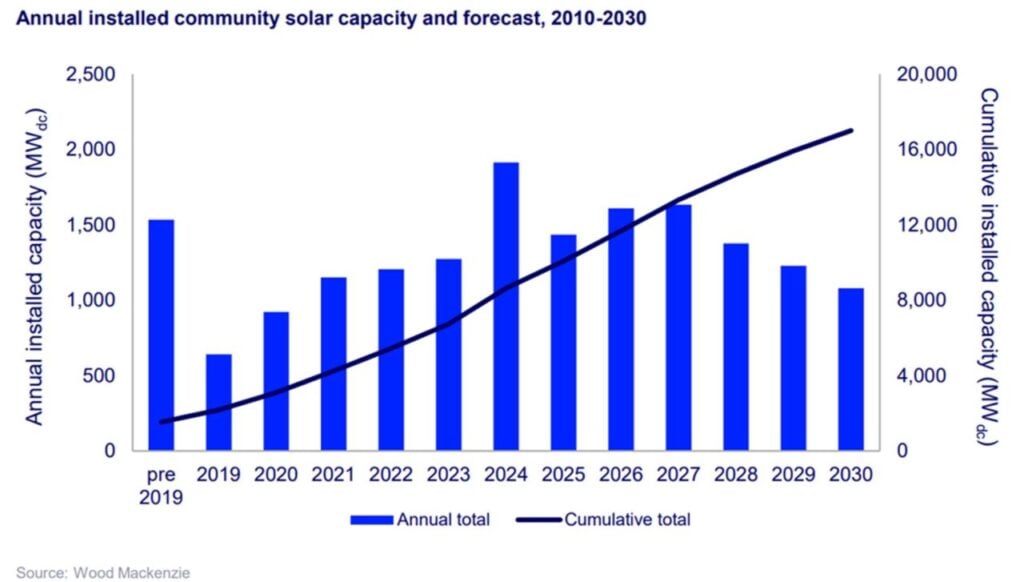

The US community solar sector passed 10GWdc of cumulative capacity in late 2025, according to a report by analysts Wood Mackenzie and the Coalition for Community Solar Access (CCSA).

Despite seeing a 25% year-on-year contraction in 2025 from 2024, community solar in the US is expected to return to an upward trajectory in 2026, with 12% growth forecast for this year.

Try Premium for just $1

- Full premium access for the first month at only $1

- Converts to an annual rate after 30 days unless cancelled

- Cancel anytime during the trial period

Premium Benefits

- Expert industry analysis and interviews

- Digital access to PV Tech Power journal

- Exclusive event discounts

Or get the full Premium subscription right away

Or continue reading this article for free

According to the report, the dip in 2025 was due to a slowdown in mature markets such as New York and Maine.

“Overall, we expect national installed community solar capacity will contract by an average of 5% annually through 2030 in existing state-level programmes,” said Caitlin Connelly, senior analyst and lead author of the report.

“The segment’s near-term growth is anchored by a strong project development pipeline that now exceeds 8GWdc, 29% of which is reported to be under construction. Developers are navigating a complex federal policy landscape and interconnection queue backlogs to ensure their current pipelines are built out as efficiently as possible to meet the start-of-construction and placed-in-service deadlines required to secure the ITC.”

In 2026, capacity additions in Illinois and the Mid-Atlantic markets are expected to drive national annual growth, the report said.

Looking further ahead, the report said further growth was less certain unless new state markets are established. It pointed to strong pre-development pipelines for proposed programmes in states including Ohio, Iowa, Pennsylvania and Michigan as encouraging evidence of future activity.

“So far in 2026, there are signs that the value proposition of community solar is gaining new traction across several states,” said Connelly. “The passage of legislation in these markets could potentially add upwards of 1.5GWdc through 2030; however, the removal of the ITC in 2030 will complicate new programme design and timelines.”

The report said developers are broadening their business models to capture what it said was a growing opportunity for “community-scale” resources, defined as solar installations up to 20MW in size. Ohio and Pennsylvania are favoured target states for this type of development, partially driven by the region’s need for new generation to meet rapidly growing demand.

“Utilities are beginning to prioritise ‘community-scale’ resources, which typically encompass smaller utility-scale projects connected directly to the distribution grid, in their long-term planning,” said Connelly. “These resources have the ability to be deployed more quickly than larger utility-scale projects and, particularly when paired with storage, can improve grid flexibility and reliability.”

Jeff Cramer, president & CEO of CCSA, said passing the 10GW milestone was a “landmark” for US community solar but said the sector still had further potential.

“The expansion of mid-scale, front-of-the-meter solar and storage into new markets signals that our industry is diversifying and adapting in ways that will serve customers and the grid for decades to come. The pipeline is strong, and the states stepping up to create new programmes are proving that community and distributed clean energy remains one of the most compelling tools we have for putting affordable, accessible power within reach of everyone.”