW) had ‘protected’ status, meaning the projects awarded all had grid connection offers in place before the queue reshuffle.

Compared to CP30 needs, there will be an oversupply of battery energy storage of 62GW by 2035. Because only protected BESS projects will be issued connection offers, 153GW of projects were not ‘prioritised’, receiving Gate 1 offers or removed completely. It is unlikely that there will be capacity for new BESS projects to connect between now and 2035. Further, some protected projects will have been moved to a later date, but still considered prioritised.

Indeed, the connection reform has, since early consultation, been regarded as something that will create clear winners and losers.

Speaking before the results of the reform were announced, an Ofgem spokesperson told PV Tech Power this is because “the new system had to be radical to give developers and investors greater certainty – fast-tracking projects which are ready to go and essential for the move to clean power”.

But no one in the industry feels confident that they will be a winner. Despite wide agreement that the grid reform was necessary, and Ofgem’s assertion that it worked closely with “NESO, ministers and industry to get this right and build a transparent, fair and deliverable system”, there is now a strong feeling that the process was rushed, with numerous oversights along the way.

NESO oversight and NESO’s oversights

Dissatisfaction with elements of the grid queue process reform, such as regional capacity allocations and the criteria that make a project ready to connect, was perhaps always going to cause complaint from somewhere.

What was not foreseen was the apparent lack of readiness by NESO to handle the volume of work that taking on the connection queue would inevitably entail.

The window for submissions for a grid connection under the new process opened on 8 July 2025, at which time the evidence window was due to close on 29 July, before NESO processed applications to issue new connection agreements in autumn.

Eight days later, on 16 July, NESO held a webinar in which it confirmed that the deadline for applications would be extended, having heard developers’ reports of issues with the application portal, ranging from poor user interface to being unable to upload evidence documents.

Beyond the technical errors, the portal also required battery energy storage system (BESS) developers to give the capacity of their prospective energy storage project in megawatt-hours. Because this cannot be accurately predicted before a battery storage system is operational, developers were stuck; they could not commit to an energy capacity and were unsure what bearing a given figure in megawatt-hours would have on their chances of receiving a connection offer.

Speaking in the webinar, Matt Magill, director of engineering and customer solutions transformation at NESO, assured that megawatt-hour figure given for lithium-ion BESS will not be used by the operator.

He explained that other types of energy storage not included in the Clean Power 2030 technology classes do need to be able to declare themselves as long-duration, which is why the portal used duration as a metric. He assured that “if you do not meet the long-duration energy storage requirement, you won’t be required to give a megawatt-hour figure”.

The application window was closed almost a month late on 26 August.

UK solar industry feels the impact

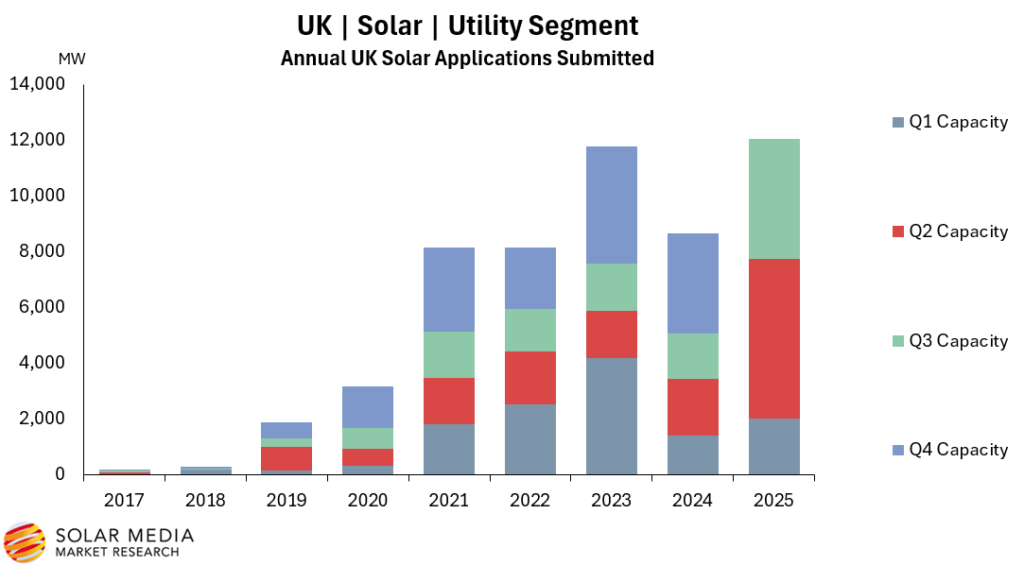

In the run up to the closure of the grid connection application window, developers rushed to submit projects. Solar Media Market Research figures show that applications soared in the 10 months up to August 2025, with over 175 projects (15GWp) being submitted to their relevant local authorities or to the government (Figure 1).

The deadline also put pressure on planning decisions. In May, June and July, local planning authorities (LPAs) in the UK decided over 80 projects.

The flurry of activity relating to grid connections has created a major opportunity in the mergers and acquisitions segment, according to Solar Media Market Research analyst Josh Cornes.

He said that over 2GW worth of solar PV has changed hands so far in 2025, with upwards of 15 developers selling. With connection dates expedited and squeezed into a smaller timeframe, large portfolios are looking at just a couple of years’ build window, which is too expensive for developers to oversee simultaneously.

Some developers simply have portfolios too large to handle, so are forced to sell to free up resources and raise capital for the remainder of their portfolio.

For example, developer Low Carbon has sold off over half of its portfolio to TotalEnergies this year. The latter took on an eight-site portfolio from Low Carbon, totalling 350MW.

Transmission-scale developers feel particularly under pressure. If developers wait until the announcement date for their grid offers, any that get pre-2029 connections may simply not have enough time to go through the conditions process and construction to hit the commercial operation date (COD) NESO assigns them.

Indeed, as Shraiya Thapa, clean energy knowledge lead at law firm Freeths, puts it: “Grid reform has been a necessary but at times painful process for developers, many of whom have had to reassess the viability of their portfolios, locational spread and business models going forward.

“While near-term projects originally due to connect between 2026-2028 should mostly be ‘protected’, due to delays in forming the queue, there is much concern that these dates will slip.”

Although at the time of publishing the specific projects given connection offers were unknown, Solar Media Market Research sees about 5GW-worth of transmission-scale solar projects waiting for connection offers to be given in Q2 2026, by which point they will have fewer than three years’ development time pre-2030.

Undoubtedly, reform of the overburdened grid connection process was long overdue in the UK to address the backlog of applications in the queue. But the jury is still out on the extent to which a process that has created substantial additional challenges for developers will ultimately prove successful in its initial goal of a more streamlined and efficient system.