The photovoltaic industry has demonstrated resilience and continued technological advancement despite significant market challenges, according to the 17th edition of the International Technology Roadmap for Photovoltaics (ITRPV), released this week at Intersolar Europe.

The comprehensive report, compiled by 38 leading international companies and research institutes spanning the entire crystalline silicon (c-Si) value chain, reveals an industry in transition—shifting toward more efficient technologies while maintaining its historical cost reduction trajectory.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

Learning rate holds strong at 26%

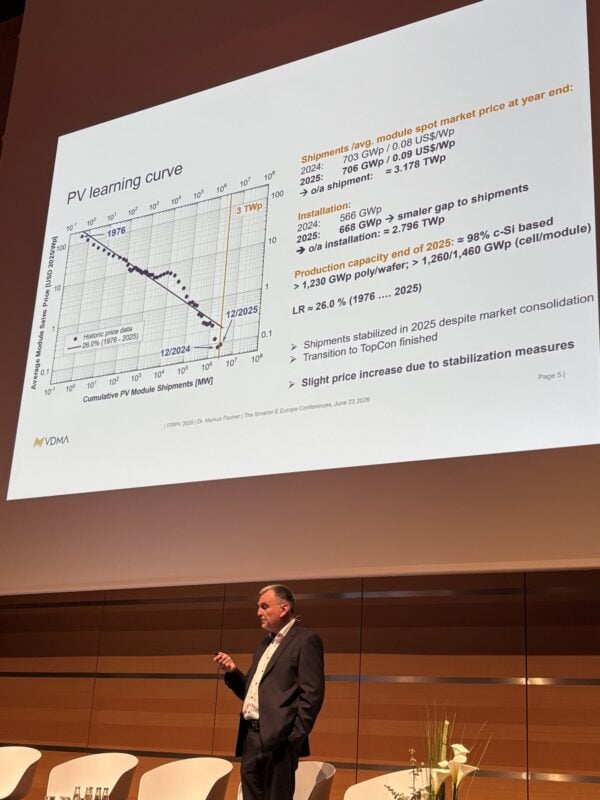

A headline finding is that the PV industry’s learning rate has increased to 26% for the period from 1976 to 2025, up from 24.9% in the 15th edition. This metric, which measures the price reduction for every doubling of cumulative production, demonstrates the industry’s continued ability to drive down costs despite recent market volatility.

After experiencing dramatic price drops in 2023 and 2024, driven by overcapacity and intense competition, module prices stabilised and even increased slightly by the end of 2025, reaching approximately US$0.09 per watt-peak (Wp), up by around US$0.01 at the end of 2024. This price recovery was primarily attributed to energy market reforms in China, which have led to a freeze in new capacity expansions and brought some balance to a market that had been struggling with significant oversupply.

N-type dominance

The solar industry is witnessing a fundamental technological shift. The report confirms that n-type tunnel oxide passivated contact (TOPCon) technology surpassed traditional p-type passivated emitter and rear cell (PERC) technology in market share during 2024, with this transition accelerating throughout 2025.

Current module efficiencies reflect this technological evolution, with n-type TOPCon modules now achieving 23.5% efficiency, matching heterojunction (HJT) technology at the same level. TOPCon-based back contact (TBC) technologies lead the pack at 24.1% efficiency, while p-type mono-Si PERC modules remain at 21.7%. The report noted that price premiums for high-power, bifacial and n-type modules have largely disappeared, indicating that these advanced technologies have become mainstream rather than premium offerings.

New manufacturing capacity is overwhelmingly focused on n-type concepts including TOPCon, HJT and interdigitated back contact (IBC) cells. New p-type PERC capacity is expected only on a small scale outside China. Back contact manufacturing technology is gaining traction, with the report predicting a 28% market share for BC cells in the next decade.

Crystallisation and wafering

The crystallisation and wafering segment has undergone significant transformation, according to the ITRPV, driven by the need to reduce material costs while accommodating larger wafer formats. Global production capacity for polysilicon, ingot and wafer manufacturing exceeded 1,230GWp by year-end 2025.

Polysilicon remains the most expensive material in c-Si solar cell production, making efficiency improvements in this area critical for cost reduction. The Siemens process continues to dominate silicon feedstock production, maintaining its mainstream position with approximately 85% market share in 2025. The fluidised bed reactor (FBR) process holds the remaining 15% and is expected to gradually increase to around 28% within the next decade.

The industry is making progress in reducing polysilicon consumption per wafer. For M10 (182.0 x 182.0mm²) format wafers, consumption is projected to decrease by approximately 26% over the next ten years, while G12 (210.0 x 210.0mm²) format wafers are expected to see a reduction of about 26.4%.

These improvements will be achieved through better yields in crystallisation and wafering processes, further reductions in kerf loss and continued wafer thickness reduction. Within ten years, polysilicon consumption is projected to reach approximately 1.39g/W for G12, 1.27g/W for M10 and 1.29g/W for G12 (R) formats.

The report reveals clear market dominance of recharged Czochralski (RCz) ingot crystallisation, which is expected to maintain approximately 95-100% market share through 2025 and beyond. Continuous Czochralski (CCz) processes are expected to gradually gain market share, reaching around 5% by 2036.

Magnetic Czochralski (MCz) technology, introduced in mass production starting from 2025, offers the potential to eliminate further impurities and extend crucible lifetimes. The technology is projected to capture more than 5% of the market by 2036, though RCz will continue to dominate.

Notably, kerfless wafering and direct wafering technologies are expected to enter the market around 2033 but will remain below 1% market share through 2036. This suggests that traditional diamond wire sawing will continue to be the mainstream wafering technology for the foreseeable future.

Wafers becoming larger and thinner

The wafer segment has seen significant standardisation around larger formats, with M10 and G12 sizes and their rectangular variants dominating new installations. The M6 format was completely phased out by 2025, reflecting the industry’s decisive move toward larger wafers.

By 2036, G12 and G12 (R) formats are expected to cover approximately 76% of the market, while wafers larger than G12 (>G12) will reach close to 20% market share. Rectangular M10 formats will sustain some market share, while standard square M10 is projected to phase out entirely. This trend means new cell production lines must be designed to accommodate these larger formats and remain flexible for even larger sizes in the future, the report noted.

One of the most significant ongoing trends in the crystallisation and wafering segment is the reduction in wafer thickness. For n-type wafers, which now dominate the market with approximately 82% share in 2025 and that the report expects to grow to more than 98% within ten years, minimum as-cut thickness continues to decrease across all formats and cell technologies.

The report shows no significant difference in thickness trends between M10 and G12 formats for n-type wafers. HJT technology leads the wafer thickness reduction rate, moving toward the thinnest wafers. G12 IBC wafers are expected to reach a wafer thickness of 110 µm within the projection period.

However, as wafer thickness decreases, practical challenges related to bending and handling must be addressed, the report noted.

Cell manufacturing

Cell production capacity reached 1,260GWp by the end of 2025, with manufacturing increasingly focused on larger cell formats to accommodate creative cell-to-module architectures. The shift toward n-type technologies is particularly pronounced at this stage, with TOPCon and HJT capacities being deployed as the foundation for future c-Si-based tandem concepts.

The report highlights growing sophistication in cell manufacturing, with improved tool concepts enabling better-matched throughput between front-end and back-end processes. This optimisation is crucial for supporting future capacity increases while maintaining quality and efficiency standards.

One notable trend the report highlights is the introduction of laser-enhanced contact optimisation (LECO) for TOPCon lines, a process step that boost the conversion efficiency of TOPCon cells.

According to the ITRPV, homogenous emitters with LECO led the market in 2025 at 74% and will increase its share to 86% by 2036. Less than 5% of the market of emitters for n-type TOPCon cells will be manufactured without LECO in the coming decade.

Edge passivation using atomic layer deposition (ALD) or plasma-enhanced chemical vapour deposition (PECVD) processes is expected to gain importance in the coming decade, the report notes, to eliminate edge recombination in technologies such as TOPCon or HJT that use half-cut cells. ALD or PECVD edge passivation is expected to gain 80% market share by 2036.

Silver consumption falls

One pressing challenge in cell manufacturing is the high silver consumption for metallisation. The ITRPV report reveals that the 706GW of modules shipped in 2025 consumed approximately 7,244 tons of silver—representing about 21.4% of the world’s total silver supply. This figure is notably higher than the 17% reported in the World Silver Survey 2026 edition, underscoring the solar industry’s significant impact on global silver markets.

Silver consumption varies by cell technology. In 2025, TOPCon bifacial cells consumed approximately 10mg per watt at the cell level (averaging M10 and G12 formats), while SHJ cells used 12.0mg/W and TOPCon-based back contact (TBC) cells required 12.2mg/W. The higher consumption in n-type concepts stems from the use of silver for both front and rear side metallisation, compared to p-type PERC’s lower requirement of around 8.9mg/W.

As the ITRPV noted, the industry faces a dual challenge: silver prices are notoriously volatile, directly impacting paste and cell costs, and the material represents a significant portion of manufacturing expenses. Silver reached an all-time high of US$3,729 per kilogram in January 2026, though it moderated to US$2,452/kg by June 2026—still corresponding to approximately 2.5 cents per watt per cell.

However, the report highlighted that overall silver consumption in 2025 was significantly below 2024 levels, demonstrating that reduction efforts are working. The roadmap projects aggressive reduction targets, with TOPCon cells expected to decrease to 6.3mg/W and SHJ cells to just 4.3mg/W within the next decade. For M10 format cells, silver consumption is projected to drop from approximately 90mg per TOPCon cell in 2025 to around 60mg by 2036.

Beyond reduction, the industry is actively pursuing silver replacement strategies. Copper-based metallisation technologies are gaining traction, particularly for HJT solar cells. The report projects that by 2036, silver-based metallisation for HJT cells will decline to just 8% market share, with copper-based metallisation capturing 62% and pure copper metallisation reaching 30%. “It is very clear that silver will be replaced for [HJT],” the report notes.

The report emphasises that continued reduction in silver consumption is essential not only for meeting future production and cost targets but also for partially decoupling PV cell production from silver price fluctuations. Close collaboration between paste suppliers, screen manufacturers and cell producers will be critical to achieving these ambitious reduction goals while maintaining cell performance and reliability.

“We see that for the first time in several years, silver consumption was reduced with the same amount of shipped modules,” said Markus Fischer, co-chair of the ITRPV steering committee at the report launch in Munich earlier this week. “So this is really good news.

“This is mainly realised by the efficient cell technologies and cell layouts, and also we see that copper-based materials are introduced especially for HJT, and in the future it will also be for tandem. And what we see here is peak consumption for silver. I am quite confident that silver will not be a material of shortage [for PV manufacturing].”

Reducing material costs crucial for module assembly

Module manufacturing capacity reached approximately 1,460GWp by year-end 2025, with roughly 98% market share for c-Si technologies and about 2% for thin-film alternatives. This was close to the 1,500GWp recorded in the last report.

Reducing material costs and improving performance are key objectives in reducing overall module costs. On the former, reducing material volumes—for example, the thickness of glass, and reducing material waste—are among the main approaches, while on performance, measures include reducing optical losses on the front side, reducing resistive losses and reducing interconnection losses.

Glass has become a hot topic in the industry in recent years, with spontaneous breakage a growing concern. The report noted that glass of between 2 and 3mm is mainstream for glass-glass modules today, with thicknesses lower than 2mm expected to gain some market share in the coming years, from 5% today to around 10% in 2036. But glass of 2-3mm thickness will dominate, with a market share of 86% by 2036.

Other areas being targeted for cost reductions at the module level are encapsulation and back cover materials, both significant cost contributors. The report noted that pure ethylene vinyl acetate (EVA) still has considerable market share due to its cost efficiency, but pure polyolefins (POE) and EVA/POE mix encapsulants will gain market share in the future due to their higher reliability.

Glass is expected to become dominant back cover material in the coming years, with the combination of glass at the front and foil at the back falling to under 16% market share within the next ten years.

Future technology horizons

Looking ahead, the roadmap projects continued efficiency improvements for single-junction cell technologies, with module efficiencies expected to reach 26.3% by 2035. However, the most exciting development lies in tandem cell technology, which promises to break through single-junction efficiency limits.

According to survey results, tandem cells and modules are expected to enter mass production around 2027, with module efficiencies of approximately 27.4% anticipated by 2028. These silicon-based tandem technologies represent the next frontier in PV efficiency, potentially enabling even higher performance levels in subsequent years.

The report also emphasises growing importance of recycling as both a business opportunity and challenge, as the installed base of PV systems continues to expand. Smart factory approaches and advanced manufacturing concepts, including improved data transparency and tracking systems, are expected to play increasingly important roles in supporting the industry’s growth trajectory.

A multi-terawatt future

The ITRPV report concludes with an optimistic yet realistic assessment of the industry’s future. Based on the broad electrification scenario from researchers Dmitrii Bogdanov and Christian Breyer cited in the ITRPV, the PV industry must install approximately 63.4TWp by 2050 to achieve a net-zero greenhouse gas emission energy system, generating 104 petawatt hours (PWh) of electricity—roughly 69% of global primary energy demand across power, heat, transportation and desalination sectors

This translates to an average annual market of approximately 4.5TWp by 2050. While historical shipments have tracked close to required levels, the lack of shipment growth between 2024 and 2025, despite available capacity, suggests that market development must accelerate to stay on track with climate goals.

Despite current overcapacity challenges, the report emphasises positive prospects for the entire c-Si PV industry. The combination of continued efficiency improvements, per-piece cost reductions, technology advancement through tandem cells, and the inevitable growth toward a multi-terawatt market provides a strong foundation for long-term success.

Read all of our coverage of Europe’s biggest solar trade show here.

")