A government-backed study has found that Australia could establish a commercially viable polysilicon manufacturing industry, positioning the country to address an emerging global shortage of non-Chinese material as solar deployment accelerates worldwide.

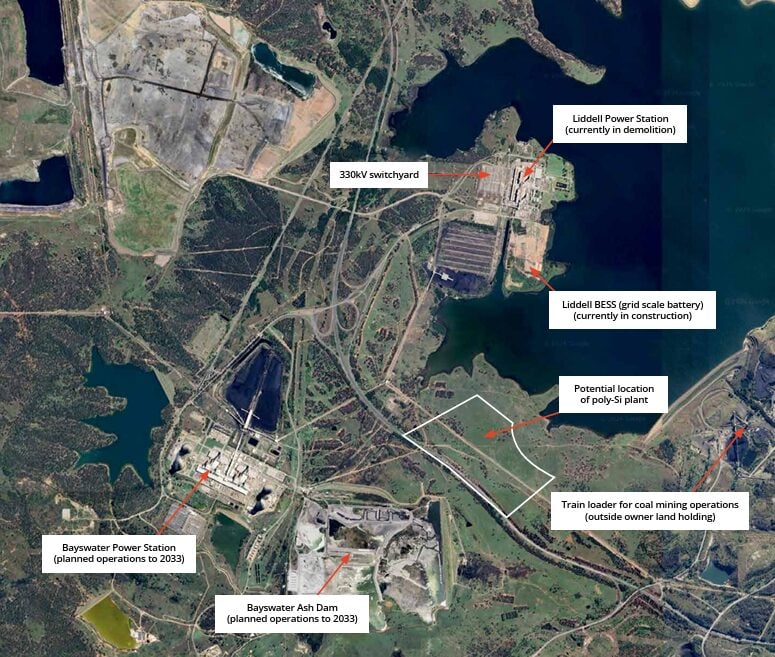

The Australian Silicon (AusSi) Study, supported by the Australian Renewable Energy Agency (ARENA) under the Solar Sunshot Program, examined the potential for a 50,000 tonne-per-year polysilicon facility at the Hunter Energy Hub in New South Wales.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

The report concluded that a credible pathway exists to build an export-oriented, large-scale polysilicon industry in Australia, provided that appropriate government support is in place.

The study estimates that the facility would require total capital expenditure of AU$2.5 billion (US$1.79 billion) to AU$3.5 billion, with government support including an upfront grant of AU$1 billion to AU$1.5 billion and production credits of around AU$200 million per year for 10 years.

With this backing, the project could deliver returns within the typical financial parameters for capital-intensive industrial assets, targeting an internal rate of return of 20% to 30%.

Polysilicon production represents the most energy-intensive step in the solar PV value chain, transforming metallurgical silicon into an ultra-pure material required for solar cells. The process is highly concentrated globally, with China accounting for approximately 95% of production.

However, sustainability concerns, labour standards and supply chain resilience are driving demand for diversified sources, particularly in the US, the EU and India.

Growing supply gap for non-Chinese polysilicon to reach 350,000 tonnes

The study identified a projected supply gap for non-Chinese polysilicon of 240,000 tonnes by 2035, rising to 350,000 tonnes by 2040.

Current and announced projects outside China are falling short of projected demand as downstream cell and module manufacturing capacity expands faster than upstream polysilicon supply.

Non-Chinese polysilicon currently commands prices three to five times higher than Chinese material, reflecting the structural scarcity and premium placed on supply chain security, the study read.

In 2025, non-Chinese polysilicon capacity totalled approximately 199,000 tonnes, with only one-third allocated to solar-grade material for PV applications. The majority serves electronic-grade markets for semiconductor production.

Solar-grade production outside China came primarily from Malaysia (27,000 tonnes), the US (18,000 tonnes) and Germany (21,000 tonnes), representing just 5% of the 1.15 million tonnes produced by China for the PV industry.

The concentration of polysilicon production in China has created vulnerabilities for countries seeking to develop domestic solar manufacturing capabilities.

Australia’s solar PV industry has historically been heavily influenced by Chinese supply chains, with the country importing the vast majority of its solar modules and components from Chinese manufacturers.

Market validation conducted as part of the study found support for Australian polysilicon from downstream producers in six countries, including Australia. Interest was driven by supply chain diversification, alignment with evolving labour and sustainability standards, and long-term security of supply.

Engagement with over a dozen downstream manufacturers across multiple regions worldwide indicated a clear growing demand for diversified polysilicon supply, spanning ingot and wafer producers, cell manufacturers and module assemblers.

The facility would produce enough material to support approximately 27GW of solar module production annually, with 90% to 95% destined for export markets. This scale represents approximately five times Australia’s current annual solar installation rate.

Policy drivers reshaping markets

Trade policy and regulatory frameworks are increasingly shaping polysilicon markets beyond traditional cost considerations.

The US has implemented Section 301 tariffs of 50% to 60% on Chinese imports, alongside anti-dumping and countervailing duties (AD/CVD) ranging from 14% to 3,521% on some Southeast Asian and Indian imports.

The Uyghur Forced Labour Prevention Act effectively bans Xinjiang-origin materials, including metallurgical silicon and polysilicon, while the Inflation Reduction Act rules disqualify projects with Chinese equity exceeding 25%.

Meanwhile, the EU’s Carbon Border Adjustment Mechanism penalises embedded carbon in imports, disadvantaging coal-fired polysilicon production. The Net Zero Industry Act provides regional subsidies and auction preferences for compliant supply chains.

European corporates and governments are prioritising suppliers with transparent supply chains, low emissions, and verified labour practices, leading to premium pricing for green polysilicon.

India has imposed a 20% border duty on modules and cells, with plans to extend it to ingots and wafers. Production-linked incentive schemes reward locally manufactured products based on the Approved List of Models and Manufacturers, favouring non-Chinese sourcing.

Japan, while not introducing hard bans or tariffs, is aligning through corporate procurement standards and alliance diplomacy.

The study states that Australia is positioned favourably across key value drivers, including low risk, strong sustainability performance, quality and intellectual property protection, infrastructure capability and competitive input costs relative to other regions actively expanding manufacturing capacity.

The Hunter Energy Hub opportunity

The Hunter Energy Hub site offers existing infrastructure, including grid connection, water access, transport links and industrial land.

The region is undergoing a transition from thermal coal power generation to a diversified energy and industrial hub, situated within a Renewable Energy Zone (REZ) with a pipeline of generation and firming capacity.

The study estimated the project could generate total economic benefits exceeding AU$1.1 billion annually and create 900 high-skilled full-time jobs.

The facility would aim to address energy dependency risks by enabling Australia to participate significantly in a globally diversified solar supply chain, providing direct returns through new investment, jobs, and exports, and offering opportunities to retrain and transition the local workforce from fossil fuel-based industries to renewable energy sectors.

Australia currently produces around 50,000 tonnes of metallurgical silicon per year, the feedstock for polysilicon production, with plans to expand capacity to approximately 200,000 tonnes.

The proposed facility would use the established Siemens process in production technology, which accounts for approximately 90% of PV polysilicon production globally and is projected to maintain an 80% share by 2030.

The process requires approximately 55kWh per kilogram of silicon, equivalent to 2.7TWh of electricity annually for a 50,000 tonne facility.

Access to low-cost renewable energy would be a key factor in competitiveness, with electricity accounting for over 40% of polysilicon production costs.

Capital costs for building the facility in Australia are estimated at two to three times higher than equivalent plants in China, highlighting adjustments for Australian design standards, construction labour rates, project services and contingency budgets for a first-of-a-kind project.

The study noted that subsequent Australian polysilicon facilities would be able to build on early learnings and development of domestic capabilities to improve economic viability, with Australia having the opportunity to become a cost leader for non-Chinese polysilicon.

Separately, Quinbrook Infrastructure Partners is developing a polysilicon manufacturing facility near Townsville, Queensland, as part of its Northern Quartz Campus project.

That facility, declared a prescribed project by the Queensland government in 2024, is expected to commence commercial operations by 2030 and will be powered by adjacent solar and battery storage projects.

Quinbrook submitted plans for a 750MW battery energy storage system at the site to support the energy-intensive polysilicon production process.

The AusSi Study concluded that, while uncertainties remain regarding the final investment decision, keeping the option alive by advancing to the next development phase is the main recommendation.

The report emphasised that planning, engineering and funding processes must commence immediately to ensure any facility is operational in time to fill the emerging supply gap in the early 2030s.