Volatile energy prices in Europe are throwing the future of the long-term power purchase agreement (PPA) into question as market instability and uncertainty abound.

The result will be, according to Werner Trabesinger, head of quantitative products at renewable advisory firm Pexapark, a shortening of the typical PPA contract length to between two and five years compared with the typical 10-year contracts found today.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

While this will insulate companies from long-term market convulsions, protecting profit margins in the process, it will also pose challenges when it comes to project finance.

Shorter PPAs mean less long-term revenue certainty and therefore less security for project financers, although Trabesinger says solar’s status as a competitive energy source and high market prices should alleviate these concerns.

PV Tech Premium sat down with him following the release of Pexapark’s European PPA Market Outlook 2022 report published on 10 February that predicted “fundamental changes” to European PPA markets.

Why are European energy markets so volatile?

In short, rallying energy demand, gas price volatility and a decarbonisation push across Europe have seen power prices shoot up. A year after seeing some of the lowest spot electricity prices ever of between €20-€30/MWh (US$23-34/MWh), Europe’s power prices are now well above €100/MWh (US$114/MWh).

This in part has been caused by the lifting of lockdowns and economies firing up again, causing electricity demand to surge, but there is also the issue of Russian gas that supplies much of the continent’s needs. Europe came out of last winter low on stored gas volumes, which meant countries were looking to replenish their supplies over the summer.

These hopes were somewhat built on Nord Stream 2 – the gas pipeline between Russia and Europe, which is still awaiting regulatory approval – being up and running. The situation was not helped by the Russia-Ukraine crisis that meant Europe was even more reluctant to approve greater Russian influence over its energy security.

“And that left the European gas market pretty squeezed in Q4,” says Trabesinger, “the first very notable spike [in prices] occurred in early October, then the situation got more tense in November and December, which is when these really extreme price moves occurred in the power market.”

While the gas market has calmed following imports from the US and other measures taken by EU states, there has been a lasting impact on PPAs following tremendous volatility in December, says Trabesinger.

The impact on PPAs

Extreme volatility at the end of last year, at points reaching up to 250%, had a dual effect on Europe’s PPA market, notes Trabesinger. Firstly, utility off-takers that trade and hedge their PPA books are liable to put up margin payments and that has cost European utilities hundreds of millions of euros, he says.

“Several European incumbent utilities have had to draw down multi-billion-dollar short term loans to cope with that situation, which has extremely strained the cash balancing of these firms,” says Trabesinger, adding that many utilities are re-evaluating a business model that could see them face “life-threatening cash shortages”. This is not to be mistaken for actual trading losses, he explains, as they have been used to cover credit risk and will eventually be recouped.

Second, utility offtakers must manage power price exposures for the next 10 to 15 years in the traded market. “All the while, as they do so, they’re subject to price moves. Of course they try to mitigate most of the price risk back in the market but the more volatile the market gets at large, the higher that risk is,” says Trabesinger.

“So how you price the PPA contract, and especially how defensively you price it, depends on what you expect future volatility to be like,” he explains.

“What is it going to be like in the future?” asks Trabesinger. “Will you see that period of 10% to 20% volatility again? Or are we in for longer, structurally higher volatility?”

What it means for the future PPA market

Uncertainty regarding future market prices is causing chaos among European utilities – “the market consensus on pricing has fallen apart”, says Trabesinger. He points to typically stable markets such as Spain and the Nordics that usually have a consensus on pricing but are now unsure about where the market is headed.

Conversations with European PPA traders revealed that many were not accepting trades in Q4 2021 given the market uncertainly and risk to margins, Trabesinger tells PV Tech Premium.

And while high prices might be good to renewable asset owners who sell their power on Europe’s markets, volatility and uncertainty is not. “If there starts to be a perception that volatility will remain very elevated for long periods of time, that will be a negative for PPA prices, with a smaller number of active offtakers.”

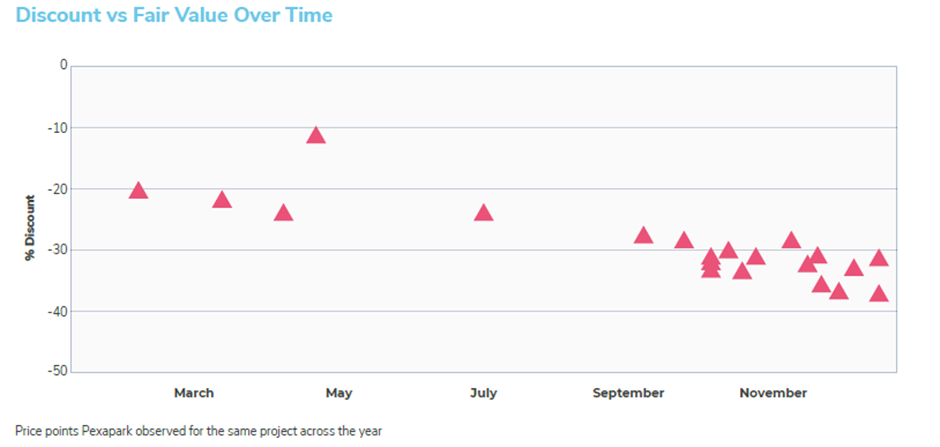

“Due to the current situation, we have seen utilities and trading houses marking up their discounts in unprecedented manners of up to 40% on their bids or halting risk taking all together,” said Pexapark’s report (see below).

All of this throws the long-term PPA contract into question, says Trabesinger. “The risk involved in these contracts being on your balance sheet is very large”, he says, adding that renewable power companies could move away from longer tenders to those of two-five years, meaning the market becomes increasingly hedgeable.

“Most markets have at least three years of liquidity. If you do a five-year PPA, the off-taker can very efficiently hedge out most of that risk into the market.”

Moreover, shorter PPAs mean less risk on company balance sheets, says Trabesinger, meaning they will price the PPA more competitively as they can mitigate most of the risk. “This also means it is much easier for the market to converge to a consensus on how that risk is priced.”

However, moving to shorter PPAs does also pose some challenges in terms of leverage for project finance, says Trabesinger. Securing a sales price for 10-years affords a high degree of leverage for a project but “given the really healthy price levels that we are seeing now, we should see a consistent shift to shorter duration PPAs.”

Indeed, when you look at solar as a technology, banks should be comfortable extending a loan even if the PPA duration is much shorter because solar has proven itself competitive and the idea of market coming back down to ultra-low power prices will be deemed unlikely, says Trabesinger.

The last few months have been tumultuous for European energy markets, with companies scrambling to react to the volatility. According to Trabesinger and Pexapark, a safer bet might be to think short-term while such uncertainty persists, de-risking operations and ensuring flexibility.