There is a “general consensus” that the EU “cannot idly stand by whilst the [solar manufacturing] industry is disappearing,” Johan Lindahl, secretary general of the European Solar Manufacturing Council (ESMC) told PV Tech Premium yesterday (5th March).

On the 4th of March, the Transport, Telecommunications and Energy Council (TTE) of the EU agreed to pursue methods to support the European solar manufacturing industry, which is facing what EU Commissioner for Energy Kadri Simson called a “very fragile situation”. Trade bodies the ESMC and SolarPower Europe met with EU state energy ministers, commissioners and members of parliament at a lunch at the TTE council.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

In recent months the European industry has seen a number of exits, most notably Swiss solar manufacturer Meyer Burger which announced the shutdown of its German manufacturing facility in January. Solar ingot producer NorSun and polysilicon producer REC Group also announced operational pauses and shutdowns respectively. The main driver behind this exodus is the price pressure put on European manufacturers by “uncompetitively low-priced” imports from China and a lack of coherent legislative support.

Following the TTE council, Lindahl called for the Commission to implement measures to allow the industry to continue in “survival mode” until the Net Zero Industry Act (NZIA) takes effect, which would “realistically” become viable in 2026, the ESMC said in a document seen by PV Tech Premium.

CAPEX and OPEX

In Simson’s statement following the council meeting, she said: “I will now work on a solar power pledge, where member states and stakeholders would commit to take concrete action to support our production here in Europe.” Details of what was said at the council lunch or what shape the “pledge” will take were not confirmed, but Lindahl said that direct financial support was needed to help new and existing manufacturers.

“We [the ESMC] suggest that the Commission should allow member states to give OPEX (operational expenditure) support in addition to the CAPEX (capital expenditure) support that they are now allowed to give to Net Zero industries,” he said. Recent announcements from the Netherlands, Spain and Germany have all sought to establish CAPEX funding for new solar and energy storage manufacturing capacity, but the EU would benefit from supporting existing producers too.

Lindahl said that the industry would benefit from emergency OPEX funding over a limited period of two years “to bridge the gap until the NZIA is in place and effective.”

He continued: “We have calculated that, if the modules that European manufacturers are manufacturing are sold at market prices, the OPEX support could be in the form of covering the difference between the now-unsustainably low module prices and the manufacturing cost of European manufacturers.”

The ESMC has previously alleged that Chinese module producers had been ‘price dumping’ in Europe, where modules were being sold at ‘uncompetitively low’ prices, which were sometimes below the cost of production. Add to this the ongoing oversupply issue, whereby some estimates say that around 80GW of imported solar modules are in European warehouses and inventories – the EU installed around 57GW of solar PV in 2023, far below the excess inventory.

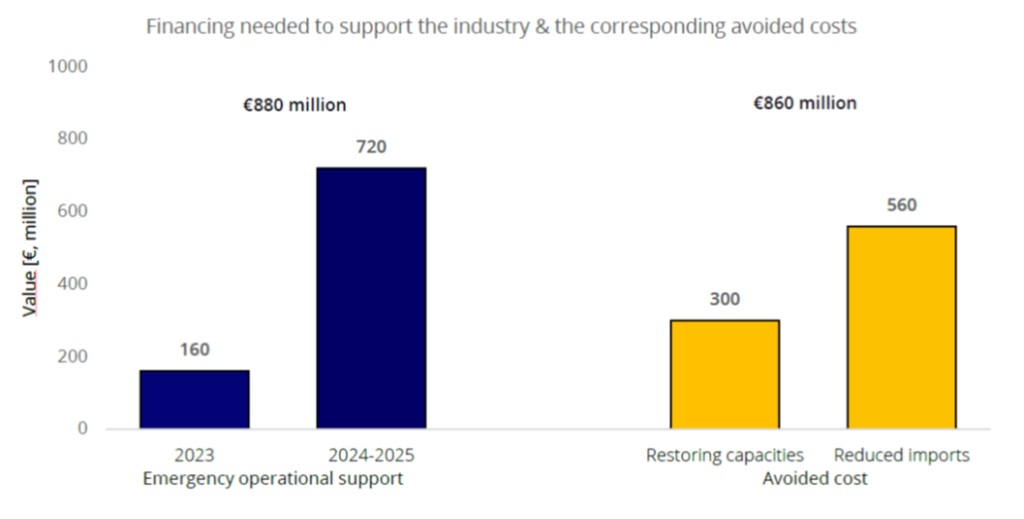

In its emergency support proposal to the European Commission, the ESMC recommended that the commission mobilise support for existing producers to operate at around 40% capacity, which it said was the minimal threshold to maintain economic operation. This would represent 2.4GW of annual European solar module production capacity in 2024/25 and the 0.8GW of European-made modules currently in inventory from 2023.

“We foresee something between €800-850 million to cover the difference between the manufacturing cost and the market price,” Lindahl said. “We are not asking the EU or member states to cover the full manufacturing capacity of all module manufacturers, but just to keep the industry alive at a utilisation rate of around 40%.”

He said that the ESMC has “checked with all the major European manufacturers and they support this.”

Spend now to save later

Committing OPEX support to existing manufacturers – whilst representing the thick end of a €1 billion commitment – could save money in the long run, the ESMC said.

Letting the industry shut down now and then reviving it again once the NZIA comes into force would require CAPEX to establish new sites, facilities and workforces.

The ESMC said that – by its own calculations – maintaining Europe’s roughly 6GW of capacity at 40% would save around €300 million in new brownfield projects. It added that buying 1GW of EU modules would lessen the bloc’s trade deficit with China by about €100 million under current market conditions – money that would stay within the EU and maintain its economy and green jobs.

Solar pledge may be ‘not enough’

In a comment to PV Tech Premium, French solar manufacturing startup Carbon said: “Sweet and fine words are not enough. The European Net-Zero Industry needs swift and concrete actions. Opening the field for Member States voluntary measures is a first necessary step, [but] won’t be sufficient. The deal on the Net-Zero Industry Act and other European regulations will help build a level-playing field to foster the European PV industry, but the EU has to move faster and harder for the revival of the European solar manufacturing sector.”

Carbon has previously announced financing and plans for a 5GW/3.5GW tunnel oxide passivated contact (TOPCon) solar cell and module plant in Fos-sur-mer, France, and spoke to this publication last year about its plans for linking production-at-scale with European research and development (R&D). The company is a member of the ESMC.

Carbon has yet to realise its solar manufacturing plans, and it is unclear what the “faster and harder” moves by the EU might be. Lindahl told PV Tech Premium that, without effective financial support, the whole value chain could be at stake.

“If there are no more European module manufacturers, then the glass manufacturers, the wafer manufacturers and other component producers will have no customers in Europe,” he said. “They cannot sell into China, so there is a huge risk of those companies also going bankrupt or completely moving to the US or other regions.”

Last month, PV Tech’s head of research, Finlay Colville, published a blog surmising that the European PV industry can still take part on the global stage. He said that Europe’s solar equipment manufacturers and research institutes can play a significant role within a number of global markets.

Fellow trade body SolarPower Europe – which was also represented at the TTE Council – took a different tone following Simson’s announcement. Its members cover a wider industry and geographical spectrum than the ESMC, including many of the leading Chinese PV manufacturers.

In a public statement, CEO Walburga Hemetsberger said: “Beyond emergency measures, we urged Ministers to make optimal use of existing financing support under revised State Aid rules and the Recovery and Resilience Facility. To leverage the single market, we further explained our proposal of an EU-wide financing vehicle dedicated to solar manufacturing.

“Having discussed solutions, we were also careful to highlight what should not be considered a solution – trade defence measures. Europe needs a robust industrial strategy accompanied by clear ESG market access standards. History has shown that trade defence measures are a lose-lose scenario, neither supporting manufacturers nor deployment.”

")